EUR/GBP Consolidates its Losses Ahead of the ECB & BoE Policy Decisions

European Central Bank

The European Central Bank paused its tightening cycle in October, after ten consecutives hikes, worth 450 basis points. This was allowed by the moderation in inflation, which has since decelerated sharply. Headline CPI grew 2.4% y/y in November according to last week's preliminary data, marking the slowest pace in more than two years. Officials are also concerned with the poor state of the European economy, which contracted by 0.1% q/q in the third quarter.

Influential and hawkish ECB member Ms Schnabel hinted at peak rates, speaking on Reuters on Tuesday. She took note of the "remarkable" progress on inflation, which has made further increase in interest rates "unlikely". [1]

Bank of England

The Bank England started hiking rates much earlier than its European counterpart and has delivered a larger amount of tightening, to the tune of 515 bps. It has stayed on the sidelines in the last two meetings, as inflation has eased substantially from last year's multi-decades peak and the economy suffers. The consumer price index was 4.6% y/y in October, but remains elevated. Furthermore, wage growth remains at historically high levels despite recent moderation and the government's upcoming 9.8% increase in the minimum wage creates upside risks.

Policymakers are in a tough spot, since price pressures are abating, but they don't expect inflation to fall below the 2% target for another two years. As such, they cannot rule out further tightening, although more actions could derail the already frail economy. Speaking on the Daily Focus last week, Governor Bailey said that officials will do "what it takes" to achieve that goal. He also shut down any rate cut prospects, noting that "we are not in a place now where we can discuss" such moves. [2]

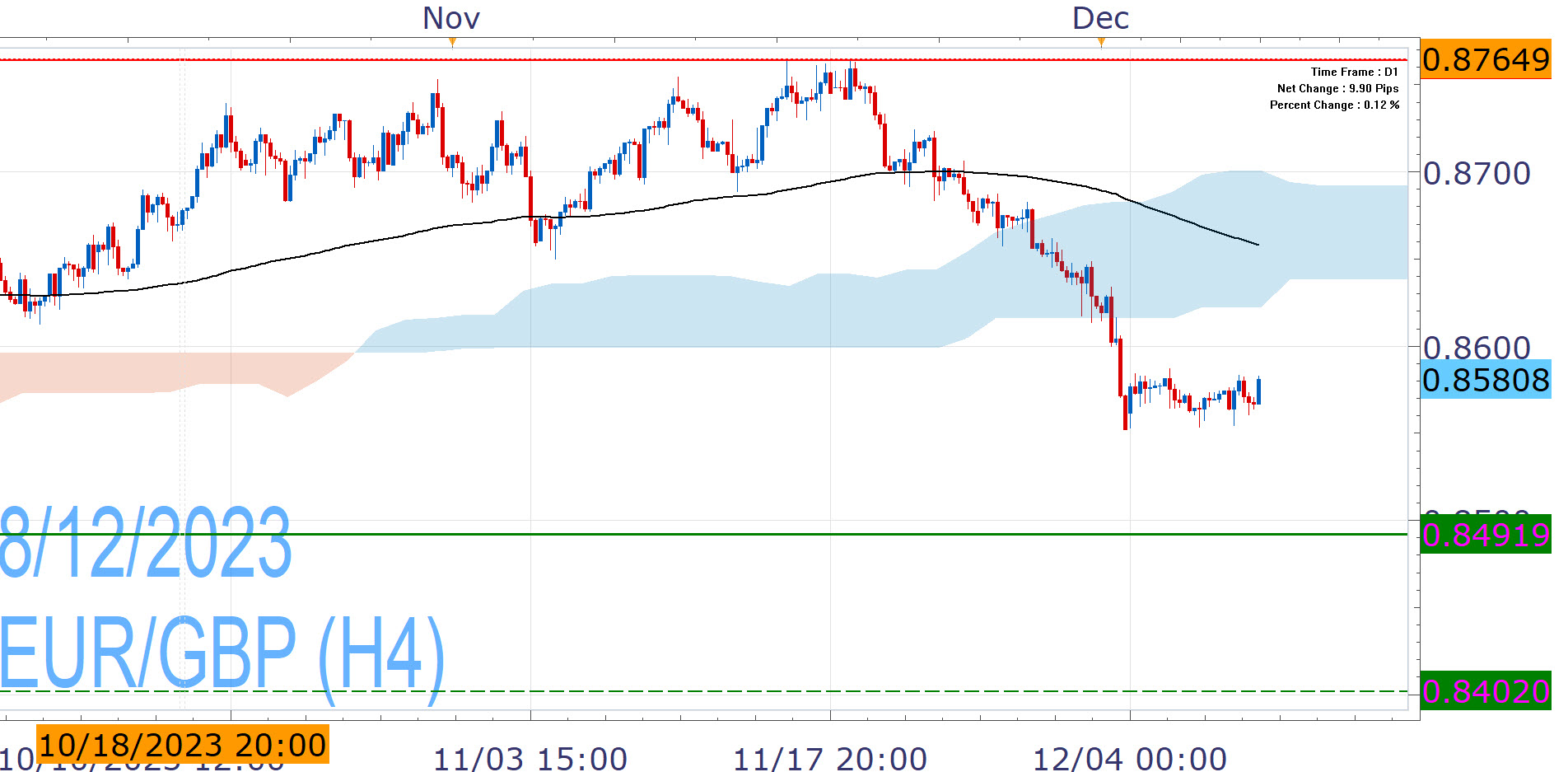

EUR/GBP Analysis

Last week's inflation print from Eurozone strengthens the case for peak rates and although calls for rate cuts within the first quarter of 2024 may be overly optimistic, the ECB is better positioned for such action than its UK peer. The Bank of England may have well reached the terminal rate, but it has more work to do on inflation.

As such, EUR/GBP has slumped over the past two weeks and is now exposed to the 2023 lows (0.8491). On the other hand, it consolidates its losses this week and we could see a rebound. However, the upside is hostile and a strong catalyst would be required for retaking the EMA200 (0.8658) and pause the bearish bias. Markets appear cautious ahead of next Thursday's decisions by both central banks, which will shape the trajectory of the pair.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.