Previous Stagflationary Periods Suggest a Hard Landing Will be Tough to Avoid

April's consumer price index (CPI) shows some respite at 8.3% y/y, compared with the previous month's 8.5% y/y. There is a hint of moderation as this was the first month of decline after seven months of higher annualised inflation. Nevertheless, it was higher than the consensus at 8.1%. Moreover, stripping the volatile items out of the basket, the core reading was higher than forecast - 6.2% vs 6% y/y.

It is also worth noting that the producer price index (PPI) for April y/y came in at 11%, which is down from last month's 11.5% y/y but was still higher than the market forecast of 10.7%.

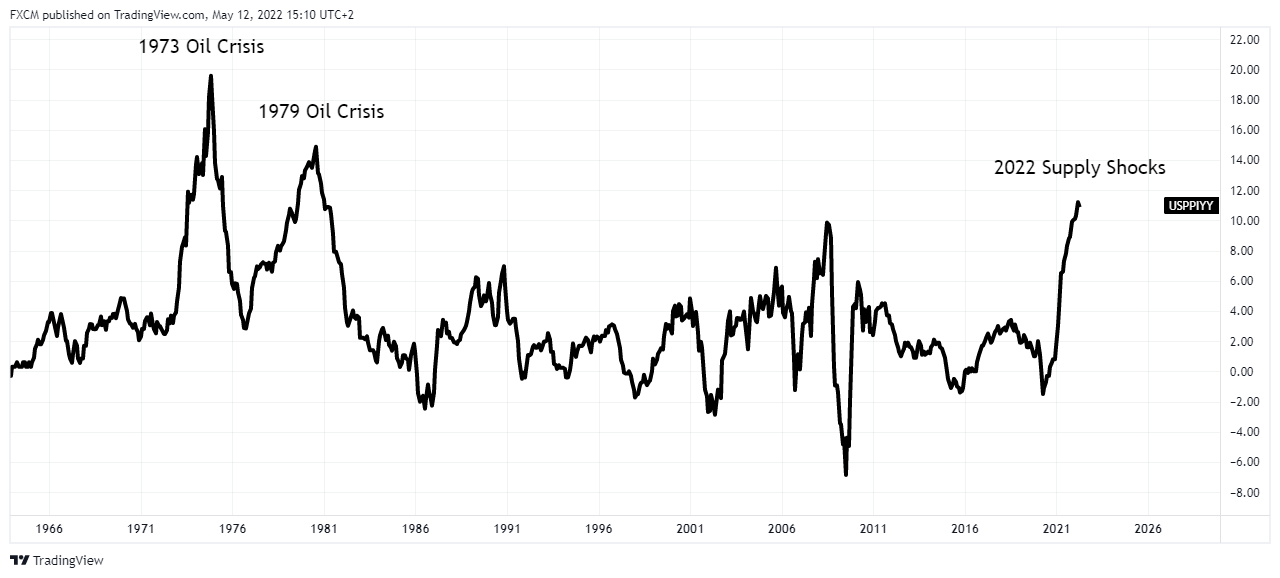

Even though both the CPI and PPI have shown slight signs of moderation, inflation is still running near 40 years highs. The Fed tends to focus on the core CPI reading, as monetary policy cannot do much to control the supply side. However, we posit that it is vital to consider the inflation picture from the PPI for this current inflationary cycle analysis. This PPI to CPI methodology is because 2022 macroeconomics has supply-side shocks, which, although rare, are an essential part of the current inflation environment. Consider the following chart showing the PPI series from May 1964:

We suggest that the 2022 supply shocks are similar to the 1973 oil crisis and the 1979 oil crisis when the Yom Kippur War and the Iranian Revolutions triggered supply shocks to Middle Eastern oil exports. Similarly, the Russian invasion of Ukraine has introduced tighter supply into a market that already had excess demand. Let's add core CPI to the series:

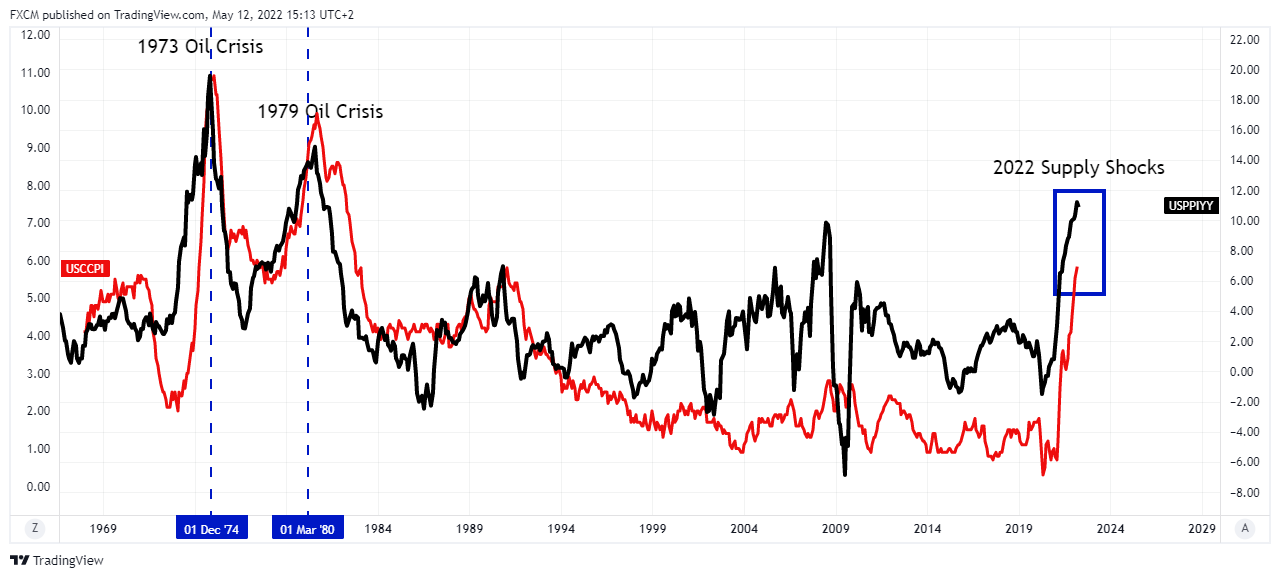

During the two oil crises, the PPI (black line) led the core CPI (red line) up. But, importantly, it wasn't until PPI moderated and dropped below the red series (blue dashed verticals) that the core CPI also slowed. We refer to this as the moderation catalyst and note that it is still to occur in our current inflationary environment (blue rectangle). To assist in the analysis, let's add the federal funds rate to the chart:

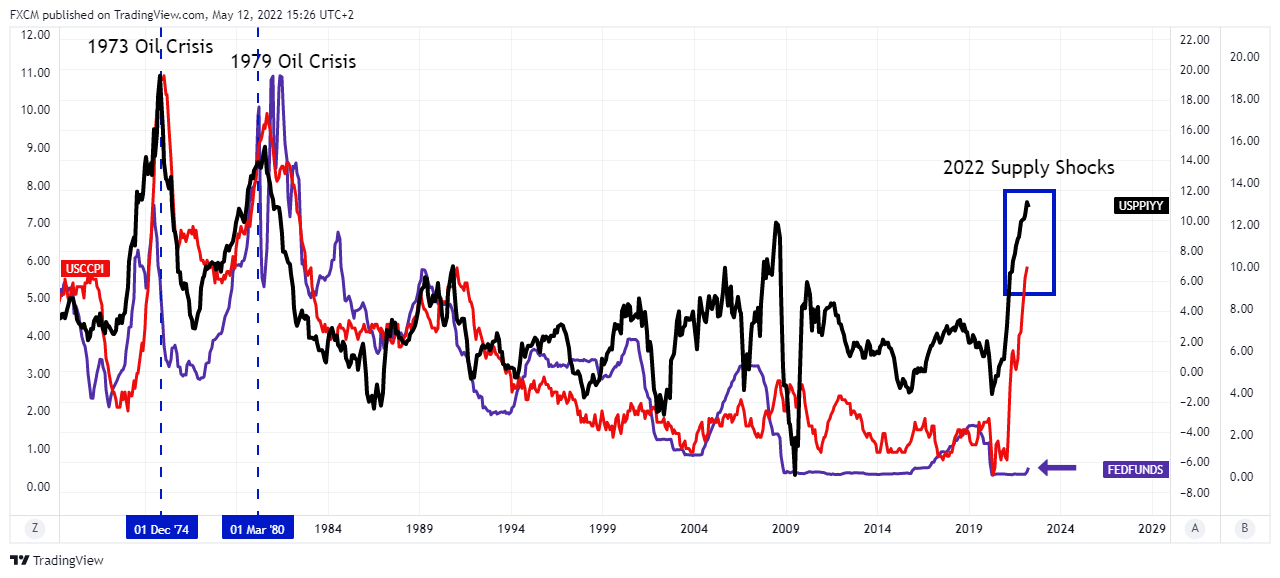

The purple line chart is the federal funds rate. Consider its movement before the blue dashed vertical, representing the moderation catalysts. In similar periods, the federal funds rate moved noticeably higher and hugged the red core CPI series. That is not the case now. The purple series severely lags behind the inflation series (purple arrow). This occurrence would suggest two likelihoods. Firstly, the Federal Reserve is far behind where it should be in this current cycle. Secondly, the Fed will have no choice but to be aggressive in its rate hiking cycle. If this is true, taking 75bps off the table for the next two meetings seems to be an error. Nevertheless, let's continue the analysis by including the U3 unemployment rate into our model:

The model is now getting fairly messy with all the included series. I have made U3 orange, with a bluish area, to make it more distinguishable. The key to this part of the analysis is that the unemployment rate tended to kick up before moderation catalysts (orange arrows). This contraction was when the federal funds rate (purple line) was heading higher.

Given that we haven't had this type of kick up in the fed funds rate, it makes sense that unemployment hasn't kicked up either. However, it does introduce the critical issue of whether the Fed can avoid a hard landing. The prior periods chosen for comparison would suggest that this will be very difficult to achieve if the Intermarket relationships still hold.

There is little doubt that the Fed needs to compel a moderation catalyst (blue dashed verticals). Unfortunately, they're behind and will have to play catch up by being aggressive with their rate hikes. However, it will be challenging for them to engineer a soft landing given previous U3 series behaviour in the model.

This is the problem that policymakers currently face. Battle inflation or protect the unemployment rate. Usually, a policy is implemented without this catch 22. This difficulty is the exact problem of stagflation, which is an economic paradox. Unfortunately, policymakers are caught between a rock and a hard place and have tough choices.

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.