New US Inflation Surge Puts Pressure on the Fed for Another Big Rate Hike

Shocking Inflation

Wednesday's latest inflation report, in the form of the Consumer Price Index (CPI) was a shocker, since it blew past estimates. Headline CPI jumped 9.1% year-over-year in June, from 8.6% prior, marking the highest level since November 1981. [1]

Food and energy prices continued their ascent, since the energy index increased to the highest level since 1980 and the food index to the highest since 1981.

The Core reading - which excludes the aforementioned components - rose 5.9% year-over-year, from 6% in May, continuing its de-escalation.

US President Biden called the headline reading "unacceptably high", noting though that it "is out-of-date", since energy accounted for nearly half of the increase. He elaborated that the figures don't take into account recent decreases in gas prices.

Markets have been trying to find a peak in inflation, but yesterday's June data crushed such hopes, coming hot on the heels of last month's unexpectedly high CPI report.

100 bps Hike Now in Play

The previous CPI report last month, just days before the Fed's June policy meeting, had forced officials to an aggressive 75 basis points hike. This was the largest move in nearly thirty years and came contrary to Mr Powell's previous guidance against rate moves of this size.

At the June press conference, Mr Powell had called the 0.75% hike "unusually large" and had pointed to "either a 50 or 75 basis point increase" for the upcoming meeting [3]. Later released accounts of that meeting and speeches of policy makers, have largely backed this guidance.

Yesterday's inflation figures however, may prove a game changer, since markets have now upgraded their expectation for an even bigger move. CME's FedWatch Tool projects a full percentage point increase this month, with 75% probability, at the time of writing. [4]

These aggressive market bets put pressure on the US central bank and give officials something to consider, but it does not mean that they will give in to them.

Fed Speak

We have seen some comments from Fed officials after the CPI release, but the activity looks to us a bit limited so far, although more speakers are due today.

Cleveland Fed President Loretta Mester (voter) was rather reserved in yesterday's interview on Bloomberg around the prospect of a 1% rate hike. When pressed, she noted that there is "no reason" for a smaller rise that the one delivered in the previous meeting (ie 0.75%).

A 100 basis points move is definitely a tall order for the Fed, since it will be the largest since at least 1990 and would constitute another break from the communicated tightening path.

If officials want to prepare markets for such an outcome, they only have a couple of days to do so, as the communication blackout period kicks in this weekend, ahead of the July 26-27 policy meeting.

Their decision is nearly two weeks out and they will have the chance to examine more data by then, such as Friday's Retail Sales and Michigan Consumer Confidence.

Market Reaction

The US Dollar jumped on the CPI release yesterday, but immediately paired back gains and ended the day with marginal profits.

The Fed's aggressive and front-loaded rate hike cycle, in reaction to surging inflation, has been a massive source of strength for the US Dollar. The policy differential compared to other major central banks is also stark, especially against the European Central Bank which has signaled to rate lift-off for next week, by a meager 0.25%.

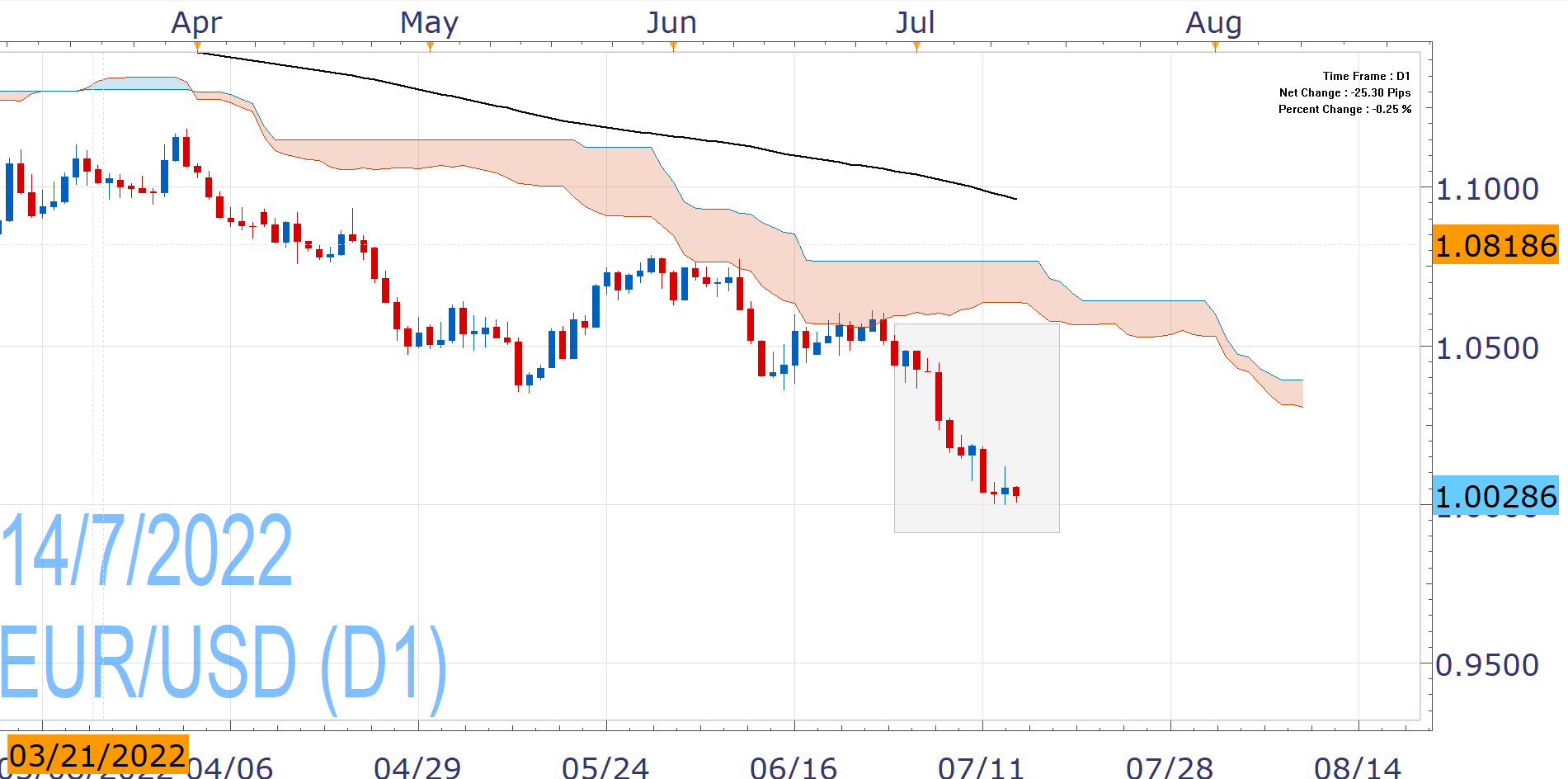

Along with recession fears, emanating mostly from gas supply disruptions in the continent and especially Germany, EUR/USD has plunged this month, hovering around parity for the first time in two decades.

The US bond market has also taken a beating and the 2-Year Note (2USNote) dropped yesterday, while the two-year and ten-year yield inverted again recently, which is often seen as a sign of impending recession.

The high inflation-high interest rates environment and fears of a recession have been detrimental for the US Stock market, with SPX500 closing the second quarter with in bear territory. However, the Fed's hawkishness may be approaching a peak and if it does not deliver a 100 bps hike, Wall Street could find reprieve.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 14 Jul 2022 https://www.bls.gov/news.release/cpi.nr0.htm | |

| Retrieved 14 Jul 2022 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20220615.htm | |

| Retrieved 30 Jun 2026 https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html# |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.