Micron earnings preview: navigating generational demand and supply constraints

AI infrastructure buildout accelerates

The rise of inference and Agentic AI has emerged as the new inflection point for the industry, fuelling a more aggressive phase of AI proliferation that broadens demand for semiconductors and infrastructure spending. Deloitte identifies inference as the "hot new thing" for 2026, expecting it to account for roughly two-thirds of all AI compute cycles [1], while Gartner projects that 40% of enterprise applications will feature AI agents this year [2]. Confirming this momentum, the World Semiconductor Trade Statistics (WSTS) expects the chip market to maintain strong growth and rapidly approach the $1 trillion threshold. [3]

Intel is shaping up to be a key pillar of this new stage, having returned to sales growth in the first quarter of the year. Advanced Micro Devices Inc MD continues to gain significant traction, posting a 38% y/y revenue increase in Q1, its fastest pace in nearly four years [4]. Nvidia reaffirmed its leadership, announcing record revenues in Q1 FY27 and forecasting further acceleration to roughly 94% y/y in the current quarter [5]. TSMC, which fabricates the advanced silicon designed by Nvidia and its peers, posted a 35.1% y/y revenue jump. Driven by what CEO C.C. Wei described as "extremely robust" AI demand, TSMC is now aiming for the upper bound of its $52-56 billion capex target. [6]

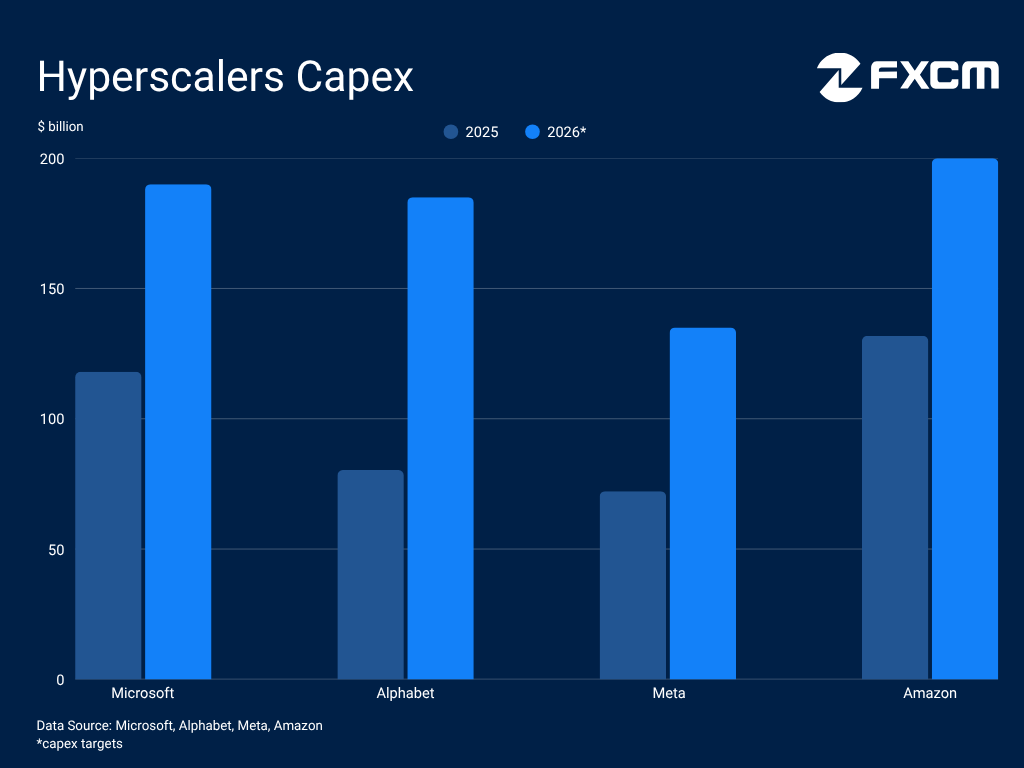

Hyperscalers are similarly reaping the benefits and driving this surge, pouring vast sums into building the infrastructure required to power this proliferation. At the same time, they are developing custom silicon, a move shifting massive capital and unlocking new growth avenues across the semiconductor supply chain. Alphabet posted record cloud revenue growth of 63.4% y/y in the first quarter while roughly doubling its spending target for the year. Amazon.com is targeting a 50% increase in capital expenditures, Microsoft is aiming for 61% and Meta Platforms is looking at a similarly aggressive expansion rate.

AI proliferation drives memory demand supercycle

The massive data centre buildout required to power this next phase of AI expansion is aggressively scaling demand for advanced storage and memory solutions. Phison Electronics, a specialised memory-logic firm and Micron partner, recently highlighted this shift, noting that "Agentic AI workloads demand more memory than traditional AI, especially when running locally". [7]

This computational appetite is triggering severe market shortages and driving acquisition costs rapidly higher. In a recent Bloomberg interview, Micron CEO Sanjay Mehrotra noted that the supply crunch will persist well beyond the current calendar year [8]. Gartner expects the global scarcity of DRAM and NAND flash storage to last even longer, while projecting price inflation of 80% and 202% respectively over the course of 2026. [9]

However, not all memory architectures are created equal, and High Bandwidth Memory (HBM) has established itself as the ultimate gatekeeper of the AI boom. McKinsey projects a 13% compound annual growth rate for the broader semiconductor market from 2024 through 2030, with the vast majority of growth concentrated in leading-edge chips and HBM. Specifically, McKinsey forecasts a 20% CAGR for HBM, vastly outstripping the growth trajectories of standard DDR DRAM (12%) and NAND (9%). [10]

Micron reaps the benefits of the memory crunch

Micron is not just another memory and storage firm but one of only three HBM makers globally, placing it in exceptionally rare air among semiconductor firms. The company has already commenced volume shipments of its latest 36GB 12-Layer HBM4, designed specifically for Nvidia's upcoming Vera Rubin architecture, the industry's most advanced AI platform. Simultaneously, next-generation HBM4E is already under deep development with a volume ramp expected in 2027, underscoring Micron's relentless pace of technological advancement. [11]

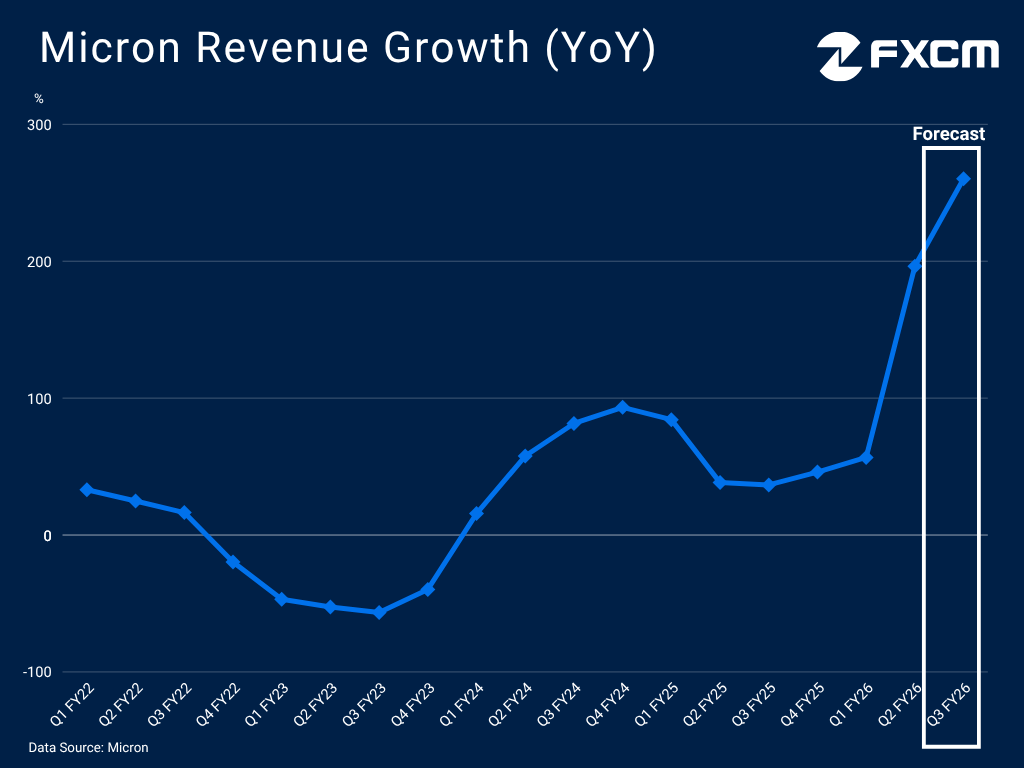

Because HBM is facing the most severe shortages in the entire hardware ecosystem, it has granted Micron unprecedented forward visibility and substantial pricing power. This dynamic translates directly into record-breaking top and bottom lines. Gross margins climbed to 74.4% in Q1 FY26, earnings per share soared 756% and sales nearly tripled to $23.86 billion in the quarter ended February 27 (Q2 FY26). Management expects further acceleration in Q3 FY26, reported on Wednesday June 24, underscoring Micron's blistering growth momentum and unique position in the AI infrastructure buildout.

Memory makers face intense competition

While memory and storage makers are reaping the rewards of unprecedented demand, the tier-one landscape remains a cutthroat battlefield. The stakes for the Big Three HBM titans, SK Hynix, Samsung and Micron, have intensified significantly following SK Hynix's multi-year technology partnership with Nvidia [12]. Announced specifically to co-develop next-generation memory tightly aligned with Nvidia's hardware roadmap, the pact embeds SK Hynix directly into the architecture for Vera Rubin AI supercomputers.

This deep architectural integration could solidify the dominant market position of the South Korean giant. According to Counterpoint Research, SK Hynix captured a commanding 58% share of the HBM market in the first quarter, leaving Micron and Samsung fighting neck-and-neck for the remaining volume [13]. Consequently, Micron has little margin for error. The company must execute flawlessly on its product ramps, as any drop in yields or inability to scale quickly would lead Nvidia to lean harder on its primary partner or pivot to Samsung, which is aggressively spending tens of billions on R&D to solve its packaging bottlenecks.

The Micron-SK Hynix rivalry is about to enter a new phase as the latter has filed for a US IPO [14] that could come as early as within summer. The listing will allow the Korean firm to tap into a new pool of capital to fund its aggressive global capacity expansion, directly threatening Micron's ability to keep pace in the high-stakes HBM race, where the advantage belongs to whoever can scale production fastest.

Operational risks loom despite soaring demand

To scale capacity and meet this unprecedented wave of AI demand, Micron has embarked on an aggressive, highly capital-intensive manufacturing expansion. It targets an 80% y/y jump in spending in the current fiscal year to over $25 billion, while expecting at least a $10 billion increase in construction-related capex in FY27 and higher equipment spend. Despite this massive allocation of capital, building semiconductor facilities is a time-consuming process, and Micron's CEO does not see a real ramp for the industry until 2028. [8]

This lag, combined with eye-watering infrastructure costs, creates a trio of business risks that could worry market participants. The most immediate danger is an execution mismatch: Micron risks failing to scale quickly enough during the peak of the current cycle, effectively leaving money on the table for rivals to capture. Conversely, these investments place a burden on the firm's balance sheet and cash flow. The ultimate structural risk, however, is a potential turn of the semiconductor pendulum, whereby this aggressive capacity race may eventually lead to oversupply. Adding to these concerns over future demand is recent research from Google on a new compression method that makes AI models more efficient, requiring less memory as a result.[15]

Micron has to walk this operational tightrope against a highly volatile macroeconomic backdrop. The energy shock from the Middle East conflict is raising input costs that constrain margins while threatening energy-intensive manufacturing. Simultaneously, persistent global economic headwinds threaten to soften consumer-facing electronics demand and test hyperscalers' capex commitments, while escalating trade restrictions between major economic blocs add further friction to Micron's global supply chain.

The earnings tightrope: translating scarcity into stock returns

Unprecedented demand and explosive financial metrics have translated directly into a surge in its stock. MU is up more than 250% year-to-date, standing as one of the top SPX500 performers. It is also among the most traded stocks at FXCM. The structural reality of the data centre buildout is upending the traditionally cyclical, boom-and-bust nature of the memory industry, creating a multi-year growth runway for Micron. Backed by a powerful market rotation toward memory and storage makers, Micron's shares are well positioned to extend their record-breaking rally.

Chart source: www.tradingview.com

However, pitfalls loom for Micron's business amid cutthroat competition and operational risk against a challenging external environment, creating scope for near-term declines in the stock. Meanwhile, the expected US IPO of rival SK Hynix means Micron will soon lose its status as Wall Street's only HBM play, as the memory and storage trade may already be getting crowded. When the Korean heavyweight arrives on US exchanges, it will trigger a battle for institutional capital, giving investors a direct alternative to Micron and introducing a new headwind to domestic equity flows.

The most immediate and high-stakes test, however, arrives on Wednesday June 24. Sky-high expectations and a lofty valuation mean even a glowing Q3 FY26 earnings report could underwhelm markets and push the stock lower, a pattern that had played out after the previous quarterly report.

Beyond core financials, capex guidance will once again be a key focal point. Any increase in spending targets may spark fresh concerns, although Micron may find a more forgiving audience this time around amid optimism over a US-Iran deal. A successful resolution and a sustained reopening of the Strait of Hormuz could lower baseline cost pressures and ease broader supply chain risks, potentially allowing the market to better absorb Micron's massive capital roadmap.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.