Post-earnings outlook: can Meta turn capex concerns into an AI comeback?

The cloudless hyperscaler problem

Meta Platforms emerged as the primary casualty of last week's hyperscaler earnings, with its stock dropping over 8% on the first trading day after the report. All four hyperscalers reaffirmed their commitment to scaling spending this year to fund the data centre buildout powering AI proliferation, as the rise of Agentic AI boosting inference needs. The increased spending is partly attributed to higher component costs, primarily driven by a memory chip crunch that is benefiting Micron and other memory makers.

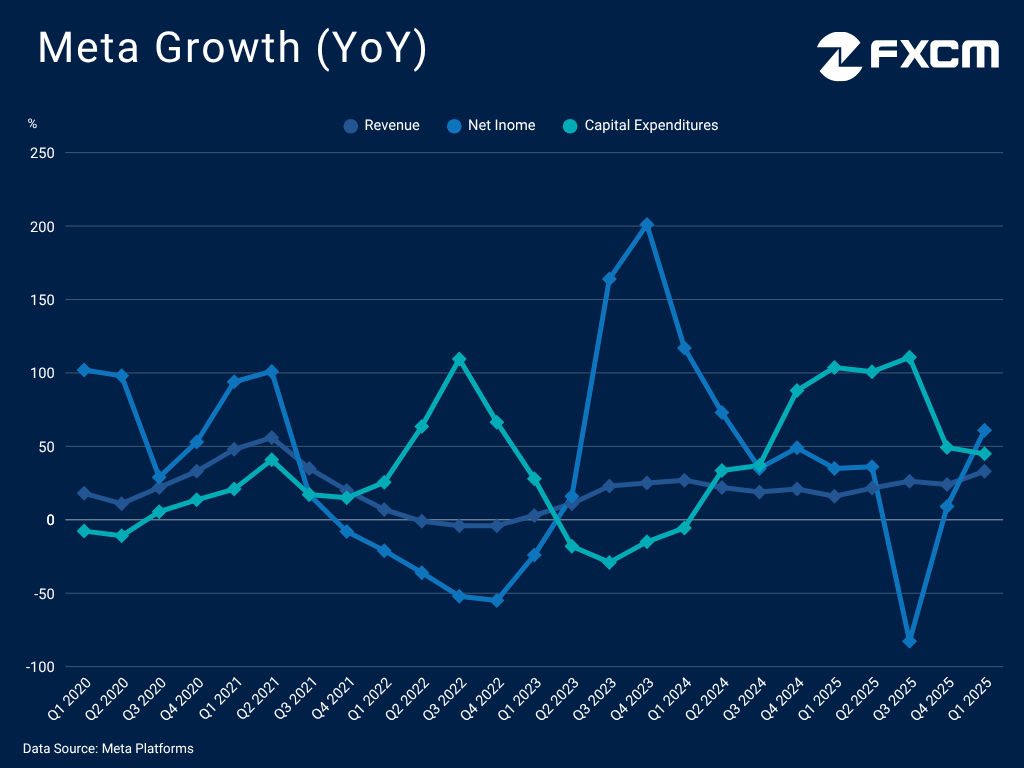

The social media giant raised its 2026 capital expenditure target to $125-145 billion to stay at the forefront of AI, representing an increase of at least 61.7% y/y [1], which sparked concern among investors. Unlike its Magnificent Seven peers Google, Amazon and Microsoft, Meta Platforms does not have a cloud business that can offer an immediate benefit from AI demand and investment monetisation. The divergence is evident in the reaction to Alphabet's report, which also boosted its capex target, yet investors reacted positively thanks to a record 63.4% y/y surge in cloud revenue, making the monetisation case increasingly convincing.

Not only is Meta a cloudless hyperscaler, depriving it of a key growth catalyst, but it also derives almost all of its revenue from advertising. This makes it particularly vulnerable to macroeconomic headwinds and the cyclical nature of the industry. The current environment is tough, with the Middle East conflict compounding tariff uncertainty in ways that could hurt consumption and weigh on marketing budgets, translating directly into slower growth. Moreover, internet disruptions in Iran and WhatsApp restrictions in Russia led to a rare sequential drop in average daily active people (DAP) during the first quarter, in a direct impact from geopolitical tensions.

Meanwhile, Meta's consumer-facing chatbots remain far less popular than those of OpenAI, Google and others, even if accurate measurements are hard to come by. At the same time, it faces an execution risk as the push to embed AI into the feed risks degrading the user experience and damaging high engagement levels across its apps.

AI investments fuel the advertising engine

However, the negative market reaction may have been somewhat exaggerated, as the results and guidance were very strong, supporting the monetisation case. Net income jumped 61% y/y while revenues rose 33% y/y, the fastest pace in nearly three years, with management expecting to maintain solid growth momentum in the current quarter of 22.1%-28.4% y/y. This robust expansion provides a strong fundamental buffer against the increased spending, particularly as capital expenditures actually moderated during the first quarter.

The dividends of Meta's AI spending are clearly visible in its advertising metrics. Ad impressions rose 19% y/y, the most in two years, while the average price per ad also accelerated with a 12% increase. These gains are directly linked to Meta's AI suite. Advances in its Ads Recommendation Model (GEM) powered a more than 6% increase in conversion rates for landing page view ads according to CFO Susan Li. Furthermore, the barrier to entry for AI-driven marketing is falling, with over 8 million advertisers now using at least one of Meta's generative AI creative tools. [2]

These initiatives are turbocharging Meta's advertising business, allowing it to navigate the macro uncertainty that has hampered smaller rivals. While Snap explicitly flagged a revenue hit from geopolitical friction [3], Meta did not report a similar impact. In a historic shift, eMarketer now projects that Meta will surpass Google in global digital ad revenue for the first time this year, a milestone driven by its superior AI-powered targeting and algorithmic discovery. [4]

To maintain its edge, Meta recently launched Muse Spark, the first model released under its new Superintelligence unit. This launch represents a significant strategic shift: unlike its previous open-source approach with Llama, Muse Spark prioritises internal monetisation and deeper integration within Meta's own ecosystem. Mark Zuckerberg noted that these models are already driving "double-digit percent" increases in Meta AI sessions/user [2]. To manage the cost of this scale, Meta is also optimising its hardware efficiency through custom silicon developed with Broadcom, alongside its continued use of AMD and Nvidia chips, a multi-vendor strategy designed to secure a long-term "strategic advantage" in compute costs.

Meta stock outlook

The negative reaction to the Q1 earnings report has shifted Meta's technical profile. The stock is now trading firmly below its EMA200, a breakdown that moves the immediate bias to the downside. This technical deterioration adds to a Death Cross (EMA50 < EMA200) and creates a clear path for a potential retest of the 2026 lows, particularly as markets continue to price in the structural risks of being a cloudless hyperscaler.

These investor concerns are rooted in tangible uncertainty. During the earnings call, Mark Zuckerberg admitted that Meta does not yet have a "very precise plan" for how each individual AI product will scale, a statement that fuelled the narrative of unfocused capital expenditure. However, the sell-off may also be an overreaction to the long-term potential.

Meta's AI advancements are already translating into superior engagement and measurable advertising outcomes. The resulting acceleration in revenues and profits provides a fundamental floor for the investment case. If Meta can demonstrate that its Muse Spark models and custom silicon can successfully navigate macroeconomic headwinds unlike more vulnerable peers, the current decline could prove to be a temporary valuation reset. While the technical bias remains bearish near term, Meta remains well positioned to bridge the gap between heavy infrastructure spending and AI-driven growth, eventually paving a path back toward new all-time highs.

Chart source: www.tradingview.com

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.