Micron post-earnings slide deepens but structural tailwinds remain

Micron analysis

Micron posted blockbuster earnings last week, but the stock has been sliding since, primarily due to fresh concerns over spending. To meet demand for memory chips driven by the AI boom, management raised its spending plans. It expects capex to grow over 80% year-on-year to $25 billion in the current fiscal year ending August, and to add at least another $10 billion in FY27 to build out its manufacturing capacity. [1]

However, this did not sit well with investors who have already shown concern about ballooning AI spending in a cyclical market against a highly uncertain macro backdrop. The Middle East conflict plays into these concerns as it disrupts trade and energy flows, stoking a surge in oil and gas prices. This poses real risks for an energy-intensive industry that relies on intricate supply chains. Making matters worse, demand worries have emerged following research from Google on a new compression method that makes AI models more efficient, requiring less memory as a result. [2]

Spending concerns and creeping demand fears add to broader headwinds from the Middle East conflict, which have led to de-risking and a flight to safety, pushing the SPX500 lower since the start of hostilities. This exacerbates pressure on Micron's stock, leaving it vulnerable to deeper declines.

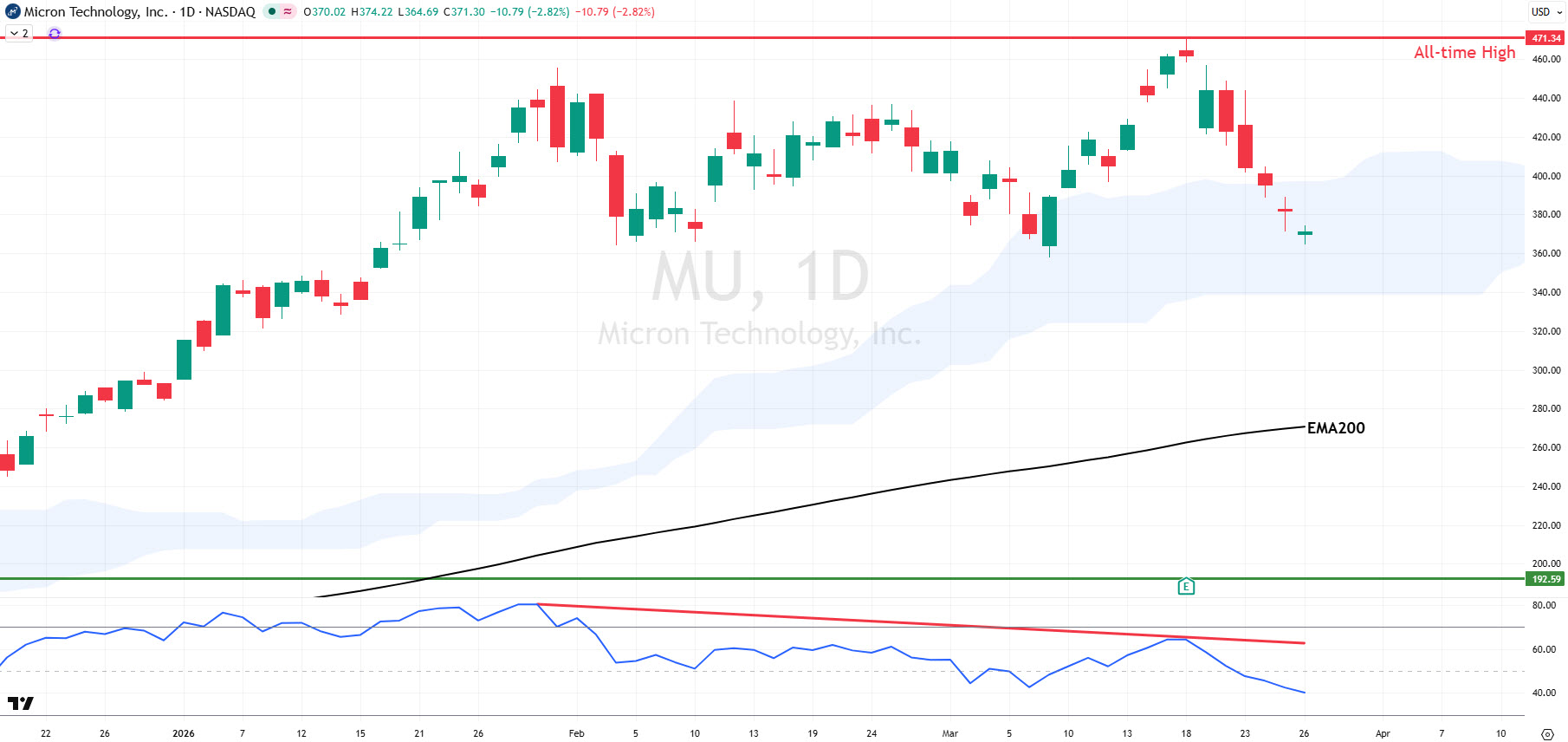

Technically, there is room for further weakness that could test the EMA200 and challenge the bullish bias, as the Relative Strength Index (RSI) diverges lower and breaks below the 50 mark. Nonetheless, the lower border of the Ichimoku Cloud provides the first line of support, and above the EMA200 the bullish bias remains intact with the road to new all-time highs open.

Chart source: www.tradingview.com

The business outlook also favours further stock upside. Fears over demand for Micron's products appear overblown. Greater computing power and further AI proliferation could lead to larger inference loads requiring more chips.

Moreover, tech giants like Meta Platforms and Microsoft are ramping up investments to build out AI infrastructure. Micron is uniquely positioned to benefit as one of only three high bandwidth memory makers alongside Samsung and SK Hynix, with shortages driving significant pricing power.

This was reflected in the blockbuster results, driven by continued demand for Micron's memory and storage solutions. Revenues nearly tripled and gross margins widened to 74.7% in Q2 FY26, with the firm expecting to maintain strong growth momentum into the current quarter. [3]

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

These materials constitute marketing communication and do not take into consideration your personal circumstances, investment experience or current financial situation. The content is provided as general market commentary and should not be construed as containing any type of investment advice, investment recommendation and/or a solicitation for any investment transactions. This market communication does not imply or impose an obligation on you to perform an investment transaction and/or purchase investment products or services. These materials have not been prepared in accordance with legal requirements designed to promote the independence of investment research and are not subject to any prohibition on dealing ahead of the dissemination of investment research.

FXCM, and any of its Affiliates, shall not in any way be liable to you for any inaccuracies, errors or omissions, regardless of cause, in the content of these materials, or for any damages (whether direct or indirect) which may arise from the use of such materials, services and their content. Consequently, any person acting on them does so entirely at their own risk. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.