Apple’s high-stakes WWDC: can AI carry the stock to new records?

Siri 2.0: the missing AI catalyst

Apple's annual Worldwide Developers Conference (WWDC), kicking off on Monday June 8, arrives at a critical juncture for the company's software roadmap. In recent years WWDC has served as the venue for major product announcements, including the Vision Pro AR headset in 2023 and Apple's strategic pivot into generative AI with the announcement of Apple Intelligence in 2024.

However, the subsequent period exposed a glaring gap between Cupertino's strategic AI vision and its real-world deployment. The initial rollout of Apple Intelligence materialised slowly and in fragmented stages, leaving consumers with an ecosystem that often lagged behind rivals. Rather than sparking a wave of consumer enthusiasm, Apple's early AI features felt less like a revolution and more like catching up.

The incoming WWDC could mark the turning point. While the company has not confirmed anything, markets expect Apple to finally unveil the delayed Siri 2.0 – an update to its native voice assistant that has fallen behind the curve. A revamped AI-powered Siri could bring enhanced functionality, with cross-app task automation, on-screen awareness and other improvements.

Should these upgrades successfully materialise, Apple would move deeper into Agentic AI and offer a structural evolution to its mature product portfolio. This could renew consumer excitement, support a device upgrade cycle and increase ecosystem stickiness.

Business momentum builds

Despite a fragile global smartphone market, the flagship iPhone 17 lineup has performed exceptionally well, reinforced by the March launch of the mid-tier iPhone 17e to capture value-conscious consumers. According to Canalys, global iPhone shipments jumped 10% y/y while surging an impressive 42% in China during the first quarter. Concurrently, the entry-level MacBook Neo has been highly successful in revitalising the Mac ecosystem, with global Mac sales rising 5.4% in the same period, significantly outperforming the broader PC market.

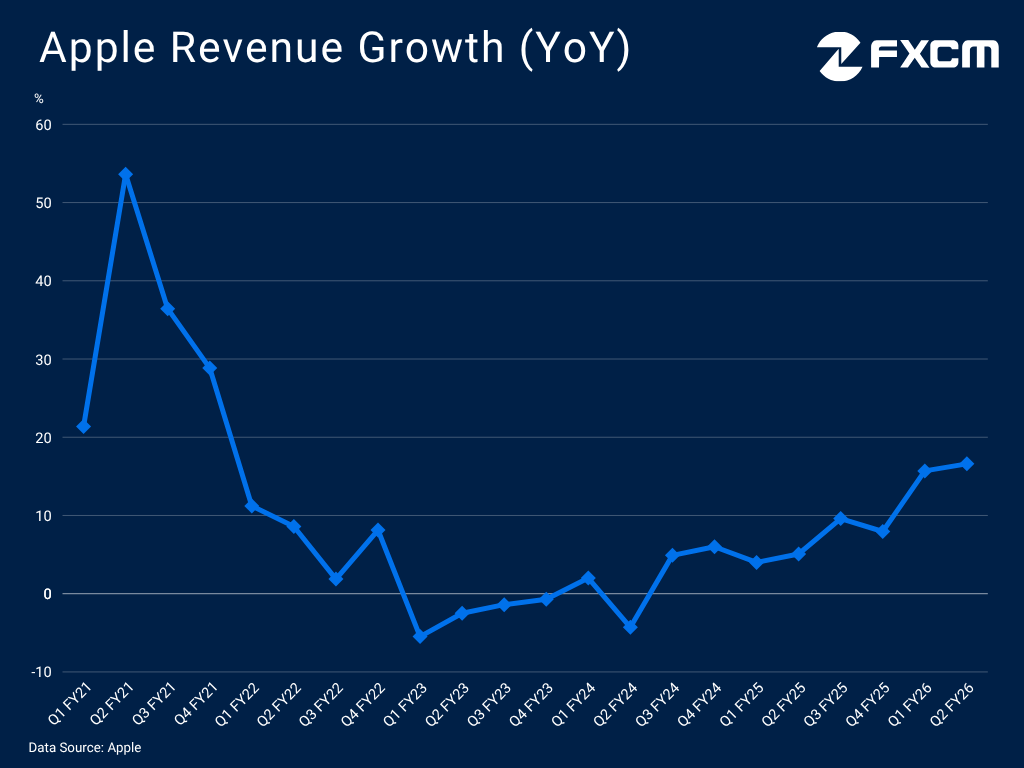

Even without a compelling AI offering, Apple is demonstrating impressive business strength, underscored by a resurgence in Greater China over recent quarters. Revenue across all geographic regions expanded by double digits in Q2 FY26, spearheaded by a standout 28.1% surge in China. Overall sales rose 16.6%, marking the company's fastest pace in more than four years. Management expects to sustain this momentum, guiding for revenue expansion of 14%-17% in the current quarter.

Complementing this hardware momentum is Apple's high-margin software ecosystem. The Services division reached a new all-time record of $31 billion during the quarter, highlighting how effectively Cupertino is expanding monetisation across its massive active user base. With Services operating at a significant profit premium relative to hardware, the segment helped lift Apple's overall gross margin to 49.3%. This steady stream of recurring subscription and App Store revenue provides a critical stabilisation mechanism for the bottom line. By combining strong global hardware demand with record-breaking, margin-expanding software monetisation, Apple enters WWDC 2026 firing on all cylinders.

Apple strength meets mounting risks

Despite Apple's momentum, the forward outlook is not without vulnerabilities. Cupertino still lags on innovation as rivals rapidly capture new product categories, underscored by Xiaomi's highly successful EV entry. At the same time, Apple's traditional health and fitness stronghold faces structural disruption as consumer preferences shift toward minimalist form factors like smart rings and screen-free wellness trackers.

On AI, the firm still has significant ground to make up and success is far from guaranteed. To deliver the long-awaited Siri revamp, Apple had to turn to rival Alphabet and its Gemini model. For a company that prides itself on full vertical integration and a walled-garden business model, relying on its primary operating system rival for its core AI brain does little to inspire long-term strategic confidence.

Meanwhile, Apple faces supply constraints and higher costs from a memory chip crunch that could contain sales and pressure profitability. Overall margins rose last quarter but product margins actually fell 200 basis points sequentially. CEO Tim Cook expects significantly higher memory costs in the June quarter and beyond, alongside reduced supply chain flexibility. At the same time, tariffs and the Middle East conflict are pushing inflation higher just as consumer sentiment weakens, an unfavourable mix for demand as stretched consumers could cut back on discretionary items like consumer electronics.

Apple stock trajectory meets the AI narrative

Apple's strong business performance is mirrored in its stock, which has gained 13.6% this year as of the May 22 close, hitting new all-time highs after the latest earnings report. China demand, new products and robust financial foundations all stand ready to propel AAPL higher, and a convincing slate of AI announcements next week could provide fresh upward impetus.

While markets have generally been patient with Apple's perceived AI lag, sentiment could quickly shift if the upcoming WWDC underwhelms. Technically, the recent rally looks extended as signalled by an overbought RSI, creating scope for a short-term correction. With macro and competitive challenges mounting, Apple may soon need to uncover its next major catalyst.

However, Apple does not necessarily need to operate on the absolute cutting edge of AI development. One could argue it is quietly winning the AI race by choosing not to play it in the same way as its peers, specifically by avoiding the eye-watering capital expenditures currently being poured into AI infrastructure by its rivals.

Chart source: www.tradingview.com

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.