Top 10 Stocks for Q2 2026 – Part 1

Stagflation risks as the Middle East conflict reshapes markets

The second quarter and the new earnings season arrive against a highly volatile backdrop. A US-Israel military campaign against Iran and the latter's counterstrikes across the region have pushed energy prices sharply higher. This has stoked stagflation fears - the toxic combination of slowing growth and rising inflation that central banks are ill-equipped to tackle simultaneously. Major central banks, already navigating stubborn price pressures, generally shifted to a more hawkish stance in March, raising the spectre of higher interest rates for longer.

The headwinds do not stop there. Stretched equity valuations, geopolitical flashpoints and a shifting monetary policy landscape all compound the challenge for global markets, just as tariff uncertainty lingers. The Supreme Court struck down President Trump's sweeping IEEPA-based tariffs 1, only for the administration to immediately reimpose a 10% global levy under alternative statutory authority 2 - leaving trade policy as unpredictable as ever and its economic consequences far from resolved.

The turbulence can also affect the AI narrative, as surging energy costs threaten the economics of power-hungry data centres and chip fabrication. Alongside ongoing macroeconomic uncertainty, concerns over massive spending could resurface. Investors have already become more selective around AI winners and losers, making the theme less straightforward.

However, the AI tailwind remains strong and can continue to support markets. Hyperscalers like Meta and Google are ramping up investment, chipmakers like TSMC point to sustained demand and the World Semiconductor Trade Statistics (WSTS) expects semiconductor sales to grow further in 2026 following a record 2025. 3

Global equity markets have shown a remarkable ability to look through disruption and the economic fallout from the Middle East conflict may yet prove temporary rather than structural. FactSet expects S&P 500 earnings to grow 12.5% year-on-year in the first quarter of 2026 4 - marking the sixth consecutive quarter of double-digit growth, a testament to corporate America's enduring ability to navigate adversity.

As the second quarter gets underway amid heightened uncertainty, we turn our attention to stocks likely to draw investor focus in the coming months. In this first instalment of a two-part series, we examine five companies across diverse sectors. These include energy, defence and aviation firms with direct exposure to geopolitical developments, alongside tech giants of perennial interest.

Netflix

The firm started out in 1997, renting and selling DVDs, and introduced streaming services ten years later. Netflix popularised binge-watching, led the streaming revolution and remains the market leader despite rising competition. It reaches more than 190 countries in 50 languages.

The second quarter begins just as Netflix pulled back from a bid to acquire Warner Bros, following a superior proposal from Paramount Skydance - a development that could shape its future. The withdrawal deprives Netflix of a potential growth catalyst, as it loses the opportunity for an intellectual property boost and an influx of new subscribers. The tie-up would also have expanded its advertising footprint and leverage as it builds its ad-supported tier. Furthermore, it misses a chance to strengthen its presence in traditional Hollywood, while a Warner-Paramount merger could create another strong rival alongside Disney.

On the other hand, markets never fully embraced the deal and the stock gained after the withdrawal. The streaming giant avoids tens of billions in new debt that could have shaken investor confidence in a challenging environment. It will also resume its repurchase programme, returning value to shareholders. Netflix can now remain focused on its core business, steering clear of regulatory scrutiny and the complexities of integrating such a large operation.

The strategic pivot towards ad-supported subscription tiers is progressing and can support continued momentum. The firm is expanding its capabilities and expects advertising revenue to double this year 5. Growth in live sports programming supports this strategy, as such events can lift engagement and subscriptions while strengthening advertising power.

Shares of Netflix have had a mixed year amid ongoing challenges and the technical Death Cross (EMA50 < EMA200) keeps the stock vulnerable to deeper declines. Nonetheless, its strategic initiatives and relative resilience to macro headwinds can sustain growth. The stock is rebounding following the Warner development and a move back above the EMA200 would negate the bearish bias.

Chart source: www.tradingview.com

Exxon Mobil

This is the largest US energy company and among the biggest globally by sales and market capitalisation. It generated revenues of over $330 billion in 2025 and its market cap stands at approximately $650 billion. A vertically integrated oil major, it explores for and refines crude oil and natural gas, while producing fuels, lubricants and petrochemicals. It has a global presence with around 58,000 employees.

The US oil and gas industry benefits from favourable policy shifts under President Trump, who is committed to fossil fuels and rolling back clean energy initiatives of his predecessor. Shortly after taking office, he signed the "Unleashing American Energy" executive order order 6, fast-tracking project permits and removing EV mandates. The US also withdrew from the Paris Agreement again 7 and repealed the EPA Endangerment Finding - the legal basis for greenhouse gas regulation, including vehicle emission standards 8.

Moreover, President Trump called on oil companies to build up Venezuela's infrastructure following the military operation that removed Maduro, creating a significant opportunity. Meanwhile, strikes against Iran have caused supply disruptions, tightening markets and driving a surge in oil and gas prices. This can boost Exxon's top and bottom lines and support the stock, which hit new all-time highs during the Middle East conflict.

However, persistently high oil prices, combined with macroeconomic uncertainty, could eventually lead to demand destruction that would hurt the industry. The opening up of Venezuela may benefit rival Chevron more, given its existing presence there. Rebuilding will require significant investment and carries risks, with CEO Woods describing the country as currently "uninvestable" 1, drawing criticism from President Trump who threatened to exclude Exxon. 10.

Furthermore, recent consolidation trends suggest energy companies may have limited appetite for costly exploration when they can expand through M&A and keep investors happy with dividends. President Trump's pro-drilling stance has weighed on oil prices and if current supply disruptions ease, the bearish fundamental outlook could return, with the IEA still expecting supply to outstrip demand this year 1.

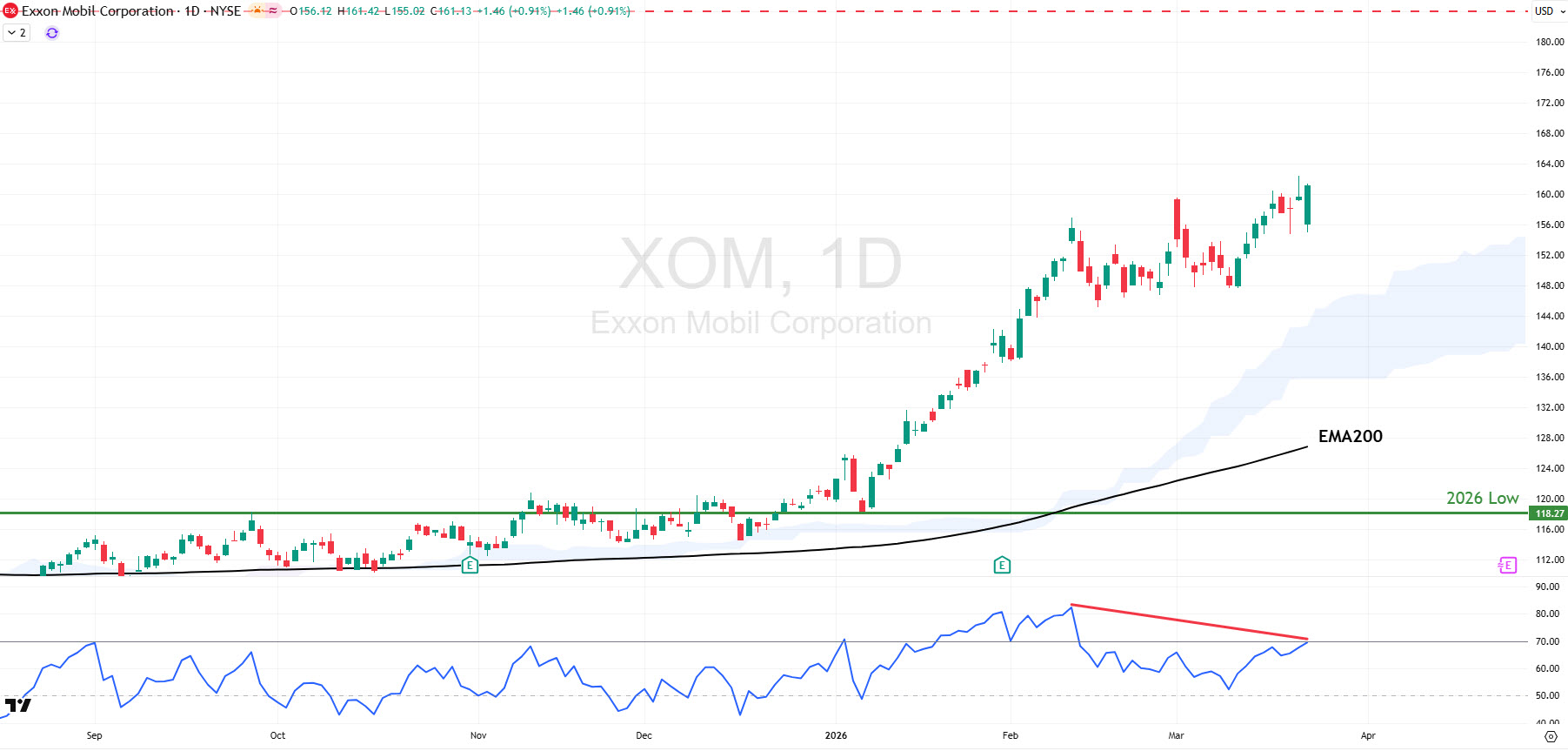

Shares of Exxon Mobil made a strong start to the year, reaching record highs after the strikes on Iran began. Supply disruptions, higher prices and supportive policy shifts can continue to drive gains. Conversely, an end to the conflict and the restoration of supply could create downside risks, as prices ease and oversupply concerns re-emerge. Technically, the RSI divergence suggests scope for pullbacks towards the EMA200, which would test the bullish outlook.

Chart source: www.tradingview.com

Delta Air Lines

Delta is one of the world's largest airlines, serving over 300 destinations across six continents. It operates up to 5,500 daily flights, carrying more than 200 million customers annually. The company is headquartered in Atlanta, Georgia, and was founded in 1925, adopting its current name three years later.

Delta Air Lines comes off a strong 2025, largely driven by its successful premiumisation and loyalty-focused strategy, which helps offset macroeconomic pressures. Total revenue grew 2%, supported by premium tickets and loyalty programmes, despite declines in the main cabin segment 12. This provides a solid foundation for continued momentum, with the company expecting 20% earnings growth this year and higher revenue in the current quarter. 13.

However, these results were also supported by lower fuel costs last year, while the recent surge in oil prices could weigh on profitability, with CEO Bastian noting a $400 million hit in March. Heightened geopolitical tensions also disrupt travel, an issue that has persisted in recent years. Although conditions improved in 2025, Cirium's latest report shows a 139% rise in US flight cancellations in January.14

Moreover, lingering macroeconomic uncertainty from tariffs and inflationary pressures may weigh on demand. At the same time, the United States appears to be turning into a less appealing destination, with overseas visitors falling 2.5% y/y last year, according to the US International Trade Administration. 15

Shares of Delta Air Lines made a weak start to the year and may remain under pressure amid macro uncertainty and fresh risks from the Middle East conflict. Nonetheless, demand remains resilient, its strategy is delivering and management expects growth this year. This has supported a rebound, putting the stock back on track for new all-time new highs.

Chart source: www.tradingview.com

Lockheed Martin

This is the world's largest defence company according to SIPRI16, with over 350 facilities worldwide and more than 120,000 employees. Its portfolio includes high-profile products such as the F-35 fighter jet, Sikorsky helicopters, Javelin missile systems and the Aegis naval combat system.

Military contractors like Lockheed benefit from a Defence supercycle driven by heightened geopolitical tensions and frictions between major economies, supporting both financial performance and stock prices. The United States is ramping up spending, with President Trump calling for an increase to $1.5 trillion for the next fiscal year. 17 The European Commission aims to mobilise nearly €800 billion over the coming years 18 and NATO has committed to raising defence investment to 5% of GDP by 2035. 19

US strikes against Iran reinforce these trends, supporting continued growth. When President Trump was asked about an additional $200 billion request to fund the war, he described it as "a small price to pay" 20. Lockheed's order backlog rose to $194 billion and revenues grew 5% in 2025, with management expecting to maintain solid momentum and return to EPS growth. 21

Still, challenges remain. Geopolitical tensions and tariff uncertainty contribute to macroeconomic pressure, while supply chain risks continue to affect costs and production. Lockheed's reliance on the F-35 programme for 26% of sales creates concentration risk 2 ,while losing the next-generation F-47 contract to Boeing is a notable setback. 23

Shares of Lockheed Martin reflect strong business performance and a supportive environment, remaining on track for new records. However, the stock is pulling back from its initial Middle East conflict boost, leaving it vulnerable to deeper corrections towards the EMA200, which would test the current upward momentum.

Chart source: www.tradingview.com

Tesla

Founded in 2003 and led by Elon Musk since 2008, Tesla has disrupted the automotive industry and remains a leading producer of battery electric vehicles (BEVs), while also expanding into energy generation. The company is increasingly focused on AI, particularly in autonomous driving and humanoid robotics.

Tesla had a rough 2025, recording its first annual revenue decline and a near halving of net profit. This was driven by weakness in its core automotive segment, with deliveries falling 9% y/y 24. The underperformance reflects a combination of macroeconomic pressures, unfavourable US energy policy shifts, an ageing product lineup and intensifying competition, particularly from China's BYD, which overtook Tesla as the top BEV seller. 25

These pressures may persist into the second quarter, although there is scope for improvement. Deliveries could remain weak, but more affordable versions of the Model 3 and Model Y may support a return to y/y growth. Meanwhile, the high-margin energy business can continue to support profitability and partially offset automotive weakness.

Furthemore, these challenges may be near-term distractions, with the second quarter potentially pivotal for the robotaxi ambitions. Progress is tangible and the company plans to expand to seven additional cities in the coming months, while production of the dedicated Cybercab is expected to begin in April. 26

That said, Tesla is still working towards fully unsupervised driving and the initiative depends heavily on regulatory approval. Moreover, Tesla has a lot of work to catch up to established players like Waymo. Meanwhile, any meaningful production of the Optimus humanoid robot is unlikely before year-end, while the consequential chip fab is more of a longer-term driver rather than an immediate catalys.

Shares of Tesla are not having a good year as markets react to the business headwinds, while the AI pivot may take time to generate material returns. The stock remains exposed to further downside, although recovery potential remains. The second quarter could prove critical and tangible progress on strategic initiatives (or the semblance of it) could improve sentiment.

Chart source: www.tradingview.com