Nvidia earnings preview: AI dominance and mounting risks

AI proliferation continues

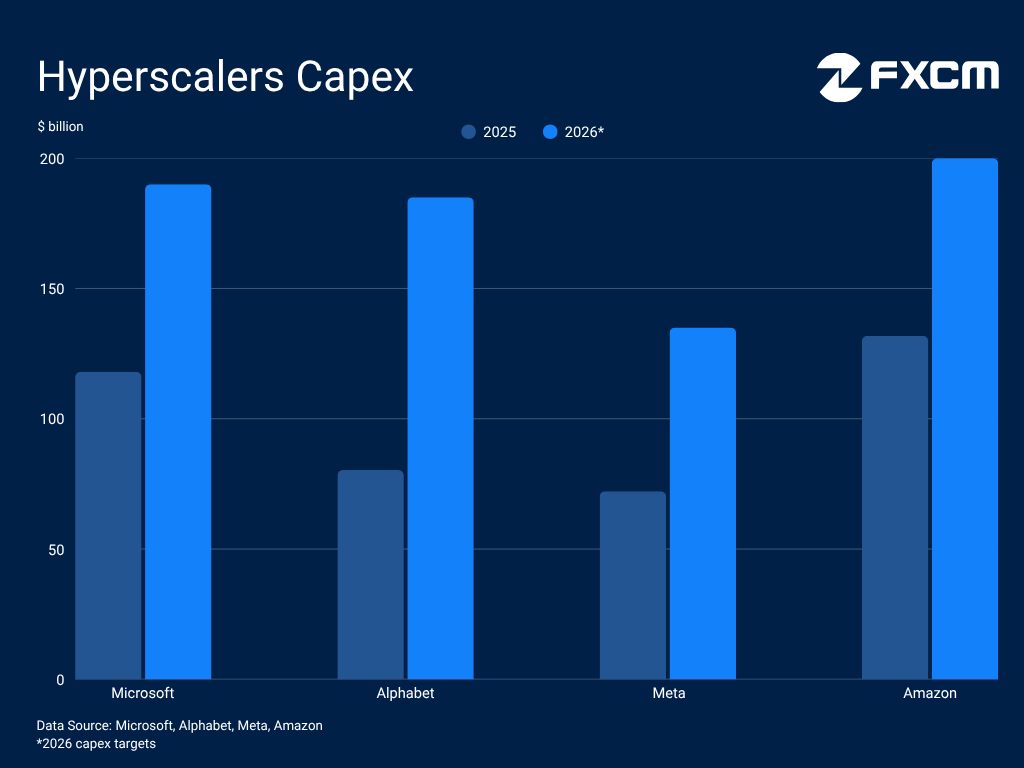

This earnings season confirms that the AI infrastructure race has entered a new, more aggressive phase, as key hyperscalers reaffirmed their spending commitments to fund the buildout. Microsoft aims for a 61% increase in capital expenditures, while Meta Platforms expects a similar growth rate after upgrading its guidance. Amazon.com reiterated its plan to boost investments by 50%, while Alphabet raised its forecast, now expecting spending to roughly double this year.

Crucially, these giants have largely silenced overspending critics by making the monetization case more convincing. Google's record 63.4% y/y Cloud revenue jump serves as a primary exhibit. This bullishness extends to the builders of the boom, like TSMC and ASML, which posted strong results and guidance.

TSMC CEO C.C. Wei spoke of "extremely robust" AI demand, with the company looking towards the higher end of its $52 billion - $56 billion capex target for the year. ASML, another gatekeeper of the global chips supply chain, expects double digit increases in both revenues and units shipped this year, with CEO Fouquet noting that demand for chips is outpacing supply. Meanwhile, the World Semiconductor Trade Statistics (WSTS) expects the semiconductor market to maintain a strong growth momentum this year and approach the $1 trillion threshold. [1]

Nvidia remains the AI leader

The battle for AI supremacy continues to fuel demand for NVIDIA's silicon, which remains the industry's gold standard. During the last earnings call, CEO Jensen Huang highlighted an exponential surge in compute demand [2], while CFO Colette Kress confirmed that hyperscalers remain the company's largest and most aggressive customer category [3]. This leadership is cemented through deepening partnerships. Amazon alone is set to deploy more than one million Nvidia GPUs this year [4], while Meta Platforms has committed to a multi-year scaling of its infrastructure using Nvidia's next-generation Blackwell and Rubin platforms. [5]

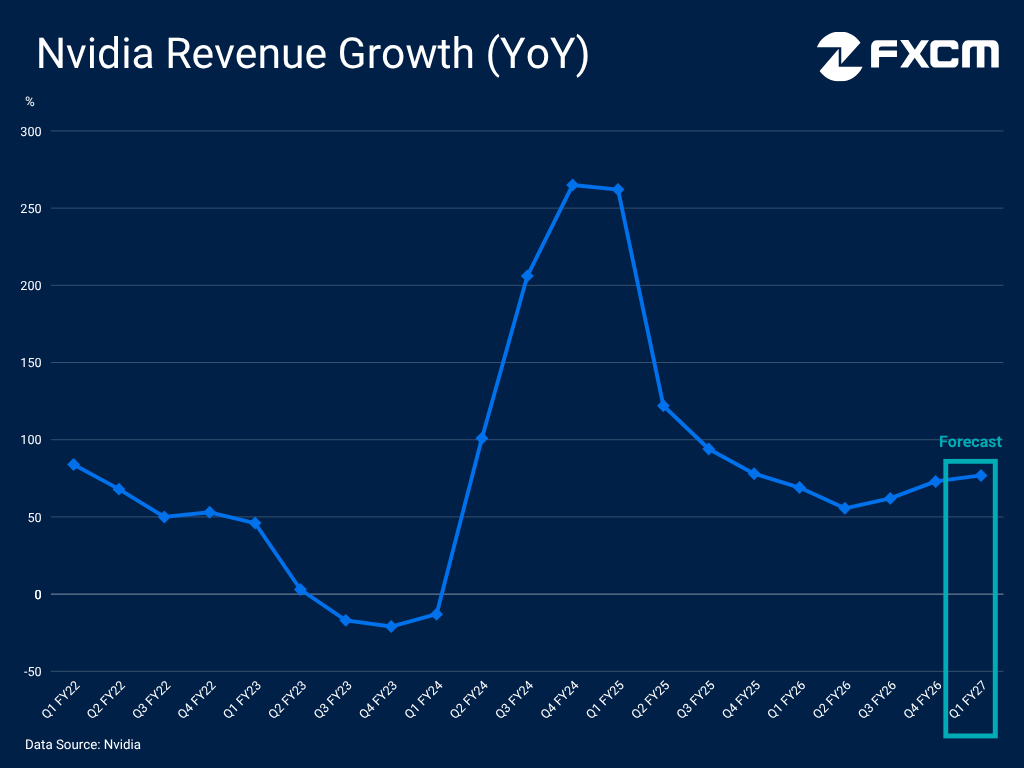

These dominant market dynamics are reflected in NVIDIA's stellar financials. The company reported record revenue of $68.127 billion in Q4 FY26 - a 73% y/y increase. Crucially, management expects this momentum to carry through the April quarter results, which are due on Wednesday May 20. Looking further ahead, the transition to the Vera Rubin architecture in the second half of 2026 is expected to provide the next major catalyst and maintain Nvidia's lead over both rival hardware and in-house silicon efforts.

Threat from CPUs and custom silicon

While NVIDIA remains the dominant force in training frontier models, the industry is experiencing a structural shift toward CPU-centric architectures. This is fuelled by a shift towards inference and Agentic AI, that rely on CPUs and benefit rivals like Intel and Advanced Micro Devices (AMD). Intel CFO David Zinsner said that training clusters historically ran a ratio of 7-8 GPUs per CPU, but that this moves to 3-4:1 for inference. With Agentic AI, it is hitting 1:1 and "potentially even flipping in the other direction a little bit". Deloitte sees inference as the "hot new thing" for 2026, expecting it to account for roughly two-thirds of all AI compute cycles [6], while Gartner project AI agents will be used in 40% of enterprise applications this year. [7]

Beyond the hardware shift, NVIDIA's moat is further challenged by a coordinated pivot among hyperscalers to develop custom in-house silicon, reducing reliance on Nvidia and optimising for proprietary workloads. Microsoft introduced its Maia 200 AI accelerator for inference in January, already live in its Iowa and Arizona data centres [8]. Alphabet unveiled its latest TPU v8, designed for the Agentic era, with CFO Anat Ashkenazi confirming it will also be sold to a "select group of customers" [9]. Amazon is accelerating its custom chips roadmap, with its CEO opening the door to third-party sales. [10]

However, these hyperscalers still rely heavily on Nvidia's chips and are deepening their partnerships in many cases rather than replacing them. Amazon CEO Andy Jassy stressed they continue to order "substantial quantities" from Nvidia, with whom they will partner "as long as I can foresee" [11]. Alphabet CEO Pichai noted that Nvidia's GPUs are "a core part of" the AI accelerator portfolio and that they will be among the first buyers of the incoming Vera Rubin architecture. [9]

Additionally, the surge in CPU-heavy workloads does not pose an imminent threat to NVIDIA's leadership. The company has proactively vertically integrated by launching its own high-performance CPUs and its CEO sees Agentic AI as the next inflection point. Escaping Nvidia's full-stack ecosystem remains a massive hurdle for enterprises due to the deep integration of the CUDA software layer. Ultimately, the relationship remains symbiotic rather than competitive. As AI agents scale, they create a hybrid demand that necessitates both high-logic CPUs and the massive parallel throughput of Nvidia GPUs.

China still a source of uncertainty

The geopolitical landscape remains a primary source of volatility for NVIDIA. The US government has shifted to a case-by-case review of export licensing and has allowed limited shipments of Nvidia's H200 chips to China. On the back of this pivot, CEO Jensen Huang said in March that the firm is ramping up manufacturing of this product [12], creating optimism for a resumption of China sales, enhanced by his inclusion in President Trump's visit to the country this week. A restart of China shipments could drive faster revenue growth, as management's guidance excludes such sales.

However, the licensing and trade landscape remains vague, as the H200 could be subject to a 25% US import tariff before being shipped, which Nvidia may not be able to pass on [13], weighing on margins. Moreover, the bipartisan AI Overwatch Act, if passed, would codify prohibitions on exports of the most advanced AI chips and give Congress veto powers. [14]

It is also unclear whether NVIDIA can find buyers in China as Beijing pushes for technological independence. President Xi stressed earlier this year that self-reliance in science and technology is critical for China's strength [15], while Reuters reported in January that Chinese customs were instructed not to permit H200 imports [16]. Meanwhile, Chinese tech giants are forging ahead with sovereign hardware tailored for local demand, including Baidu's Kunlunxin M100 for large-scale inference [17] and Alibaba's Zhenwu 810E for both training and inference. [18]

Structural fragilities

While the AI boom appears unstoppable, it is increasingly colliding with a fragile macroeconomic backdrop. Persistent stagflation risks, fuelled by energy shocks and the Middle East conflict, threaten the marketing budgets and corporate investments that serve as the lifeblood for hyperscalers like Meta Platforms and Alphabet. A contraction in advertising spend could quickly test investor patience for multi-billion dollar AI capex. Furthermore, deteriorating consumer sentiment and rising inflation pose a direct threat to the wider consumer electronics sector.

Meanwhile, the disruptions caused by the Middle East conflict pose real-world hurdles for energy-intensive chip manufacturing, adding to pressure from the memory crunch. Although this is unlikely to affect NVIDIA's shipments directly, cost pressures could weigh on margins while making the construction and operation of data centres more expensive.

The uncertain macroeconomic backdrop exacerbates concerns over Nvidia's sales and manufacturing concentration. The AI boom remains confined to a small group of hyperscalers and Nvidia's exposure is significant, with just two customers accounting for 36% of total revenue in FY25, up from three customers representing 34% the previous year. At the same time, its supply chain is concentrated in Asia among a small number of companies including TSMC and Samsung. [13]

Nvidia growth meets structural rotation

NVIDIA enters Wednesday's earnings on fundamentally solid footing, expecting to extends its growth momentum, as it remains the indispensable engine of an AI boom. A strong report, coupled with bullish guidance, would reaffirm the stock's upward trajectory, which has reached new all time highs this month.

Chart source: www.tradingview.com

However, the margin for error is narrow as challenges to NVIDIA's dominance mount. Technically, the RSI has not followed the stock higher, in a divergence that suggests momentum may be exhausting at these levels, creating scope for a pullback if results show any signs of softness.

Perhaps most telling is a rotation in market leadership. A strategic shift is underway, moving capital away from the companies funding the AI boom, toward those actually building it. This transition favours firms solving critical power and thermal bottlenecks such as Vertiv and Caterpillar, alongside vertically integrated memory leaders like Micron. Simultaneously, the shift toward inference-heavy workloads is driving renewed interest in CPU-centric plays like Intel and AMD, increasingly viewed as primary beneficiaries of the Agentic AI investment cycle. While NVIDIA remains the king of AI, the market is now rewarding a broader set of players.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.