Oil Prices Subdued after Rise in US Inventories & Surge in China Exports

Higher China Exports & US Inventories

Exports in the world's second largest economy and consumer of oil, surged 16.9% in May year-over-year in USD terms, from 3.9% prior. Imports rose 4.1% and the trade balance expaned to US$78.76bn.

After recent steep decline, US commercial crude oil stockpiles increased by 2.0 million barrels for the week ending in June 3, as Thursdays' report by the by the Energy Information Administration (EIA).

Despite this buildup, at 416.8 million barrels, U.S. crude oil inventories are about 15% below the five-year average for this time of year, while motor gasoline stockpiles dropped by 0.8 million barrels. [1]

Lower GDP Forecasts

Over the last couple of days, we saw two international organizations slashing their global economic growth forecasts, which added fuel to the fire of stagflation fears.

The World Bank projects global GDP to grow by 2.9% in the current year, lower compared to the 5.7% expansion in 2021 and the 4.1% it had projected in January. [2]

USA and China GDP figures for 2022, are also seen lower from last year and previous projections, to 2.5% and 4.3% respectively.

The Organisation for Economic Co-operation and Development (OECD) was also gloomy, as it projects GDP growth to slow sharply this year to 3%, around 1.5% weaker than projected in the December. [3]

OPEC+ Action

Last week the Organization of the Petroleum Exporting Countries (OPEC) and allies including Russia, a group referred to as OPEC+, had decided to accelerate its output increase plan, increasing production by 648,000 barrels per day in July and August.

This did not do much to contain the surge in oil prices however, since the decision did not exclude Russia, which has been facing sanctions from Western countries that have curtailed its output.

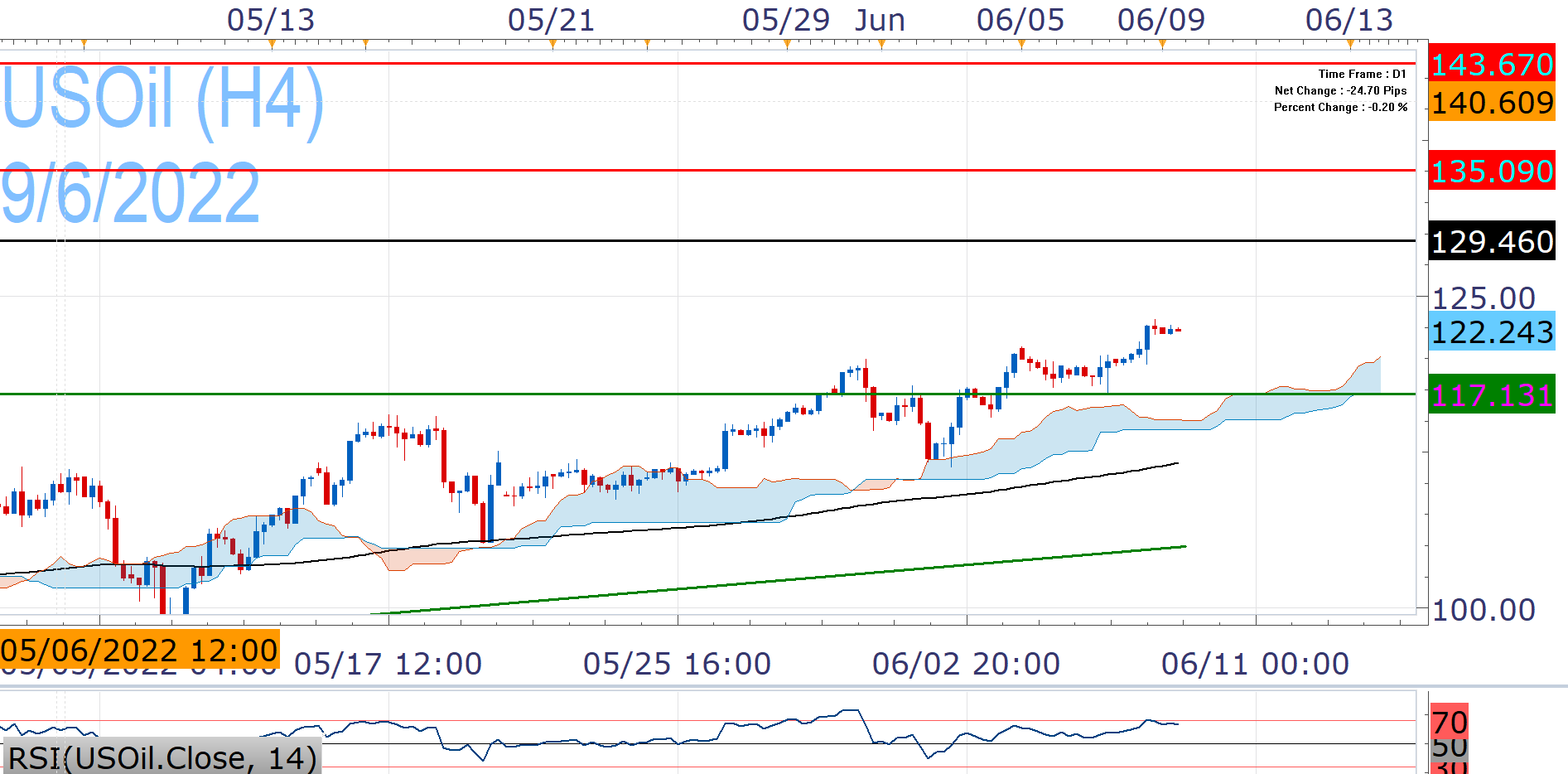

USOil Analysis

Despite the OPEC+ output boost, USOil runs its seventh straight profitable month and third consecutive week of gains. This brings the 14-year high from March (129.46) in its eyesight, but will need fresh impetus for conquering them and look towards 135.09.

However, USOil is cautious today as markets digest latest mixed data and threat of stagflation persist. This week's unexpectedly aggressive rate hike by the Reserve Bank of Australia seems to have renewed these fears, while investors now brace for today's policy decision by the ECB and Friday's US CPI Inflation.

Given today's difficulties and the Relative Strength Index (RSI) hovering close to overbought levels, we could see a pullback towards 117.13, but the downside seems well protected, since the daily Ichimouku Cloud and the EMA200 follow. Daily closes below the latter (at around 115.70) would halt the upside bias, but that looks like a tall order at this stage.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 09 Jun 2022 https://ir.eia.gov/wpsr/wpsrsummary.pdf | |

| Retrieved 09 Jun 2022 https://openknowledge.worldbank.org/bitstream/handle/10986/37224/9781464818431.pdf | |

| Retrieved 03 Jul 2026 https://www.oecd-ilibrary.org/sites/62d0ca31-en/1/3/1/index.html |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.