The PPI spike is likely to influence core inflation further

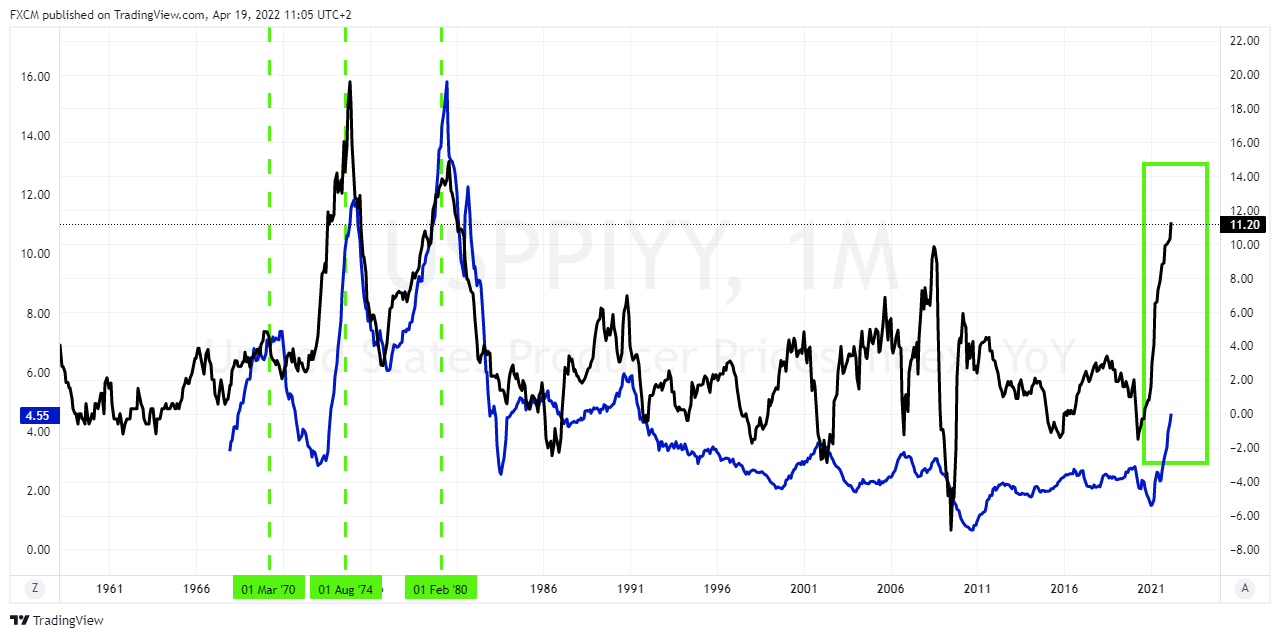

Market participants tend to focus on the CPI because consumption makes up 66% of GDP. Given that core CPI moderated somewhat, this has led to some pundits calling for a top in inflation. In a previous article, we argued that this might be premature given series behaviour in previous inflationary cycles, i.e., 1969, 1974 and 1979. However, PPI is also likely to have a say here, given that it has risen to an astounding 11.2% y/y. Consider PPI's influence on CPI in previous inflationary periods:

The black series is the PPI in this chart, and the blue series is the core CPI. Remember, some market participants are calling for moderation in the core series. However, the above chart suggests that this may be premature, like our previous article. When PPI was spiking and above CPI, it acted like a magnet pulling the blue series up. It was not until the black PPI series crossed below the blue core CPI series (dashed green verticals) that consumer inflation could moderate. I.e. when inflation has spiked above, PPI tended to lead core CPI. The chart highlights the critical crossovers in March 1970, August 1974, and February 1980 that allowed core CPI to abate.

However, the current situation has PPI well above core CPI (green rectangle). The inflation spike environment makes all the difference because the tendency to strip out volatile items is likely to be erroneous in these situations. This price pressure is because supply-side shocks are causing these spikes. I.e. producer inflation spikes are stagflationary and influence real output. It is the cost of food and energy that is contributing to inflation expectations and hitting sentiment. These expectations, as detailed previously, can lead to self-perpetuating cycles, which the Fed wants to avoid at all costs. Hence, their aggressive monetary policy stance. However, this dangerous spiral still has potential, reiterating that more evidence is needed before suggesting a top in inflation.

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.