GBP/USD Eases the Post-US CPI Rally as UK Inflation Also Decelerates

GBP/USD Analysis

Tuesday's data showed progress on US inflation as the all-inclusive CPI was unchanged in October over the prior month and increased by 3.2% y/y. This was a notable deceleration from a recent resurgence, helped by the decline in energy and energy services prices. Core CPI ticked down to 4% y/y, in the smallest increase in a year.

These figures are definitely in the direction the Fed wants and reinforce expectations for peak rates. Markets had never embraced the one-more hike forecast and yesterday's report brought forward bets around the timing of rate cuts. CME's FedWatch Tool assigns the highest probability that materializing in May, from June previously. [1]

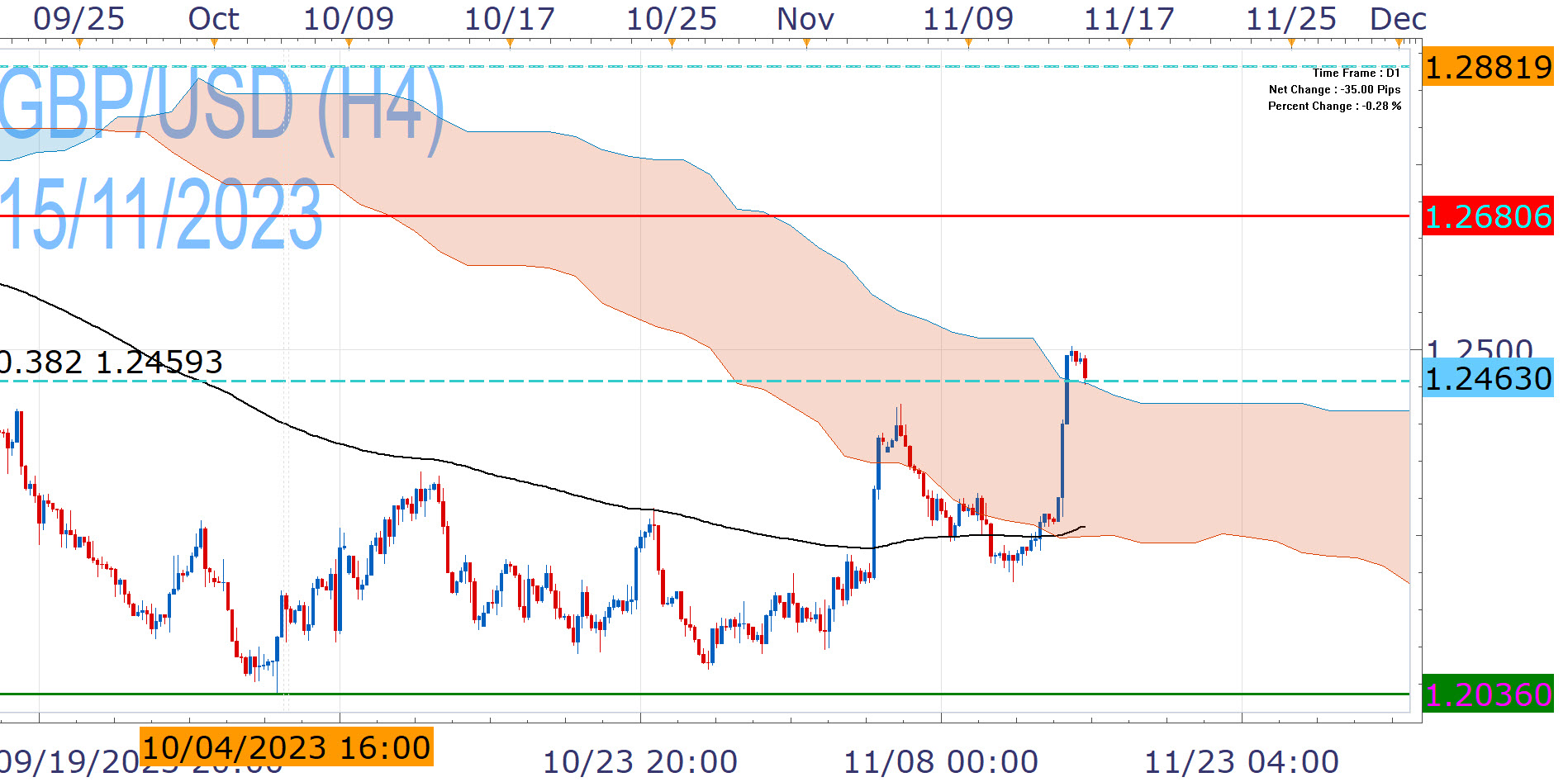

The greenback fell as a result and GBP/USD posted its best day in a year on Tuesday, breaching key technical hurdles. The rally brings 1.2680 in the spotlight, but we are still cautious around the ascending prospects.

The move is stretched and the pair slides after the inflation update from the UK, which showed significant deceleration. Headline CPI of 4.6% y/y is the lowest in two years, while Core of 5.7% marked the smallest increase since March 2022. The report lowers the need for further tightening by the BoE, which has stayed on the sidelines for the past two minutes, as it tries to balance between restoring price stability and not doing unnecessary damage to already weak economy.

As such, there is scope for further pressure back towards the 200EMA and the lower border of the daily Ichimoku Cloud (around 1.2250). However a strong catalyst would be needed for daily closes below it that would pause the upside bias, while 1.2036 seems distant at this stage.

This week's soft inflation figures raise the bar for further rightening, but monetary policy is at intricate and uncertain phase. The two central banks are unlikely to declare victory yet and there are reason for a prolonged restrictive stance and potentially more hikes. In both cases, inflation is still far from target and has surprised to the upside in the past. In the Fed's case, strong economy and tight labor market don't bode well for the peak rates scenario.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 30 Jun 2026 https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.