Intel earnings preview: AI demand and lingering risks

Intel Q2 earnings preview - quick take

Earnings are due on Thursday July 23 2026, with Intel forecasting Q2 revenue of $13.8-$14.8 billion, which has the potential to mark the best performance in six years. The report comes as Intel's stock rises nearly 20% year-to-date, making it a top S&P 500 performer. But a lofty valuation and high expectations create a high-stakes environment that leaves little room for error.

The stock and business momentum is fuelled by the AI boom and a transition from GPU-heavy model training to CPU-orchestrated AI inference and Agentic AI, which boosts demand for Intel's products. Even so, structural risks and lingering turnaround challenges continue to loom, threatening to disrupt Intel's long-term growth trajectory.

AI proliferation drives chip growth

AI infrastructure development continues at a relentless pace as hyperscalers commit massive amounts of capital to build out the physical architecture of the future. Alphabet and Amazon.com are looking to roughly double their investments this year, while Microsoft and Meta Platforms pursue even larger increases. This aggressive expansion aligns with broader structural forecasts. Goldman Sachs estimates that cumulative global AI spending, encompassing power generation, state-of-the-art data centres and specialised compute, will more than double to exceed $1.6 trillion by 2031. [1]

This rapid scaling of physical AI infrastructure is driving unprecedented demand across the global semiconductor industry. TSMC, the world's leading foundry, raised its 2026 target again as it tries to meet supply [2]. This came as it posted a net profit jump of 77.4% y/y in Q2, following a surge in monthly revenues of 67.9% y/y in June - its best performance since 2015. ASML, another crucial chokepoint of the global semiconductor supply chain, raised its full-year guidance, expecting a sizeable increase in gross margins and an acceleration in sales growth to 31.5%-37.6%. [3]

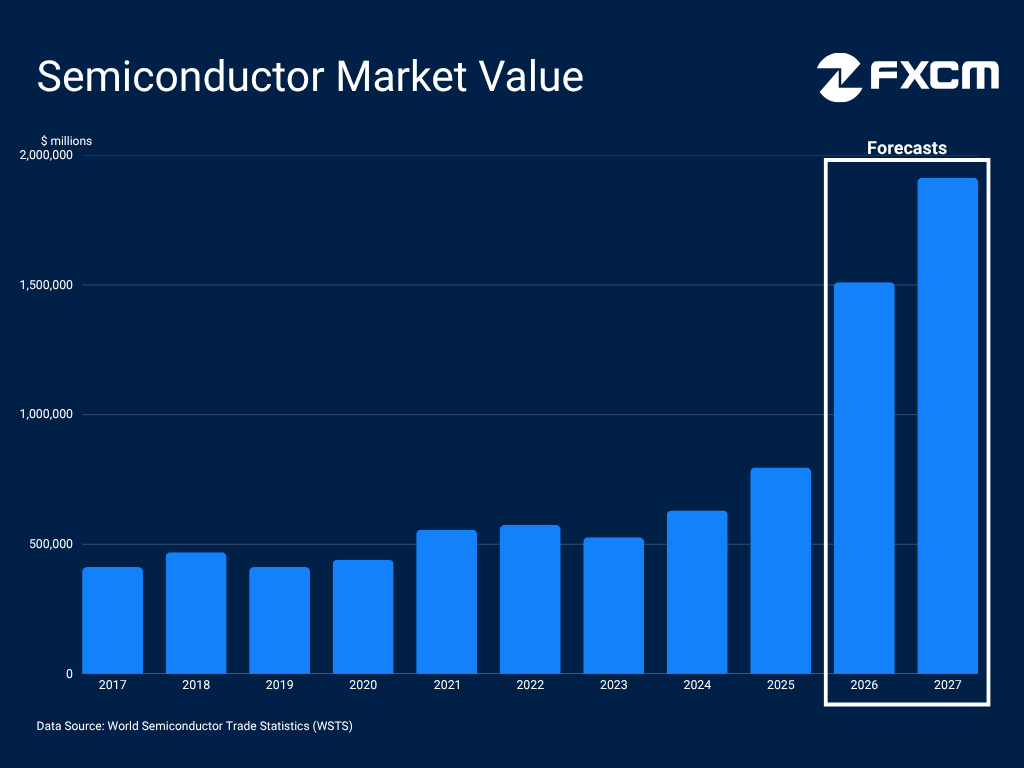

Underpinning these individual corporate successes, the World Semiconductor Trade Statistics (WSTS) projects a massive acceleration in sales. It estimates the global semiconductor market will expand this year by a massive 89.9% to reach $1.5 trillion, before climbing toward the $2 trillion threshold by 2027. [4]

Why Intel benefits from the global AI boom

Intel is uniquely positioned to capitalise on the ongoing AI expansion as the industry transitions from GPU-heavy model training to CPU-orchestrated real-time inference and Agentic AI. Gartner forecasts that enterprise spending on AI agent software will surge 139% to reach $206.5 billion in 2026 [5]. McKinsey projects that inference demand will grow 49.3% this year to match training workloads, ultimately becoming the dominant data centre workload from 2027 onward. [6]

This transition elevates the CPU to the centrepiece of AI workloads. Intel CFO David Zinsner noted during the Q1 earnings call that training clusters historically ran a ratio of 7-8 GPUs per CPU, moving to 3-4:1 for inference and hitting 1:1 with Agentic AI, "potentially even flipping in the other direction a little bit" [7]. With Intel commanding a dominant share of over 70% of the x86 processor market according to Mercury Research [8], this hardware transition naturally places the company at the heart of the industry's new expansion phase. Counterpoint Research projects this shift will expand the total addressable market for server CPUs to $110-$120 billion annually by 2030. [9]

While this architectural shift naturally plays to Intel's strengths, the company is actively going on the offensive, leveraging strategic high-profile alliances to secure its position at the epicentre of AI infrastructure. Nvidia is investing $5 billion to co-develop high-performance x86 CPUs [10], while Google is deepening its infrastructure alliance to deploy next-generation Intel Xeon processors and co-develop custom IPUs. [11]

Crucially, Intel is aggressively building out its external manufacturing wing, Intel Foundry, to establish itself as a viable domestic alternative for advanced chip fabrication. This is exemplified by the landmark deal with Elon Musk to utilise Intel's upcoming leading-edge architecture in the Terafab [12], which will produce custom silicon for humanoid robotics and robotaxis. Apple is also reportedly looking to partner with Intel to fabricate a portion of its custom silicon, a deal that President Trump recently indicated has been agreed upon. [13]

Beyond the structural shift in AI workloads, Intel's revival is supported by the US administration's push to reshore advanced chip manufacturing and increase technological independence. The US government has made an $8.9 billion investment, taking a nearly 10% stake in the company [14], providing the long-term sovereign backing needed to establish Intel's domestic fabs.

AI demand fuels a return to growth

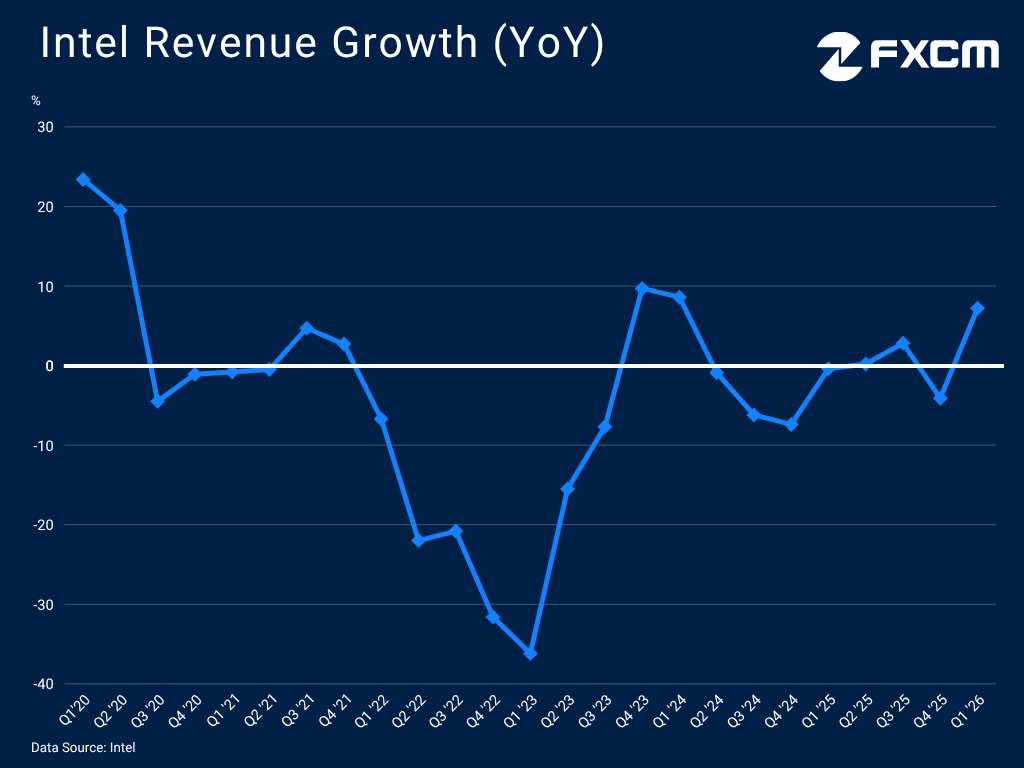

The proliferation of AI and the shifts in workloads that put CPUs at the epicentre of the physical buildout, translate directly into stronger financial results. The Foundry business accelerated with a 16% revenue growth in the first quarter and Data Centre and AI (DCAI) was the best performing sector (up 22% y/y). These were the key engines behind Intel's return to growth, with total revenues rising 7.2% y/y and the fastest pace in two years. [15]

This operational momentum is finally feeding back into the company's liquidity. While heavy upfront factory investments and one-off restructuring charges kept GAAP net income negative, Intel successfully generated $1.1 billion in cash from operations during the first quarter. This stabilization in operating cash flow provides crucial breathing room as Intel aggressively funds its domestic factory footprint.

Furthermore, with demand outstripping supply, Intel is regaining critical pricing power. Combined with aggressive cost discipline and improving manufacturing yields, this supports margins. Even though GAAP net losses persisted in Q1, gross margins climbed to 39.4%, their highest level since 2024, placing profits within reach.

Intel expects to turn profitable in the second quarter, which it reports on Thursday July 23 2026. Management has guided for GAAP diluted EPS of $0.08, even with a projected seasonal narrowing in gross margins to 37.5%. On the top line, the chipmaker forecasts revenues of $13.8-$14.8 billion. Reaching the upper bound would represent a robust 14.7% y/y growth rate, Intel's strongest revenue performance in six years.

Intel continues to face structural hurdles

Despite the turnaround gathering pace thanks to the AI boom, Intel continues to face significant hurdles. Even though it remains dominant in CPUs, its market share is steadily declining as AMD gains ground. The Foundry division continues to lose money and despite solid revenues, these are almost entirely internal rather than driven by external customers, as evidenced by offsetting eliminations. Building a foundry and attracting clients is a monumental task and Intel may find it hard to capture meaningful share from giants like TSMC.

Meanwhile, its Client Computing Group eked out only marginal growth and could continue to face headwinds as global sales struggle. Worldwide PC shipments dropped 3.6% y/y in the second quarter according to Omdia [16], largely due to supply constraints and price increases from the severe memory chip crunch. Ironically, Intel sold its NAND memory business to SK Hynix, which is now seeing explosive growth, underscoring how past strategic mistakes still weigh.

To successfully meet demand and fend off formidable competitors, Intel must scale its manufacturing output at pace. However, management has guided for flat capex in 2026 compared to a year ago, highlighting the lingering constraints of a balance sheet that, while improving, is still bound by past capital allocation decisions.

Beyond its own factories, Intel must navigate escalating threats facing the broader semiconductor industry. Geopolitical conflicts pose real-world challenges to the energy-intensive chip fabrication process and inflate the already steep costs of maintaining and expanding global AI infrastructure, potentially testing hyperscalers' resolve to keep raising capital expenditure. Tightening technology trade restrictions and complex supply chain risks add further pressure.

From survival to scaling: the stock's balancing act

Just a year ago, the prevailing narrative surrounding Intel was whether it could survive the severe risks facing its business. Today, the conversation has completely flipped. The central question is whether Intel can scale its manufacturing capacity quickly enough to meet the tidal wave of AI-driven demand.

Reflecting this profound shift in business fortunes and market sentiment, the stock is up nearly 200% year-to-date, making it one of the top SPX500 performers. With its turnaround plan finally bearing fruit and the evolving nature of AI workloads heavily favouring CPU demand, the stock remains well-positioned to extend its rally toward new all-time highs.

Chart source: www.tradingview.com

However, any advance is unlikely to be straightforward and the stock is vulnerable to declines that could test the EMA200 and the bullish outlook. The RSI divergence creates scope for such pullbacks, while fundamental risks also loom. Investors remain acutely aware of the company's tight balancing act between a costly Foundry buildout, defending CPU market share and navigating a tough macroeconomic environment that tests the bounds of the AI boom.

As Intel prepares to report its second-quarter earnings on Thursday July 23 2026, it undoubtedly has the wind in its sails. Yet the combination of high expectations, stretched valuations and residual operational risks leaves plenty of room for disappointment and sharp volatility. Wall Street will be closely scrutinising underlying profitability, tangible milestones within the Foundry business, spending targets and forward guidance. For a company that has successfully put its survival crisis in the rearview mirror, this report represents the next major test of its ability to execute, scale and permanently solidify its comeback.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.