Apple’s Revenues Dipped Again in Q4 FY23 in the Worst Streak in 22 Years

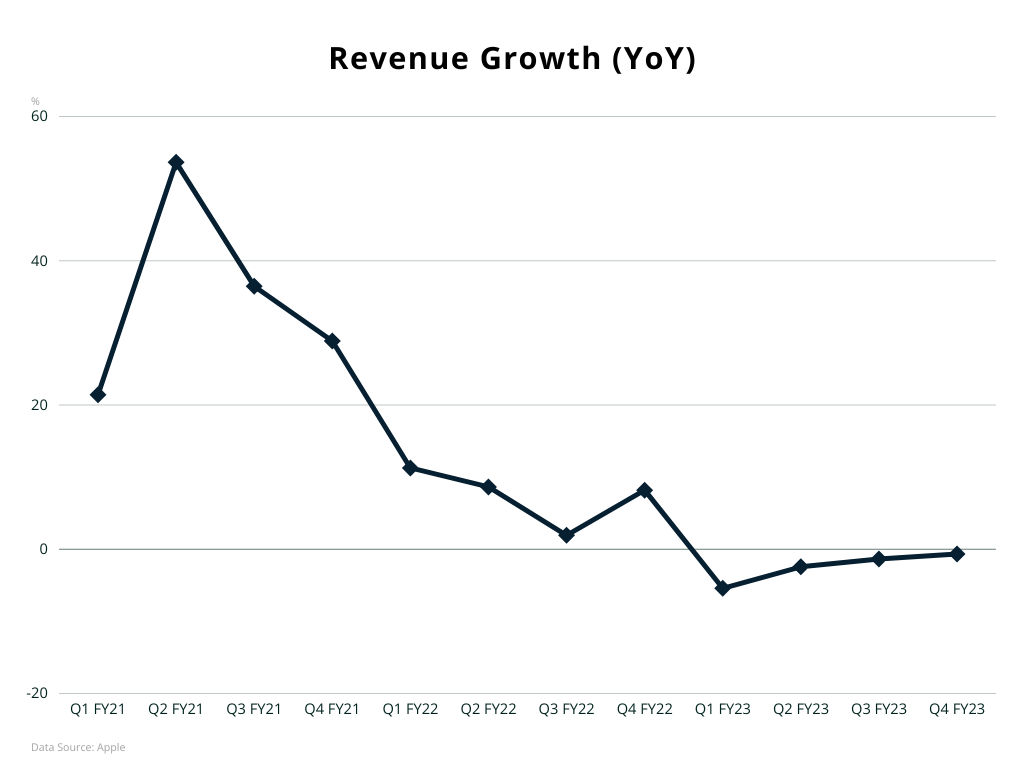

Declining Revenues

Apple released its latest earnings for Q4 FY2023 (period ended September 30) on Thursday, which showed strong bottom line performance. Net income rose nearly 11% y/y to $22.956 billion and gross margins of 45.2% was up 70 points on a sequential basis. [1]

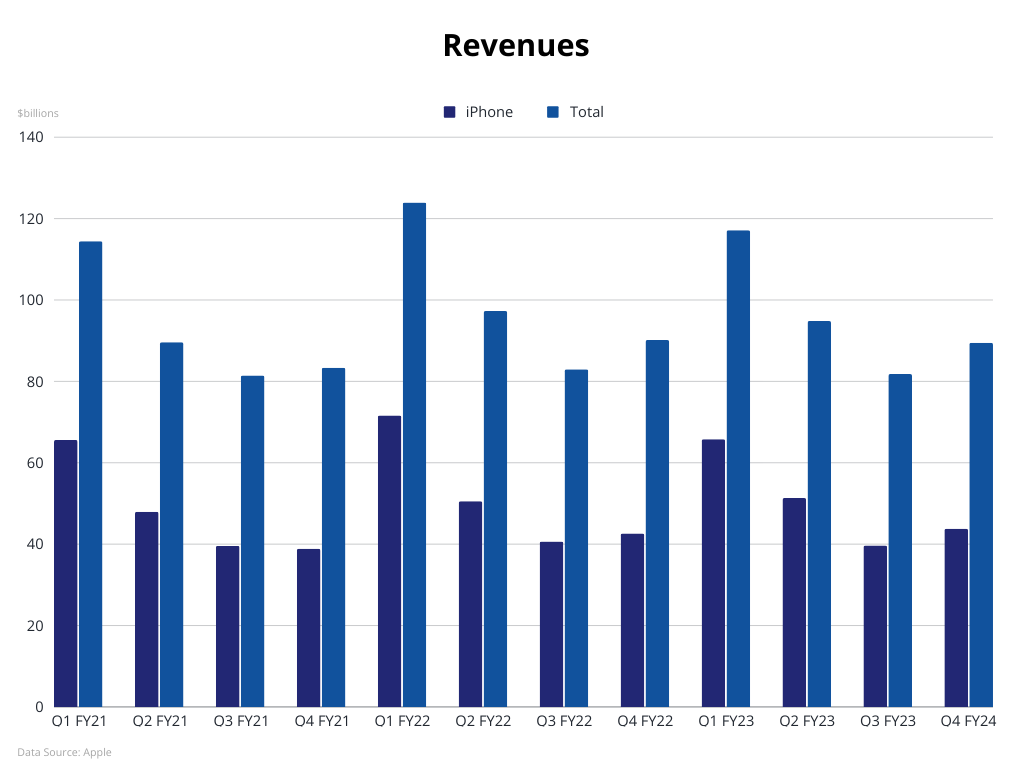

Its top line however, disappointed again, as revenues of $89.498 billion marked an almost 1% y/y drop. This figure extended the company's lack of growth into the fourth consecutive quarter, in what is the weakest streak in twenty-two years and the worst performance of the iPhone era.

The firm faces a challenging environment, as elevated inflation, high interest rates and economic uncertainty make consumers reticent. The global smartphone, tablet and PC markets have been mired in weak demand this year. Sales of Macs, iPads and Wearables all registered year-over-year contraction in Q4 FY23.

CFO Luca Maestri offered reserved guidance for the current December quarter (Q1 FY2024), during the earnings call. He expects "similar" revenues to last year (which had one more week), so it is unclear whether the tech giant will be able to return to revenue growth and overcome its dry spell [2]. In last year's December quarter, the firm had generated sales in excess 117 billion and the second highest figure ever. This is typically the strongest reporting period, as it includes the holiday season and the first full quarter of the newest iPhones.

Services Record

The star of yesterday's report was once more the Services segment, which continues to flourish. Sales increased 16.3% y/y to $22.314 billion, setting new all-time highs. The segment includes the App Store, advertising, cloud storage, music, streaming and more.

Apple's strength lies in its ecosystem these services become increasingly important for the company. They create stickiness and make users spend, helping the top and bottom lines, outside of the product cycle. They also reinforce the firm's moat, as switching to other ecosystems becomes harder, the more engaged a consumer is with those services.

Along with the latest iPhones in September, the firm announced two new iCloud+ tiers, with higher storage capacity and price tag. It also continues to make progress on streaming (TV+), with appealing and critically acclaimed content, including live sports. Underscoring the appeal of its services and its pricing power, Apple raised costs recently, with the One bundle (iCloud, TV+, Music, Arcade) now starting at $19.95/month in the US, from 16.95 previously. [3]

Encouraging iPhone Sales

The global smartphone market has taken a hit over the past several quarters due to various factors, including saturation, maturity, high inflation and economic slowdown. However, there are signs of bottoming out, with global shipments falling just 1% y/y in Q3 according to Canalys. [4]

Apple's main revenue generator are the iPhones and although their demand has been negatively affected from the global slowdown, they have generally shown resilience. This was reflected in Thursday's results, as iPhone sales rose more than 2.5% y/y, to $43.805 billion, marking a record for the September quarter. The results included some sales of the latest iPhone 15 lineup, released in late September, with mostly incremental updates rather than any radical upgrade.

China Concerns

Apple's dependence on China for production and sales has been a source of concern, given the fraught Sino-US relation and the chip export curbs. Highlighting the potential headwinds, The Wall Street Journal reported in September that China had banned the use of iPhones for government officials [5], although the foreign ministry denied any restriction on foreign devices [6].

Greater China is the third largest market and sales contracted 2.5% y/y, to $15.084 billion in the reported quarter, contrary to the growth in Europe and the Americas. CEO Tim Cook attributed that to the negative FX impact, saying that sales expanded on a constant currency basis.

Mr Cook's recent visit to the country underlines the market's importance and the worries around demand. This occurred not long after sales of the new iPhone 15 started, which underperformed those of its predecessor in the first days, according to Counterpoint. [7]

Apple however got some good news from India, where it has been shifting its focus and where it opened its first retail stores earlier this year. iPhone sales reached all-time record in India in the September quarter, according to CFO Luca Maestri.

Cagey on AI

Apple is entering the nascent Augmented Reality market, with the Vision Pro headset, which was unveiled in June and is scheduled for release in early 2024. Mr Cook spoke of "amazing response from developers who are currently creating truly incredible apps" in Thursday's earnings call. [2]

The AR headset showed the tech giant has not lost its ability to innovate and push on new frontiers, but there are fears that it may be missing out on the most important development, that of generative Artificial Intelligence (AI). Apple's latest iPhones and Macs sport the most advanced 3 nanometers chips, which can definitely handle heavier AI workloads, but the firm is tight-lipped around its generative AI plans. Mr Tim Cook remained cagey in yesterday's call, only saying that "we have work going on". [2]

The technology can unlock tremendous value for the company, especially given its vast proprietary data, but a late entry in the AI arms race can put it at a disadvantage. What we have seen so far, is that early adopters stand to benefit the most. Chip designer Nvidia who enabled this revolution has seen its revenues and profits soaring, as rival AMD is just now stepping up. Microsoft with its first-mover advantage, got a bump in its cloud sales thanks to AI demand, whereas Alphabet lags in monetizing due to its late start.

Rough Patch

Apple is going through a rough patch lately against a challenging environment. Thursday's results highlighted that, with the fourth straight quarter of y/y revenue decline and the stock drops in today's premarket. The high valuation creates concerns, given the lack of growth. There is also the lack of any concrete plans around its Artificial Intelligence planning, which can be critical for its future.

On the other hand, the report had significant encouraging signs. Profitability strengthened, iPhone sales rose despite suppressed demand globally and the increasingly important Services business hit new records.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 03 Nov 2023 https://www.apple.com/newsroom/pdfs/fy2023-q4/FY23_Q4_Consolidated_Financial_Statements.pdf | |

| Retrieved 03 Nov 2023 https://www.apple.com/investor/earnings-call/ | |

| Retrieved 03 Nov 2023 https://www.apple.com/apple-one/ | |

| Retrieved 03 Nov 2023 https://canalys.com/newsroom/worldwide-smartphone-market-Q3-2023 | |

| Retrieved 03 Nov 2023 https://www.wsj.com/world/china/china-bans-iphone-use-for-government-officials-at-work-635fe2f8 | |

| Retrieved 03 Nov 2023 https://www.fmprc.gov.cn/eng/xwfw_665399/s2510_665401/2511_665403/202309/t20230913_11142374.html | |

| Retrieved 15 Jul 2026 https://www.counterpointresearch.com/insights/early-look-iphone-numbers-show-waning-china-vs-vibrant-us/ |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.