UK Inflation Proves Sticky in the Aftermath of the BoE’s Pause

Persistent Inflation

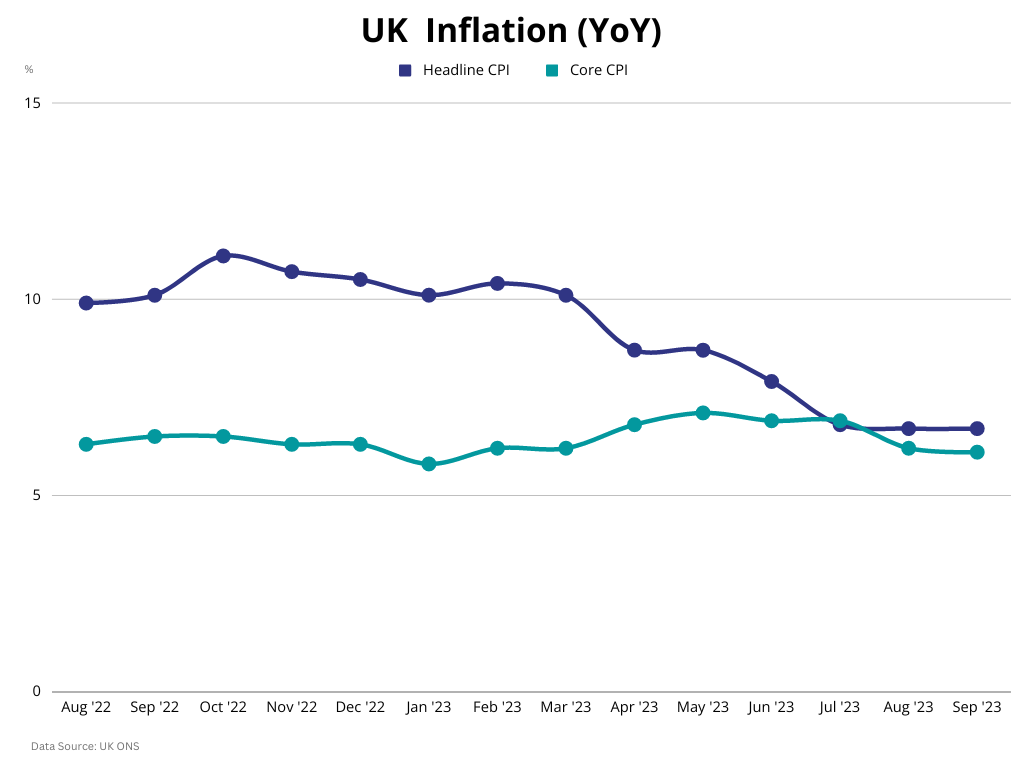

Price pressures in the UK have eased significantly after the October 2022 multi-decades peak of 11.1% y/y in CPI and decelerated sharply in August. Today's release however showed that inflation remains persistent. Headline CPI accelerated 0.5% m/m in September and steadied at 6.7% on a yearly basis. Core CPI, which excludes the volatile energy, food, alcohol and tobacco prices, eased marginally to 6.1% y/y.

Despite progress, the cost of living remains high in the UK, which has the highest inflation among the G7 nations. Chancellor of the Exchequer Jeremy Hunt noted that inflation "rarely falls neatly in a straight line" after the release, but believes it will keep falling "if we stick to our plan". [1]

Rising Energy Prices

The biggest upward contributor to the annual headline rate was "prices for motor fuel" according to the Office for National Statistics (ONS) [2]. Energy prices have increased substantially over the summer, with USOil having appreciated by around 30% since June.

This is largely due to the massive oil supply cuts by Saudi Arabia, Russia and other OPEC+ producers and dwindling inventories. The military conflict that has erupted in the Middle East – a key energy hub – threatens to aggravate the issue.

The events likely set back efforts to normalize relations between Israel and key Arab states, such as Saudi Arabia. Furthermore, Washington appears to have been overlooking the increase in Iran's oil production, but could now adopt a more forceful stance and make any lifting of restrictions much harder.

Wage-Price Spiral

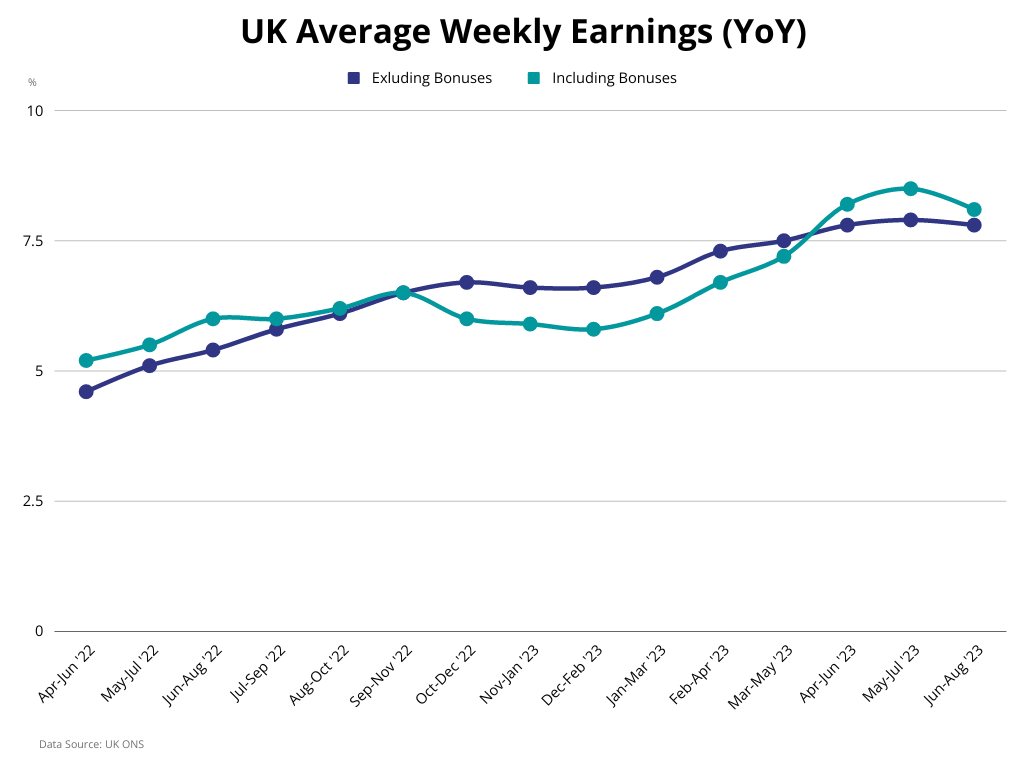

Yesterday's release showed a moderation in pay growth for the June-August period, which will be welcomed by the Bank of England, as average weekly total pay eased to 8.1% and to 7.8% excluding bonuses. However, earnings remain at historically high levels, feeding a wage-price spiral, which makes controlling inflation very difficult.

Governor Bailey has repeatedly spoken about those second round effects and found the wages situation puzzling, according to Reuters, as the usual transmission mechanism is not yet being demonstrated. [3]

Monetary Policy Implications

The Bank of England had paused its tightening cycle last month, after fourteen consecutive hikes, worth 515 basis points. It was emboldened by August's sharp deceleration in inflation, but I had then cautioned that policymakers "could have a hard time staying on the sidelines", as they have been overoptimistic about inflation in the past.

They believe it will continue falling significantly but don't expect it to return below the 2% target for another couple of years. Today's CPI report showed stickiness and keeps the door open to further monetary restraint.

The central bank has maintained its typical non-committal stance and the 4-5 split vote adds to the uncertain outlook. Speaking on Bloomberg after September's decision, Governor Bailey said "the job isn't done yet and we will of course keep on doing the job", refraining from signaling peak rates. [4]

Officials definitely have reasons to not hike again, since they risk sparking a mortgage crisis in their effort to mitigate the high cost of living. Borrowing costs have increased substantially for households and businesses, while mortgages in arrears rose 28.8 y/y in Q2, according to the latest FCA report [5]. At the same time, there is risk of further harm in economic activity. Although it has generally performed better than expected, the economy is in bad shape, as indicated by the slow growth and the poor PMIs.

Market Reaction

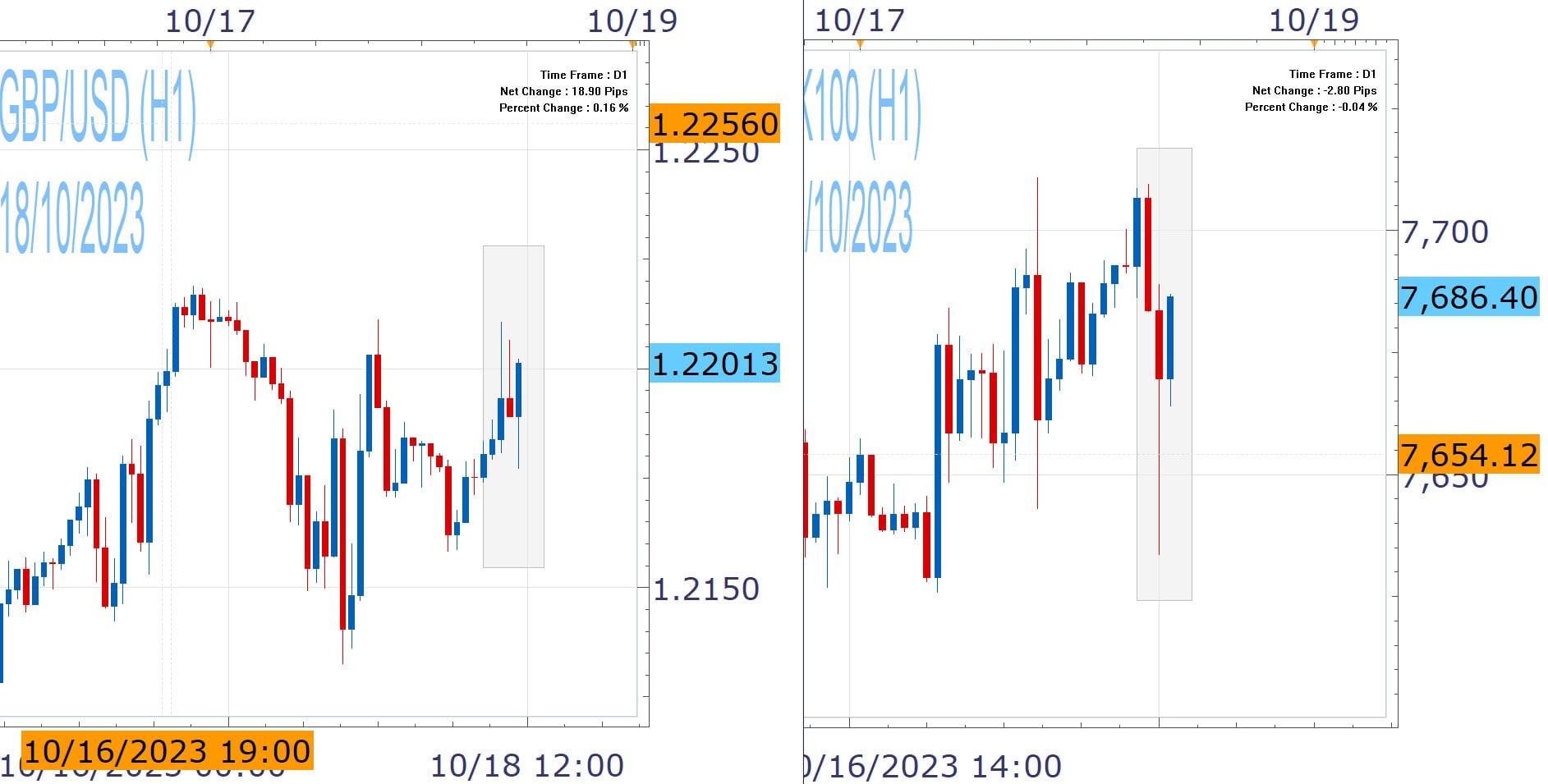

Bond yields are up today and the stock market reacted lower, with UK100 facing pressure, while GBP/USD is underpinned. The CPI release showed persistence, underscoring the need for sustained restrictive monetary stance and keeps further tightening in play. However, market reaction is relatively limited so far, as inflation is on a downward path. It remains to be seen if central bank officials can stand pat again, at their next meeting in November 2.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 17 Oct 2023 https://twitter.com/Jeremy_Hunt/status/1714531837194727651 | |

| Retrieved 17 Oct 2023 https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/latest | |

| Retrieved 17 Oct 2023 https://www.reuters.com/world/uk/boes-bailey-says-hes-puzzled-by-stubborn-pay-growth-uk-2023-10-14/ | |

| Retrieved 17 Oct 2023 https://www.youtube.com/watch | |

| Retrieved 10 Jul 2026 https://www.fca.org.uk/data/commentary-mortgage-lending-statistics-q2-2023 |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.