Nike Stock Reaffirms Bearish Bias after Poor Results but Further Rebound May Be in Store

NKE.us Analysis

Nike is going through a protracted rough patch as it fell behind on innovation in recent years, relying too much on innovation, while its focus on direct sales did not work. These factors also assisted the rise of established rivals like Adidas (ADS.de), as well as startups like Swiss ON (ONON.us) and Deckers (DECK.us)-owned Hoka. Macros were not helpful either, with elevated inflation, high interest rates and economic uncertainty posing headwinds to consumption of discretionary goods.

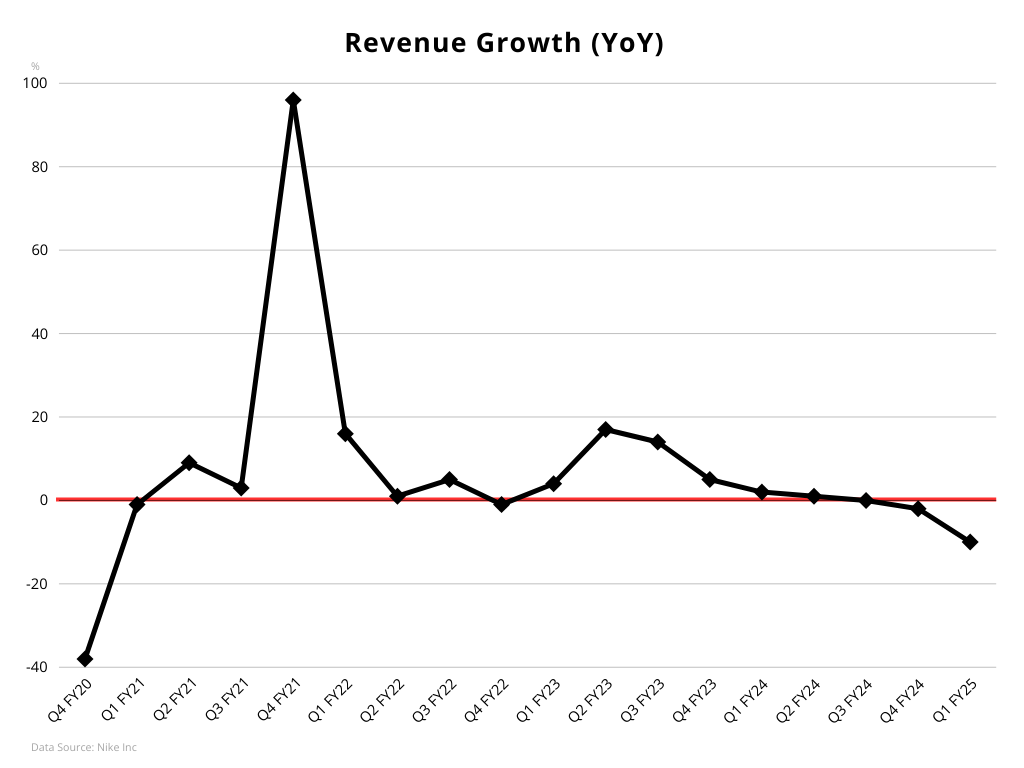

The June results were disappointing, but Wednesday's latest report for the June-August period revealed further deterioration [1]. Gross profits dipped 8% y/y in the first contraction in two years and net income plunged 28% y/y, marking the biggest drop in more than a year. More importantly, the declining sales trend deteriorated, as revenues contracted by 10% y/y. The company expects another 8-10% contraction in the current quarter and withdrew prior full year guidance for "mid-single-digits" drop.

These adversities reflect on the stock, which posted a record losing streak of eleven days in 2023 and the single worst day in late-June of the current year. NKE.us runs its third negative year, with losses of around 25% so far in 2024. Markets reacted negatively to this month's poor results and the stock rejected the pivotal confluence of resistances at the $90 region, provided by the EMA200 (black line) and the 38.2% Fibonacci of the December-July slump. This reaffirms the bearish bias and creates scope for fresh multi-year lows (70.64).

On the other hand, Nike has identified the issues and is already working to fix them. It is cutting costs, rekindling relationship with third party-retailers and accelerating innovation. It is also spending on marketing, with its demand creation expenses jumping 15% in the reported quarter, which included two major sporting events – the UEFA Euro 2024 football championship and the Paris Olympics. Macros are also improving as major central banks around the world are cutting rates thanks to lower inflation, while China implements massive stimulus to prop the economy and consumer spending.

Furthermore, Nike veteran Elliott Hill will take over as CEO later this month, replacing outsider John Donahoe after four years at the helm. Nike's recovery will largely rely on this change that represents a directional shift that can bring back the grassroots identity that made it successful and regain its cultural edge. Although headwinds are likely to persist, Nike may be close to the end of the tunnel and better days could lay ahead.

The stock may have bottomed out, rising more than 15% in the third quarter, as markets liked the leadership change and turnaround plans. If executives can deliver, then the stock can rebound further. NKE.us needs to take out the aforementioned critical resistance cluster at around $90 to pause the bearish bias and get the chance to push towards and beyond 98.06.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 02 Aug 2026 https://s1.q4cdn.com/806093406/files/doc_financials/2025/q1/v2/Q1-25-Press-Release-FINAL.pdf |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**