The Fed Delivered a Smaller Hike, but Projects a Higher Terminal Rate

Rate Downshift

The US Federal Reserve had pointed towards a slowdown in the pace of rate hikes, as officials try to assess the cumulative economic impact of the most aggressive tightening cycle in decades, given the lagging nature of monetary policy.

Chair Powell had recently rubberstamped such a downshift and on Wednesday, the bank unanimously delivered a well-telegraph increase of 50 basis points, coming down from a series of outsized 0.75% moves. [1]

Since the March lift-off, the Fed has produced 425 basis points worth of hikes, in order to bring down inflation. After yesterday's adjustment, the benchmark rate now stands at 4.25%-4.50% and the highest in fifteen years.

Other central banks have already taken their foot of the tightening pedal, such as the Reserve bank of Australia, which has been raising rates by smaller 25 basis points over the past three meetings [2]. The Bank of Canada has been decelarating since July's full-percentage hike and actually opened the door to a pause [3].

Softer Inflation & Strong Economy

This easing in the pace of rate increases is supported by recent data that have shown a deceleration in in inflationary pressures. The Fed's preferred measure of this, the Core Personal Consumption had eased to 5.0% y/y in October, while the most recent Consumer Price Index (CPI) figures from Tuesday, cemented the progress.

The Core CPI moderated for second month in a row in November, to +6.0% y/y and the lowest print since July. More to it, the headline CPI posted its lowest level of the year (+ 7.1% y/y) and continued its decline from June's forty-years high.

On the other hand, recent economic data and the last Employment Report show that more work is needed on the Fed's part. The US Economy added 263,000 jobs in November, unemployment stayed near fifty-year lows and wages grew significantly.

Furthermore, the economy expanded at an impressive pace of 2.9% in Q3, according to recent preliminary data, rebounding from two consecutive quarters of contraction.

Hawkish Message

Mr Powell welcomed the softer inflation figures during his press conference, but also noted that "less progress than expected" has been made. Moreover, he stressed that "substantially more evidence" will be required to provide confidence that inflation is on a sustained path lower, in an overall hawkish speech. [4]

The policy statement was practically unchanged, which in itself is hawkish, as the guidance for "ongoing increases" was maintained. The Fed-Chair hammered this message home, saying that "we're not in a sufficiently restrictive policy stance yet".

Once again, he downplayed the significance of the pace of hikes, as the ultimate level of rates is now more important and the time of period during which policy will need to remain restrictive.

Higher Terminal Rate

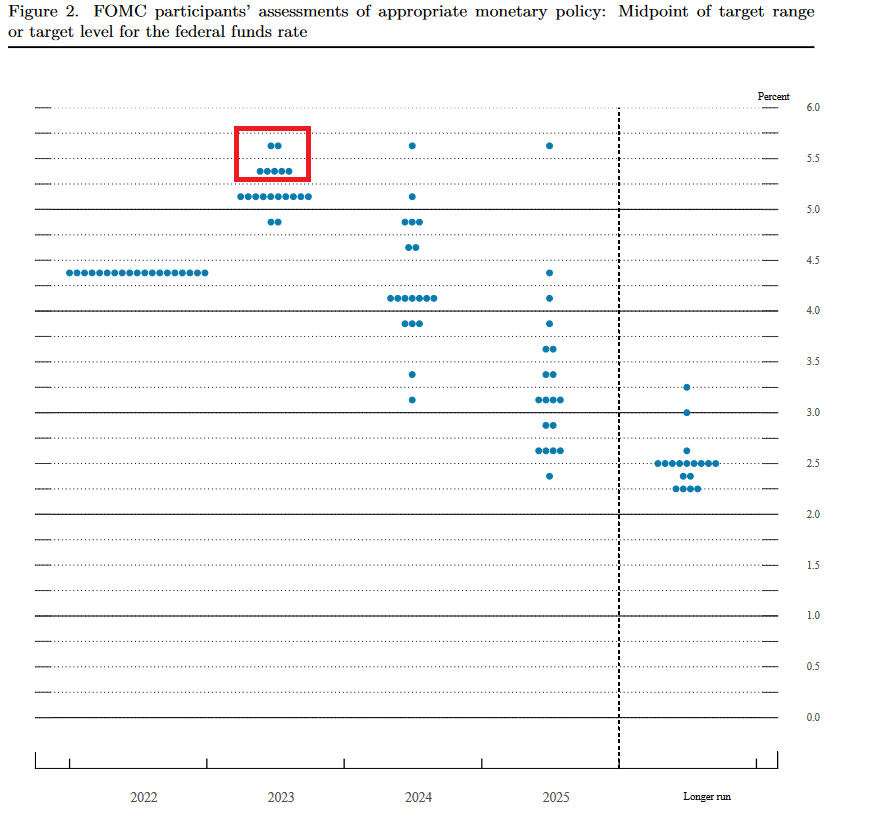

The need for more rate increases and restrictive policy "for some time", in order to restore price stability, was evident in the updated Summary of Economic Projection (SEP) and the "dot-plot".

Officials significantly upgraded their expectations for the appropriate policy path, now projecting the median rate to peak at 5.1% in 2023, from just 4.6% in the previous forecast, which implies another 75 basis points worth of rate increases. [5]

More to it, only two of the 19 participants see the terminal rate below 5%, while seven of them expect it to be above 5.25%.

Furthermore, the central bank forecasts Core PCE inflation to go as high as 3.5% next year (from 3.1% previously), without expectation for a return below the 2% target within the projected period.

Source: https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20221214.pdf

Markets Unconvinced

This week's soft CPI report created market optimism for a faster and lower peak in the Fed's interest rates, but the central bank did not get carried away and its rhetoric pointed to a "higher for longer" environment.

The USDOLLAR strengthened after the decision and SPX500 declined, but yesterday's drop seems rather limited and disproportionate to the Fed's rhetoric. This initial reaction shows that markets are probably unconvinced that the Fed will actually hike by as much as the update SEP suggests.

CME's FedWatch Tool still assigns the highest probability to a terminal of 5.00% - against the Fed's 5.1% median projection – and leaves room for rate cuts in the back-half of 2023 [6]. Mr Powell ruled out such a scenario though, saying that "historical experience cautions strongly against prematurely loosening policy".

The press conference was emphatically hawkish, but towards the end Mr Powell seemed to deviate from message, with the comment that"we are getting close to that level we think sufficiently restrictive". This reference caused Wall Street to jump and is likely partly responsible to the pared-back expectations around the policy path.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 15 Dec 2022 https://www.federalreserve.gov/monetarypolicy/files/monetary20221214a1.pdf | |

| Retrieved 15 Dec 2022 https://www.rba.gov.au/media-releases/2022/mr-22-41.html | |

| Retrieved 15 Dec 2022 https://www.bankofcanada.ca/2022/12/fad-press-release-2022-12-07/ | |

| Retrieved 15 Dec 2022 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20221214.htm | |

| Retrieved 15 Dec 2022 https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20221214.pdf | |

| Retrieved 27 May 2026 https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.