Top 10 Stocks for Q2 2026 – Part 2

Stagflation risks as the Middle East conflict reshapes markets

The second quarter and the new earnings season arrive against a highly volatile backdrop. A US-Israel military campaign against Iran and the latter's counterstrikes across the region have pushed energy prices sharply higher. This has stoked stagflation fears - the toxic combination of slowing growth and rising inflation that central banks are ill-equipped to tackle simultaneously. Major central banks, already navigating stubborn price pressures, generally shifted to a more hawkish stance in March, raising the spectre of higher interest rates for longer.

The headwinds do not stop there. Stretched equity valuations, geopolitical flashpoints and a shifting monetary policy landscape all compound the challenge for global markets, just as tariff uncertainty lingers. The Supreme Court struck down President Trump's sweeping IEEPA-based tariffs 1, only for the administration to immediately reimpose a 10% global levy under alternative statutory authority 2 - leaving trade policy as unpredictable as ever and its economic consequences far from resolved.

The turbulence can also affect the AI narrative, as surging energy costs threaten the economics of power-hungry data centres and chip fabrication. Alongside ongoing macroeconomic uncertainty, concerns over massive spending could resurface. Investors have already become more selective around AI winners and losers, making the theme less straightforward.

However, the AI tailwind remains strong and can continue to support markets. Hyperscalers like Meta and Google are ramping up investment, chipmakers like TSMC point to sustained demand and the World Semiconductor Trade Statistics (WSTS) expects semiconductor sales to grow further in 2026 following a record 2025. 3

Global equity markets have shown a remarkable ability to look through disruption and the economic fallout from the Middle East conflict may yet prove temporary rather than structural. FactSet expects S&P 500 earnings to grow 13% year-on-year in the first quarter of 2026 4 - marking the sixth consecutive quarter of double-digit growth, a testament to corporate America's enduring ability to navigate adversity.

As the second quarter gets underway amid heightened uncertainty, we turn our attention to stocks likely to draw investor focus in the coming months. In the second instalment of a two-part series, we examine companies from diverse sectors, but all tied to the AI boom. A tech behemoth pushing the envelope, a memory chipmaker enabling its proliferation and a smartphone maker lagging in the AI race. Adding to the mix, an industrial and a mining giant that benefit from the AI buildout and the need for critical minerals. You can read Part 1 here.

Alphabet

The parent company of Google is one of the largest and most valuable technology companies in the world. Its market cap hovers above $3 trillion, placing it behind just Apple and Nvidia. Its products are woven into daily life - from Google Search and YouTube to Google Maps and the Gemini AI assistant - while its enterprise cloud platform is a staple in the industry. Alphabet is also a leader in robotaxis with Waymo.

The tech behemoth was caught off guard by the ChatGPT launch that ushered in the AI era and needed time to offer a credible response. But Alphabet is spending vast sums to ensure it moves into the driver's seat. It raised its 2026 capex target to between $175 billion and $185 billion to "meet customer demand and capitalise on the growing opportunities" according to CEO Sundar Pichai. 5

Those efforts are bearing fruit. The launch of Gemini 3, which enables more powerful reasoning at lower cost, was very well received. Furthermore, its Ironwood custom AI chips 6 can increase self-reliance and offer a credible alternative to Nvidia. Progress is also evident in the financial results, with sales and profits growing substantially in 2025 on strong performance in cloud and advertising. 7

Nonetheless, challenges loom. The economic fallout from the Middle East can weigh on advertising spend and Alphabet's financials. This can in turn intensify questions over the massive investments. The AI story is also becoming less straightforward, with markets increasingly selective about winners and losers and focus shifting from companies funding AI infrastructure to those building and powering it.

Shares of Alphabet are among the most traded stocks this year at FXCM. They are down weighed by the aforementioned headwinds, testing pivotal technical levels, leaving them vulnerable to deeper corrections. Nonetheless, the decline is technically stretched based on the oversold RSI, which could lead to a rebound and set the stage for fresh record highs. Alphabet is now a leader in AI and can continue to reap the benefits.

Chart source: www.tradingview.com

Micron Technology

Micron is a leading designer and manufacturer of memory and storage semiconductors, playing a critical role in enabling AI, cloud computing and data-intensive applications. It is one of only three global producers of High Bandwidth Memory (HBM), alongside Samsung and SK Hynix. Headquartered in the United States, Micron operates a global network of manufacturing and R&D facilities.

AI models are becoming more powerful and more widely deployed, with every step up in capability demanding more memory and storage. Hyperscalers are pouring hundreds of billions into data centre buildout, driving demand for the products of companies like Seagate, Western Digital and Micron and sparking supply shortages. Micron's HBM portfolio puts it on the leading edge and in a unique position to benefit from this crunch, driving demand visibility and pricing power.

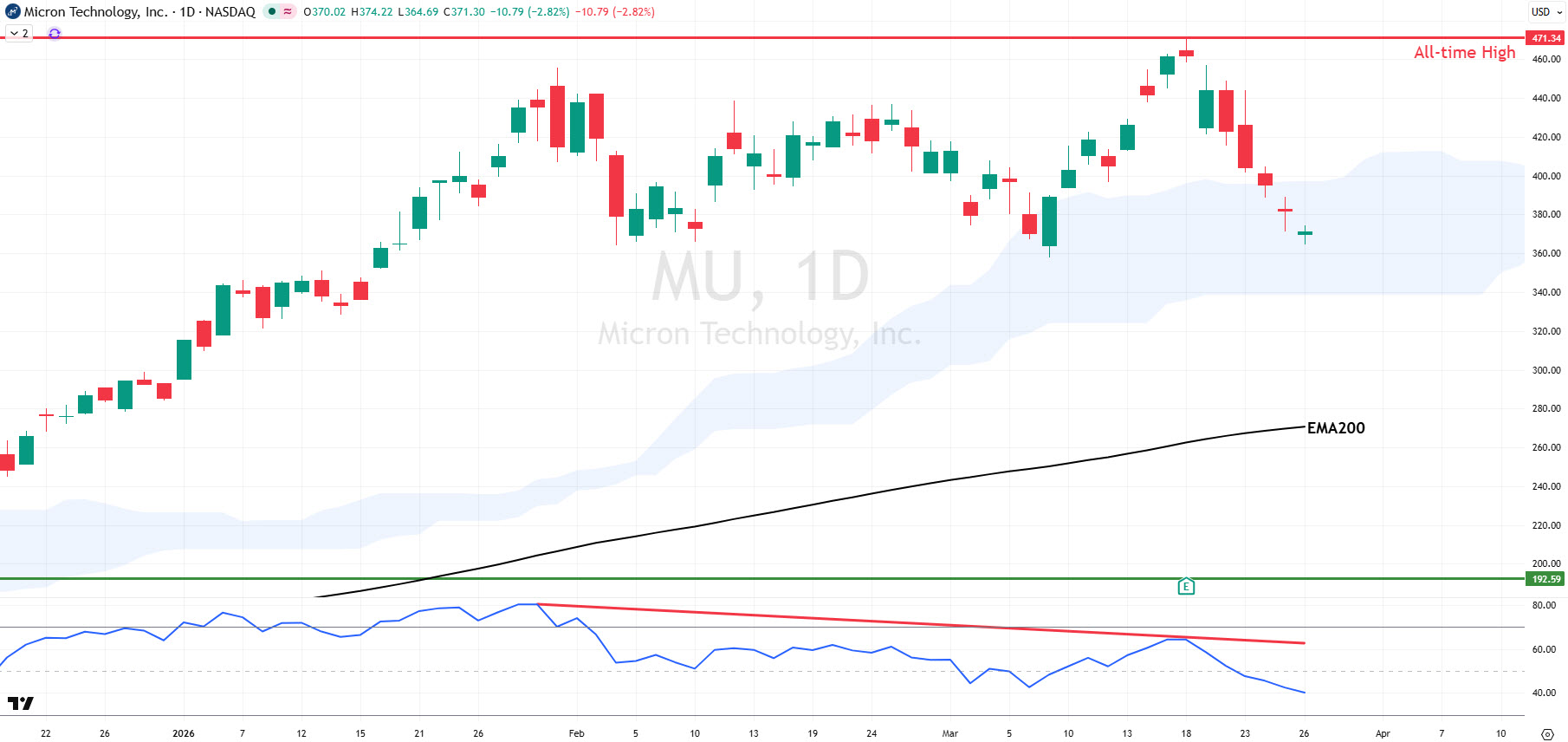

This was evident in its explosive results for Q2 FY26. Revenues nearly tripled to $23.86 billion, gross margins widened to 74.7% and net income jumped to $17.78 billion. What is more, management expects to maintain momentum in the current quarter. In order to meet demand, Micron needs to ramp up its capacity and spending, targeting capex growth of 80% y/y this fiscal year and expecting to add at least another $10 billion in FY27.

However, increasing investments in a highly competitive and cyclical industry raise concerns. This is especially true as the Middle East conflict creates hurdles for energy-intensive chip manufacturing that relies on intricate supply chains. Moreover, a recent compression breakthrough by Google has raised memory demand concerns.

These developments have put pressure on the stock of Micron (MU), which has been declining since its explosive earnings, creating scope for bigger pullbacks. But such spending fears are overblown given the eye-watering growth, and demand worries are overstated amid ongoing AI proliferation. The bullish business outlook stands firm and can continue to fuel the stock's rally to new records.

Chart source: www.tradingview.com

Apple

This is one of the most valuable companies in the world, with a market capitalisation in excess of $3 trillion. It is among the largest smartphone makers globally, with an installed base exceeding 2.5 billion active devices. It is renowned for a seamless and sticky ecosystem of hardware, software and services.

Apple reported a blockbuster holiday quarter (Q1 FY26), with revenue jumping 15.7% y/y - marking the fastest pace in more than four years. This was driven by the best ever iPhone quarterly performance, a surge in China sales and ongoing India demand. The latest iPhone is performing very strongly, while the new more affordable MacBook Neo and other new products can support demand ahead. The company expects to maintain its strong growth momentum in Q2 FY26, with CFO Kevan Parekh guiding for an increase of 13-16% y/y. 8

However, challenges loom. Memory chip shortages driven by AI demand are pushing component costs and prices higher. Apple CEO Tim Cook warned of "a bit more of an impact" on gross margins in the soon-to-be-reported quarter. IDC forecasts a substantial drop in global smartphone sales this year due to this crunch 9, while the Middle East conflict and the energy shock can exacerbate headwinds.

Apple's lack of innovation continues as rivals make progress - Samsung and others push new wearable form factors, while Xiaomi rides the success of its EV business. Crucially, Apple is a laggard in AI and, to break the stalemate, has had to resort to rival Android maker Alphabet and its Gemini AI model to power the long-delayed Siri revamp. 10

Still, this quarter's June WWDC conference could bring meaningful updates on this front. With deep pockets and access to vast user data, Apple can still make progress in AI. Importantly, it may not need to be at the bleeding edge - its enormous user base, coupled with its entrenched ecosystem, can sustain demand regardless.

Shares of Apple dropped in March as the Middle East conflict added to tariff headwinds can weigh on the business and demand, while its AI lag remains a drag. The breach of the EMA200 creates risk of larger corrections. Despite lingering challenges, Apple's financial position makes it resilient. The last report showcased durable demand and any signs of AI progress could lift sentiment and push AAPL to new all-time highs.

Chart source: www.tradingview.com

Caterpillar

Founded 100 years ago and headquartered in Irving, Texas, Caterpillar is a leading manufacturer of construction and mining equipment, industrial gas turbines and diesel-electric locomotives. It has over 500 locations across the world and more than 115,000 employees.

As hyperscalers like Meta and Alphabet continue to increase their investment to build data centres and support AI proliferation, companies across chip making, utilities and industrials reap the benefits. Caterpillar is a beneficiary of this boom, seeing increased demand for its Power & Energy solutions, with segment sales rising 13.5% in 2025 and driving the company's return to revenue growth. Meanwhile, demand for gold and critical minerals like silver and copper - driven by AI, cleantech and ballooning defence budgets - can support mining activity and the Resource Industries business. 1

Caterpillar is well positioned for continued growth, amid an AI boom, US onshoring, a record backlog and good sales visibility. An all-time high in January for new US equipment demand, according to the Equipment Leasing and Finance Association 12, adds further confidence. Management expects an acceleration in revenues this year, coupled with higher operating margins.

Not all is rosy though. The company took a $1.7 billion hit from tariffs in 2025, leading to lower profits, with pressures expected to continue this year. Moreover, the economic fallout from the Middle East conflict can hurt demand and create cost pressures, adding fresh profit headwinds. President Trump's public call on Caterpillar and other equipment makers to cut prices for farmers 13 adds a further layer of political risk to an already challenging margin outlook.

Shares of Caterpillar declined in March as the macro outlook darkened from the Middle East conflict and the energy shock. CAT is vulnerable to the 38.2% Fibonacci level and the EMA200, which if breached could open the door to a greater drop. However, above this pivotal support confluence, the bullish bias is intact and the path of least resistance points towards new all-time highs. The AI boom can continue to drive business and stock growth.

Chart source: www.tradingview.com

Newmont

Among the largest mining companies in the world, Newmont is primarily focused on gold, with output of 5.9 million ounces in 2025. It also produces silver, copper, lead and zinc. Headquartered in Denver, it operates twelve sites across multiple countries and employs approximately 17,500 people.

Newmont had an impressive 2025 with higher revenues, profits and cash flow, while debt declined. This was driven by an effort to become leaner and more efficient via cost reductions and divestitures, as well as higher metal prices. That was fuelled by a mix of risk aversion amid trade and geopolitical uncertainty and demand for crucial minerals used in the AI boom, the defence industry and the clean energy transition. 14

These demand and price drivers, alongside Newmont's strong financial position, set the stage for continued momentum this year. US tech giants like Meta and Alphabet and chipmakers like TSMC are increasing their spend, the shift to renewables carries on despite risks and military budgets in the US and Europe are rising. At the same time, demand for gold is underpinned by structural tailwinds from currency debasement trends and diversification away from the US dollar.

However, the growth path is not straightforward, with the firm expecting somewhat higher costs in 2026 and another decline in output. Prices of gold, silver and copper dropped in March after the Middle East conflict began, and the global economic fallout could curb demand - creating further challenges.

Shares of Newmont fell in March in line with the decline in precious metals and critical minerals, leaving it vulnerable to deeper declines. Nonetheless, NEM is defending the EMA200, maintaining its upside bias and the ability to set new records. Demand from the crucial industries driving the global economy can continue to spur business growth.

Chart source: www.tradingview.com