NVIDIA’s AI-Powered Rally Lifted the Tech Sector Amidst Debt Ceiling & Fed Uncertainty

NVIDIA AI Boom

Late last year, OpenAI launched ChatGPT, which is a generative Artificial Intelligence (AI) chatbot that generates human-like responses. This quickly took the world by storm and has become the next big thing, with tech giants such as Microsoft and Alphabet racing to offer similar services.

The development and deployment of these applications requires semiconductors and NVIDIA is well positioned to capitalize on the Artificial Intelligence boom. This was evident in Wednesday's quarterly results, which although overall a bit mixed, showed strong demand for the firms AI-related chips.

NVIDIA Rally Lifted NAS100

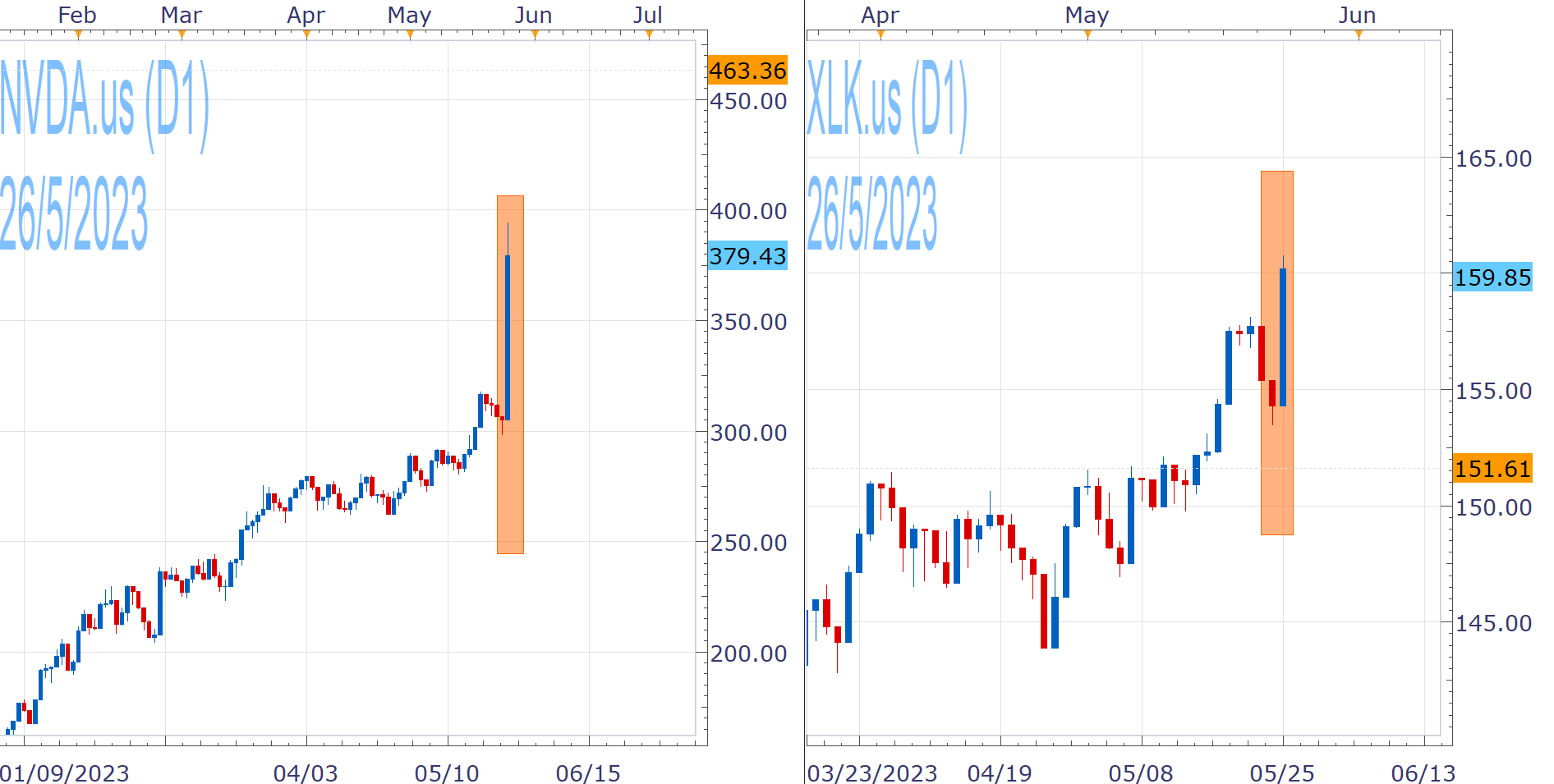

The quarterly results of the chip-designer, not only sent its stock (NVDA.us) to an around 25% rally on Thursday and new record highs, but fueled a rise of the broader tech sector. The Spdr Technology Fund (XLK.us) jumped more than 3% to the highest levels in over a year.

This also helped the tech-heavy NAS100 into a strong day and fresh 2023 highs, outperforming the wider SPX500, which posted only marginal gains yesterday. NAS100 is having a blockbuster 2023, as tech companies recover from last year's disappointing performance and the AI boom has provided momentum.

The index has exited the bear market, which started after the November 2021 all-time highs and has stepped firmly into bull territory, since it gains more than 30% from the October 2022 2+year lows. A 20% rise from a recent low is generally considered the threshold for a bull market designation.

However, the index faces some headwinds, stemming mainly from the hawkish repricing in market expectations around the Fed's policy outlook and the uncertainty around the debt ceiling negotiations.

Fed Repricing

This year's rally has also been fueled by market hopes for an end to the Fed's tightening cycle, which was detrimental to stock markets in 2022, but also for rate cuts later this year. The Fed has become more conservative and pointed at a pause earlier in the month, due to the lagging nature of hikes and the expectied credit tightening from the recent banking turmoil.

However, this tightening does not appear to be that significant for now, the labor market remains very tight and inflation is elevated and far from the 2% target. This can make a hold hard and could lead to more monetary firming, while rate cuts have been generally dismissed by policymakers.

This has created a hawkish repricing around the Fed's policy path, which creates headwinds for the stock market. CME's FedWatch Tool assigns the highest probabilities to one more hike (to 5.50%) and to rates ending the year at 5.00%.[1]

Debt Ceiling Uncertainty

Furthermore, investors also grapple with the debt ceiling drama, as Democrats and Republicans have not yet come to an agreement to avoid a default. Treasury Secretary Yellen, has repeatedly estimated that the US government could become unable to pay all of its bills as early June 1 (X-date). [2]

Credit Rating Agency placed the US AAA rating on negative watch this week, as it believes that "risks have risen that the debt limit will not be raised or suspended before the x-date", although it still views a timely resolution as the more likely outcome. [3]

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.