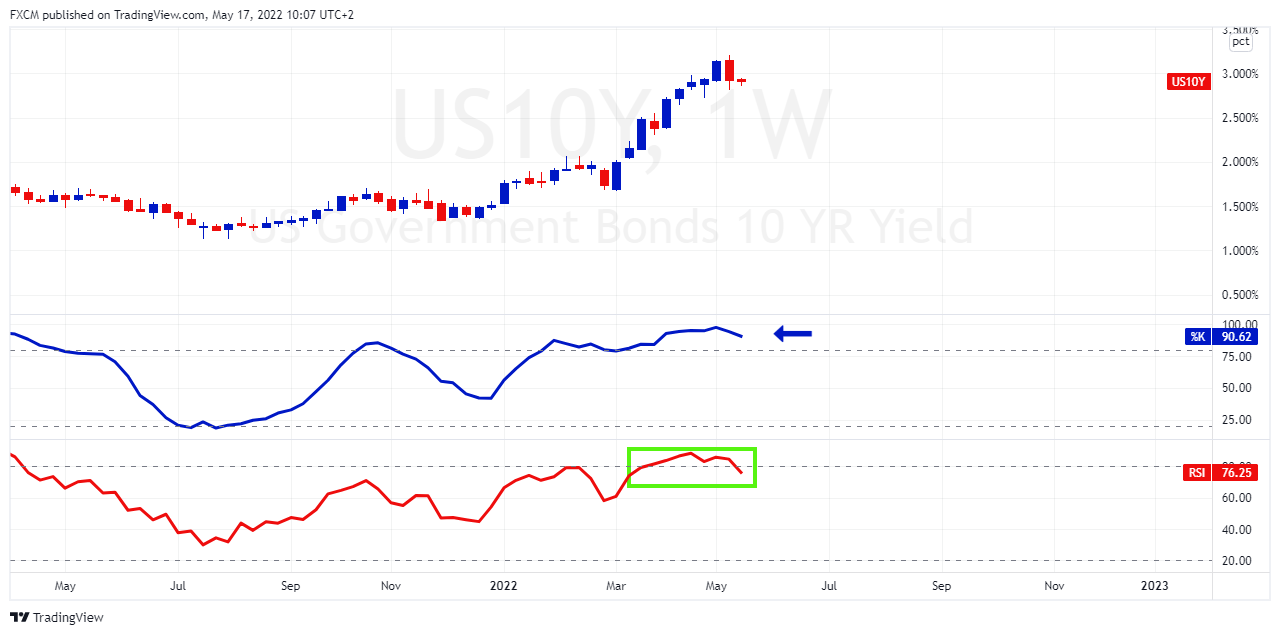

US 10-year treasury pauses as overbought condition normalises

The US 10-year treasury has halted its rapid ascent. Since the end of February, and over the course of 10 weeks, the yield jumped from around 1.73% to a high of 3.2%. The speed of the rise suggested that the treasury's yield had become overbought, which was confirmed by the RSI (green rectangle). Since then, the yield has pulled back to 2.92%, as the overbought condition looks to normalise (green rectangle again). This has alleviated some of the pressure that risk markets have faced over the course of the yield ascension.

However, the stochastic remains over 80 (blue arrow), which advocates that the underlying momentum is still strong. Market thinking is that the Fed's reduction of its bloated balance sheet will be supportive of policy tightening and yields reflect such. As long, as the stochastic remains in its upper quintile, we remain tentative about yield moderation. Prices don't move in a straight line and this is true for the price of money as well. In other words, this pause may be the proverbial "dip in an uptrend" scenario.

To this end we refer to a previous article, which suggests that the Fed is still too far from where it needs to be in this inflation cycle. The key here is moderation in the inflation numbers which should translate into the US 10-year treasury's stochastic moderating. That hasn't happened yet, which leads us to remain cautious.

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.