A Divided Bank of England Raised Rates by 0.5% to New 14-Year Highs

Smaller Hike

The Bank of England had started tightening a year ago, but had been limited to mostly small rate adjustments. This approach has been unable to control surging inflation and the bank accelerated the pace of tightening over the summer. This culminated to a 75 basis points hike in the previous meeting last month [1], which was the biggest since 1989.

Today the bank shifted gears again, but towards the opposite direction, since it delivered a smaller increase of 0.5%, bringing the Bank Rate to 3.5% and new fourteen-year highs. In typical BoE fashion, the decision was not unanimous, as three of the nine members voted against the majority.

One of the dissenters preferred a bigger 0.75% move, while two policy makers wanted to pause and not raise rates. They argued that the now previous 3% rate was "more than sufficient to bring inflation back to target". [2]

BoE in a Tough Spot

The divisions amongst policy makers are also reflected in the policy statement and the murky guidance, for a bank whose communication usually leaves much to be desired. It repeated that further increases in the bank rate "may be required", while at the same time stressing that it will respond "forcefully" if inflationary pressures persist.

However, this is to certain extend understandable, since the Bank of England is between a rock and a hard place and faces bigger challenges than most of its major counterparts.

CPI Inflation eased in November according to yesterday's data to 10.7% y/y, which allowed the bank to downshift, but remains close to the prior 11.1% four-decades high. Meanwhile, the labor market remains "tight" and wages are elevated.

On the other hand, the UK economy contracted by 0.3% in the third quarter according to recent preliminary data, while the BoE expects this to be just the beginning of a prolonged recession.

Central Banks at Crossroads

The tectonic plates of monetary policy have been shifting since most major central banks try to assess the cumulative effects of their aggressive tightening cycles, which are of lagging nature. The Reserve Bank of Australia has taken the foot of the pedal, with its third miniscule 0.25% hike last week, despite the fact that inflation continues to rise. [3]

The Bank of Canada has been moderating its pace since July's full percentage point increase and has become the first major central bank to hint at a pause [4], while yesterday the US Fed downshifted to a smaller 0.5% increase, after a series of outsized 75 bps hikes. However, it maintained its hawkish stance and raised its projections for the terminal rate. [5]

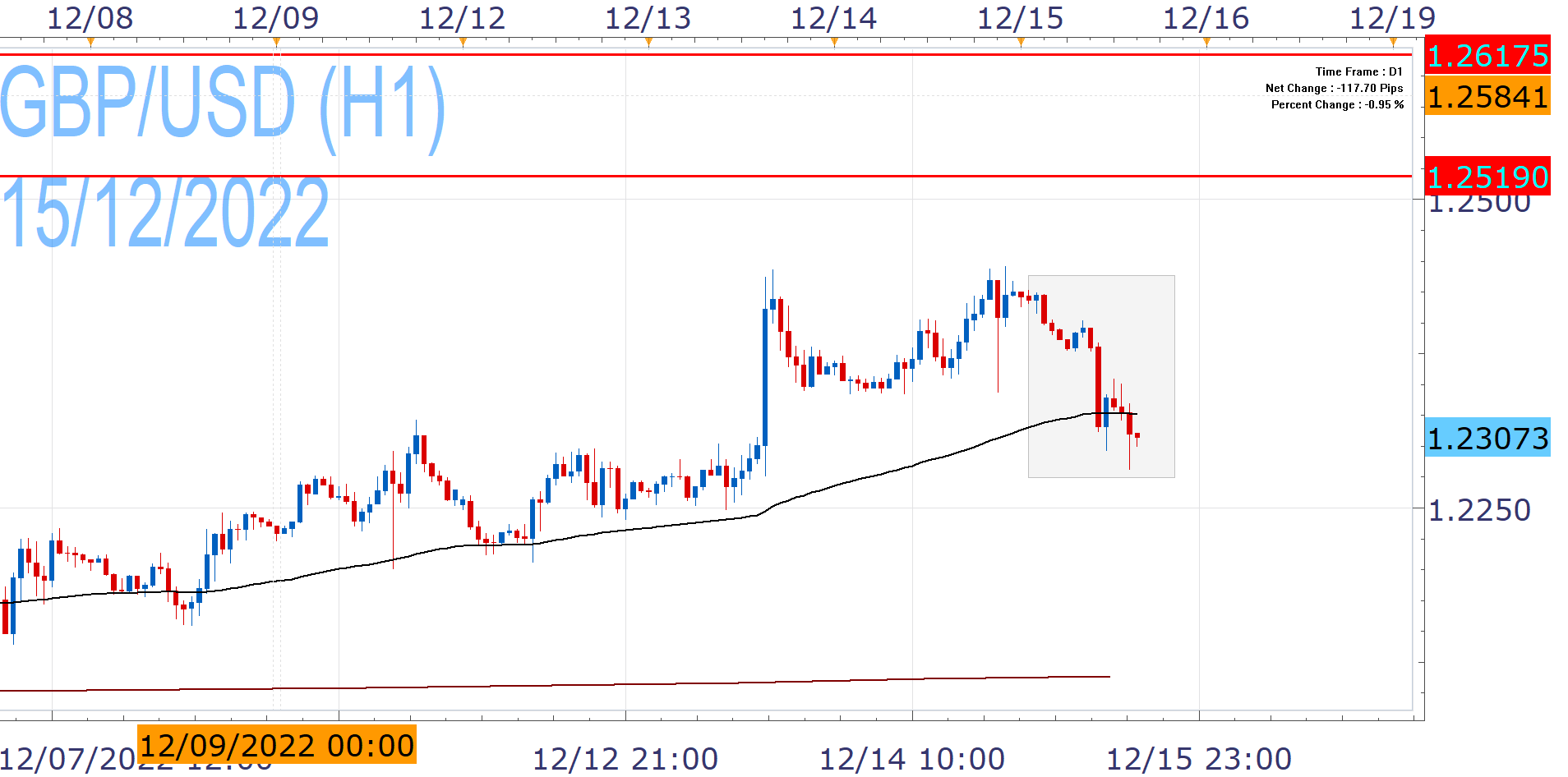

GBP/USD Reaction

The pair has managed to stage an impressive recovery from September's record lows, which it extended to six-month highs this week, after the soft US CPI report. The advance faltered today though, as the greenback benefits from the Fed's hawkish rhetoric.

GBP/USD has a limited reaction so far to the downshift from the Bank of England, staying under pressure.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 15 Dec 2022 https://www.bankofengland.co.uk/monetary-policy-report/2022/november-2022 | |

| Retrieved 15 Dec 2022 https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2022/december-2022 | |

| Retrieved 15 Dec 2022 https://www.rba.gov.au/media-releases/2022/mr-22-41.html | |

| Retrieved 15 Dec 2022 https://www.bankofcanada.ca/2022/12/fad-press-release-2022-12-07/ | |

| Retrieved 27 May 2026 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20221214.htm |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.