EUR/USD And The Post-Fed Path of Least Resistance

The US Federal Reserve announced on Wednesday the tapering of its Quantitative Easing program (QE) by $15 billion/month, to begin later in November. However, this was largely dovish, as the bank did not commit to the tapering pace beyond December and did not link the unwinding its asset purchases with future rate hikes, delivering overall the minimum of what was expected.

The US Dollar dropped on the news, sending the pair higher yesterday, but the tightening of monetary policy is expected to be supportive for the greenback, mostly against currencies that are backed by central banks that are behind the Fed in the policy normalization process.

The European Central Bank (ECB) is one of those, as it maintains at this stage a massive stimulus program, with its President Ms Lagarde, making some very dovish comments recently. The latest one came on Wednesday from Lisbon, as she commented that rate hikes are unlikely in 2022.[1]

On the Fed's side, nine officials saw higher interest rates as per the September projections[2], with next forecasts due in Decmeber, while markets are far more aggressive and see rate multiple hikes in H2 2022.

Furthermore, the Fed has a problem with high US inflation and although it maintains its transitory view, it is clear that it is less certain lately. A stronger USD would help contain inflationary pressures, while a lower Euro o the other hand can help the ECB sustain its expansive monetary policies.

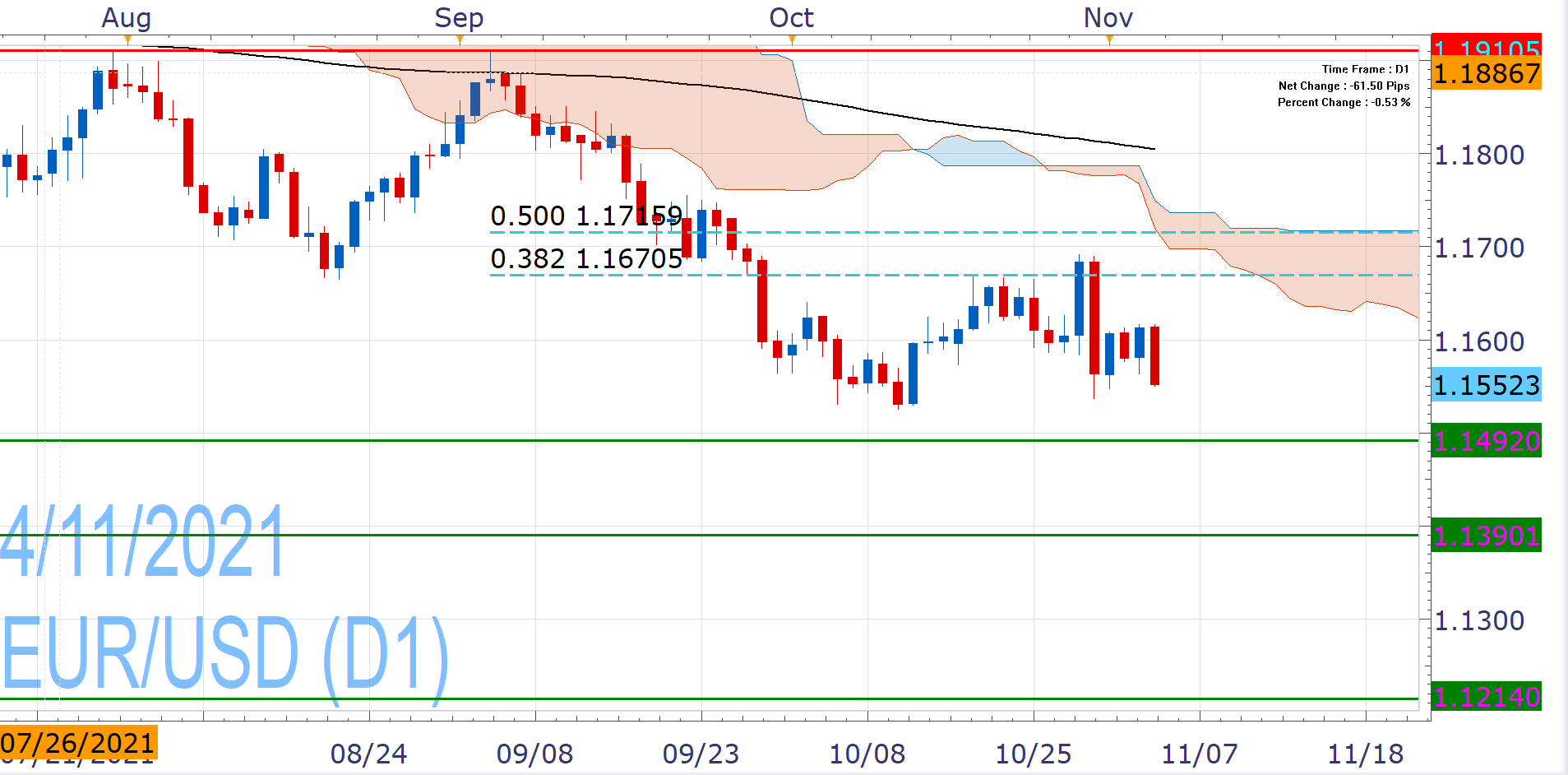

Given all this, the path of least resistance at this stage seems to still be lower for EUR/USD, which drops today and erases its post-Fed gains. From a technical prospective, it rejected the 38.2% Fibonacci of its last downward move (September - October) last week, creating heightened risk for fresh 2021 lows (1.1523), with the first support located at around 1.1500-1.1492. Further decline, will bring the 1.1400-1.1390 area in the spotlight, but it may still be early for such move.

On the other hand, the pair did stage a rebound after its October 2021 low and another similar effort could be in the cards, but the upside has significant obstacles.

Past Performance: Past Performance is not an indicator of future results.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 04 Nov 2021 https://www.ecb.europa.eu/press/key/date/2021/html/ecb.sp211103~d0720ef27b.en.html | |

| Retrieved 04 Nov 2021 https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20210922.pdf |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.