Nike Posted its Slowest Sales Growth in 1+ Years in Q2 FY24 & Slashed the Full Year Guidance

Mixed Q2 FY24 Results

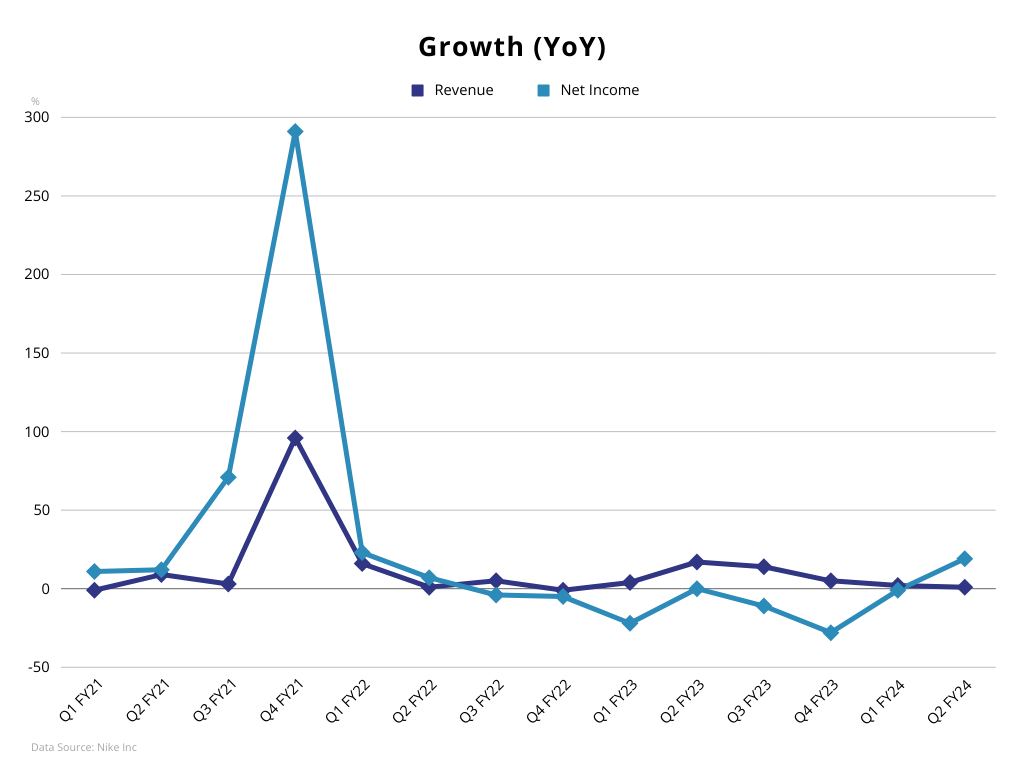

Nike Inc. (NKE.us) reported record total sales of 13.388 billion on Thursday for the three months ended November 30 (Q2 FY2024). However, the marginal 1% y/y increase (in constant currency) marked the slowest growth in more than a year and a big miss compared to the firm's own projection [1].

These results were weighed by North America, its biggest market, which dropped 4% y/y. However, Greater China grew by that amount in a period that contained multiple holidays and the Singles' Day (11.11) shopping festival. In fact, CEO John Donahue said during the earnings call, that Nike was the number one sports brand on Tmall, during Double Eleven.

Its bottom line was more encouraging, as Net Income of $1.578 billion was the highest since Q4 FY22 and the 19% y/y increase marked the first expansion in two years. Gross Margins widened to 44.6%, primarily due to "strategic price actions and lower ocean freight rates", despite unfavorable exchange rates.

The sports-apparel giant also made further progress on offloading excess merchandise, which has troubled most retailers, after the pandemic years stockpiling. Its inventories dwindled 14% y/y, to nearly $8 billion, a substantial climb down from the Q1 FY22 peak (of around $9.7 billion). This is achieved partly by promotional discounts, which curtail profitability, but demand creation expenses were up just 1% y/y, steadying at around $1.1 billion.

Cost Cuts & Trimmed Outlook

The Oregon-based firm announced on Thursday cost cuts of $2 billion over the next three years. The savings will come from "simplifying" its product mix, more automation, higher efficiency and streamlining of the organization. The latter will results in restructuring charges of $400 - $450 million that will largely materialize in the current third fiscal quarter.

During the previous earnings call, CFO Matthew Friend had highlighted a number of potential headwinds, emanating from the strong US Dollar, subdued holiday demand and H2 order book. On Thursday he said that the impact of these risks "is becoming clear' and slashed the full FY24 revenue guidance.

He now expects sales growth of just 1%, a substantial cut from the previous projected mid-single digits expansion. This is partly due external headwinds in Greater China. The post-pandemic recovery of the world's second largest economy has been uneven and grapples with deflation, as consumers keep their purses tight. The CFO also attributed the lower guidance to the strong dollar, promotional actions and "softness" in online traffic.

In recent years, Nike (NKE.us) has pursued a direct-to-consumer strategy via its online and physical stores and has complicated relations with its wholesales partners. It still relies heavily on them though and actually appears to be placing renewed emphasis on third-party vendors, with its products having returned to Macy's (M.us) this year. Most of the Nike brand revenues come from wholesales partners, amounting to $27.5 billion in the last fiscal year.

Market Reaction

The first nine months of the year were bad for NKE.us, posting a historical losing streak in August, amidst a challenging external environment with elevated price pressures, tight monetary policy and economic uncertainty. Things are improving though, as most major central banks have made significant progress on inflation and interests rates have likely peaked, while the Fed projects at least three rate cuts next year. This has helped NKE.us to rally in Q4 and break into profits for the year.

Thursday's quarterly report had encouraging aspects, but was a bit of a mixed bag. Markets reacted negatively to the outlook downgrade and the revenue miss, sending the stock more than 10% lower in today's premarket.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 30 Jun 2026 https://investors.nike.com/investors/news-events-and-reports/ |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.