The Fed May Lack the Flexibility That Other Central Banks Enjoy

Central Banks Introduce Hawkishness

On 21 April, the Bank of Canada was the first industrial country's central bank to signal a reduction in stimulus and a normalisation of monetary policy. Since then, there has been a hint of hawkish sentiment from the Bank of England by chief economist Andy Haldane who views inflation as an increasing threat. We have also seen a positive statement from the Reserve Bank of New Zealand and Reserve Bank of Australia.

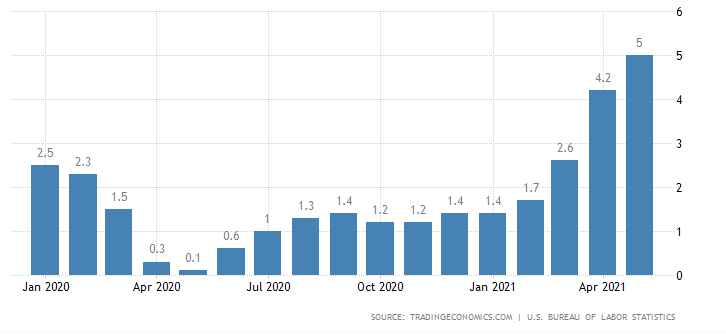

Market participants are now watching with a keen eye for any sign or signal from the US Federal Reserve (Fed) on the timing of its tapering and reduction in stimulus. Taking a look at the last 3 CPI prints out of the US, one sees significant spikes in inflation:

Inflation May Actually Be Elusive

Surely with these types of releases it would make sense for the Fed to begin its tapering programme? However, prudence in this regard may be apt. We certainly acknowledge the Fed mandate of stable prices. The CPI here suggests that the Fed is making progress in this regard (the Fed will take its policy cues from PCE as opposed from CPI, but they tend to trend similarly). However, we make the point that the last three prints are probably suffering from a low base effect and that the Fed needs more data.

Labour Languishes

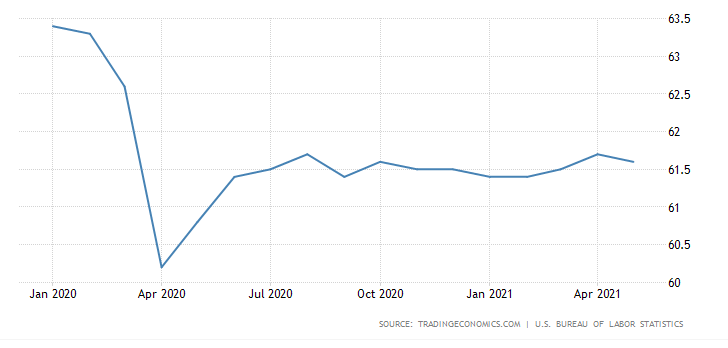

Moreover, the Fed has a second mandate to achieve maximum employment and in this regard it is lagging. Whilst the central banks mentioned above have signalled a reduction in stimulus (or dissented in Haldane's case), it must be mentioned that their respective labour markets seem to have recovered to pre-pandemic levels. This is not the case for the USA which still has a languishing participation rate:

Given the maximum employment mandate this must be a concern for the Federal Reserve and, as such, it may not have the flexibility to reduce its stimulus as the other central banks have signalled in their statements. The next FOMC statement will be released on Wed, 16 June at 6:00pm GMT. At 6:30pm GMT, Fed Chair Powell will hold his press conference. Market participants will be listening for clues regarding the timing of tapering and for further communication regarding the Fed's thoughts regarding inflation and the health of the US labour market.

Conclusion

We acknowledge that the downtrend that characterised the USD during 2020 has abated for now. However, FXCM's USDOLLAR index is now consolidating sideways, without a directional bias. This suggests that market participants still need further information regarding the Fed's monetary policy stance. If indeed they turn hawkish, it is likely to support the greenback, with accumulation to ensue.

However, this is not the case. Given the uncertainty around whether inflation is transitory or not and the lagging participation rate, the last five weeks, in particular, are characterised by neutral and uncertain price points in the USDOLLAR index. This may all change once we hear the press conference but, for now, it seems that the market is not convinced that the Federal Reserve has the same manoeuvrability that allowed the other central banks to issue statements that had the introduces hawkishness in them.

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.