ECB, Fed & BoE Head to Pivotal Rate Decisions Amidst Great Uncertainty

Diverging Policies

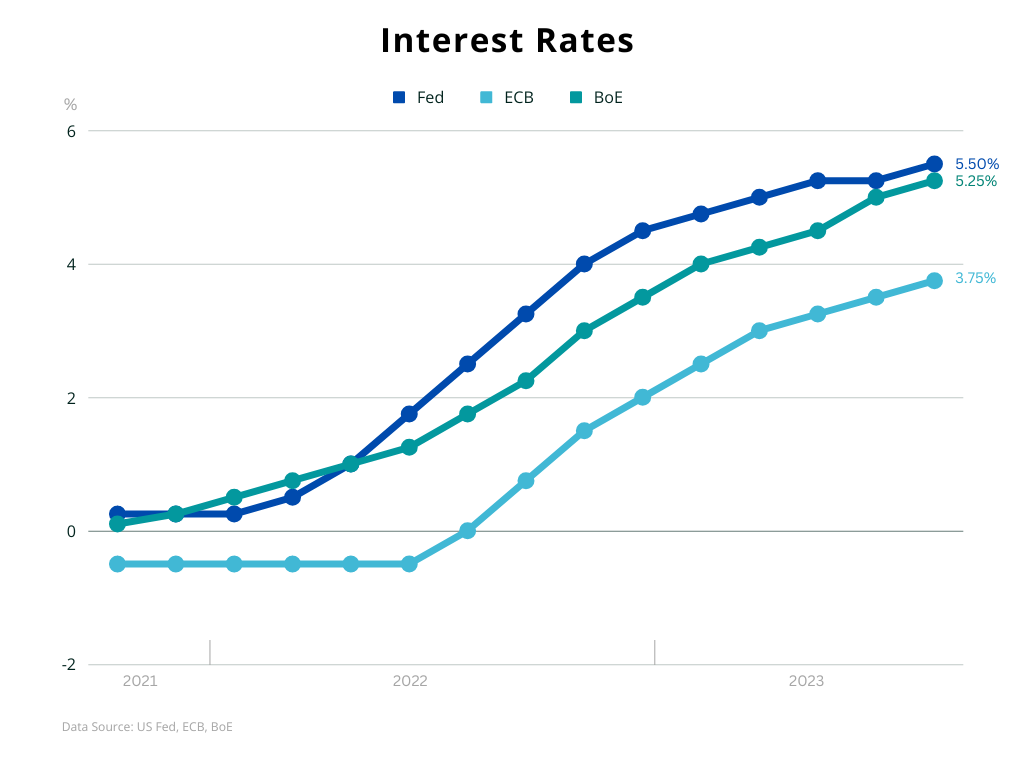

The Bank of England was one of the major central banks to begin tightening back in December 2021, followed by its US counterpart in March 2022, while the European Central bank did not produce a hike until July of that year. Despite the different starting dates, all three spent 2022 with a very aggressive stance and outsized hikes in order to bring down surging inflation. Although all are still committed to restoring price stability, their paths have been less in-tune during the current year, as they assess the cumulative impact of their actions and face different challenges.

The Bank of England has been hiking non-stop, but there was some back and forth, having reaccelerated its pace and has produced 525 basis points worth of hikes. The Fed has made greater progress and has slowed down this year - even paused in June before increasing rates again- having delivered 550 basis points of hikes so far. Its European peer maintained an aggressive stance, with more ground to cover and remains behind, having tightened by 425 basis points.

European Central Bank

Although policymakers have been very hawkish this year, they changed tack after their last hike in July. In contrast with her recent press conferences, president Lagarde adopted a non-committal stance and for the first time, she opened the door to a pause, saying "we might hike and we might hold" in upcoming meetings. [1]

The ECB is caught between a rock and a hard place, as it tries to balance between more tightening, economic slowdown and tighter credit conditions. Inflation is moderating, but more work is need, since at 5.3% y/y (both core and headline) in August it is far from the 2% target. On the other hand, the region's economic engine is sputtering, as Germany has not grown since the third quarter of 2022, creating trepidation.

US Fed

The US is far ahead than its peers, as inflation has already moderated substantially and given the lagging nature of the transmission mechanism, it may have already done enough. However, inflation is still high and its preferred gauge – the core PCE – ticked up to 4.2% y/y in July.

Furthermore, the US economy is strong, despite some recent softening and the labor market remains hot, even though there have been signs of cooling. These don't allow the Fed to declare victory yet and sustain the higher-for-longer prospects. Chair Powell has steered clear of offering forward guidance and has kept his options open, but his recent Jackson Hole speech had a hawkish tilt, where he warned that officials are "prepared to raise rates further if appropriate". [2]

Bank of England

The UK central bank may have started hiking much earlier that its two counterparts, but has not managed to contain the high cost of living, with inflation having surprised to the upside multiple times. Officials don't expect it to fall below the 2% for another couple of years, while historically high pay growth, is fueling a wage-price spiral. Inflation and wages keep pressure for more hikes.

On the other hand, economic growth is anemic and the outsized rate moves have increased borrowing costs, creating apprehension. Every extra hike increases chances that they may break something in their effort to contriol inflation. Testifying in the parliament this month, Governor Bailey noted that that the bank is "much nearer now to the top of the cycle", suggesting that the terminal rates is close [3]. However, similar remarks in the past have proven overly optimistic.

Uncertain Outlook

The three major central banks have adopted a non-committal and data-dependent approach, creating uncertainty around their next steps. They have all delivered massive amounts of tightening and have made progress on inflation, but they can't call it a day yet.

The ECB kicks things off for the Big-3 on next Thursday (September 14) and although baseline forecasts are for a pause, there is high uncertainty around the outcome. The Fed picks up the baton on September 20 and markets price in a pause, as things stand now. The Fed definitely has the room to stay on the sidelines and has traditionally sought to avoid surprises. The Bank of England follows on September 21 and it is not easy to stop with the current data, but it has surprised before.

Monetary policy has is now at an intricate phase and focus will be not only on the rate decisions themselves, but also on any signaling as to their intentions from there on. It is unlikely they will commit to a specific policy path, but any hints will be welcome. The Fed also publishes its updated dot-plot. The last one from June projected a median terminal rate of 5.6%, implying another rate hike. [4]

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 08 Sep 2023 https://www.ecb.europa.eu/press/pressconf/2023/html/ecb.is230727~e0a11feb2e.en.html | |

| Retrieved 08 Sep 2023 https://www.youtube.com/watch | |

| Retrieved 08 Sep 2023 https://parliamentlive.tv/event/index/a874d801-1604-4242-a466-ed33f21019c8 | |

| Retrieved 09 Aug 2026 https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20230614.pdf |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.