Market Threads – Oil Continues to Consolidate

.png)

Tracking important market threads across currencies, commodities, and indices.

- Oil at a crossroads: resilient charts, rising geopolitical risk, and the key signals every trader needs to watch next.

- Is the US dollar preparing for another leg lower, or will sticky inflation and a hawkish Federal Reserve reignite support for the greenback?

- Gold approaches a critical breakout as Fed uncertainty, sticky inflation, and rising oil prices collide with resilient institutional demand.

- The SPX500 keeps surging on AI optimism and resilient earnings, but rising inflation, oil, and stretched valuations could test the rally next.

Cross-Asset View

One of the most compelling stories in markets is the relationship between oil, the dollar, gold, and equities. Oil remains elevated above $100 a barrel as Middle East tensions and disruption around the Strait of Hormuz keep supply fears alive. That is feeding directly into inflation, with US CPI accelerating to 3.8%, strengthening the dollar as traders push back expectations for Federal Reserve cuts and even price in a small chance of another hike.

Normally, a stronger dollar and higher yields would pressure gold, and gold has indeed softened near $4,700/oz. Yet it has not broken down, suggesting that central bank demand and geopolitical hedging remain powerful forces.

Meanwhile, the S&P 500 has backed off record highs but continues to find support from AI-driven earnings optimism. In short, oil is driving inflation, inflation is supporting the dollar, the dollar is testing gold, and equities are still trying to bet that earnings can outrun all of it, at least for now.

Oil

Techncial Analysis

Last week, we flagged potential topping patterns in UKOil and USOil. While there was some initial downside follow-through, oil has so far remained resilient. A broader topping process may still be developing, but we need to see clearer confirmation before that view gains conviction.

For now, both charts are showing signs of congestion, with their respective Relative Strength Index (RSI) readings oscillating around the 50 level. The longer RSI remains anchored near 50, the greater the likelihood that this consolidation phase continues to unfold.

If oil is genuinely in the process of topping out, we would need to see RSI break below 50 and hold there. Until that happens, the case for materially lower oil prices remains unconvincing.

Fundamental Perspective

Crude eased after a sharp rally, but oil prices remain elevated as the Middle East conflict continues to disrupt global supply. Pressure is growing on Iran's exports, with signs of reduced shipments from key terminals and the Strait of Hormuz still heavily restricted. While Donald Trump has tried to calm markets ahead of talks with Xi Jinping, rising fuel prices are adding inflationary pressure and political risk at home. For now, traders appear to be pricing in a prolonged period of tight supply, keeping the oil market supported despite short-term pullbacks.

The USDOLLAR

Technical Analysis

The USDOLLAR is showing signs of weakness. On the daily chart, it has formed a lower peak followed by a lower trough, suggesting the broader trend is bearish. The key question now is whether the index is in the process of forming the next lower peak in that sequence.

Momentum indicators are leaning in favour of the bears for now, with the Relative Strength Index (RSI) holding below the 50 mark, which typically reflects negative momentum. The longer RSI remains below this level, the greater the probability that dollar weakness persists and that another lower peak begins to take shape.

However, if RSI breaks back above 50, it would suggest momentum is shifting, potentially offering broader support for the greenback and challenging the current bearish structure.

Fundamental Perspective

Fundamentally, the US dollar looks better supported after hotter-than-expected inflation data reinforced the view that the Federal Reserve may keep rates restrictive for longer.

April CPI accelerated to 3.8% year-on-year, up from 3.3% in March, with energy costs, partly linked to elevated oil prices, accounting for over 40% of the monthly inflation increase. That keeps inflation well above the Fed's 2% target and reduces the likelihood of near-term rate cuts.

Higher Treasury yields and a repricing of Fed expectations have helped support the dollar, although sustained dollar upside likely still depend on whether oil remains elevated.

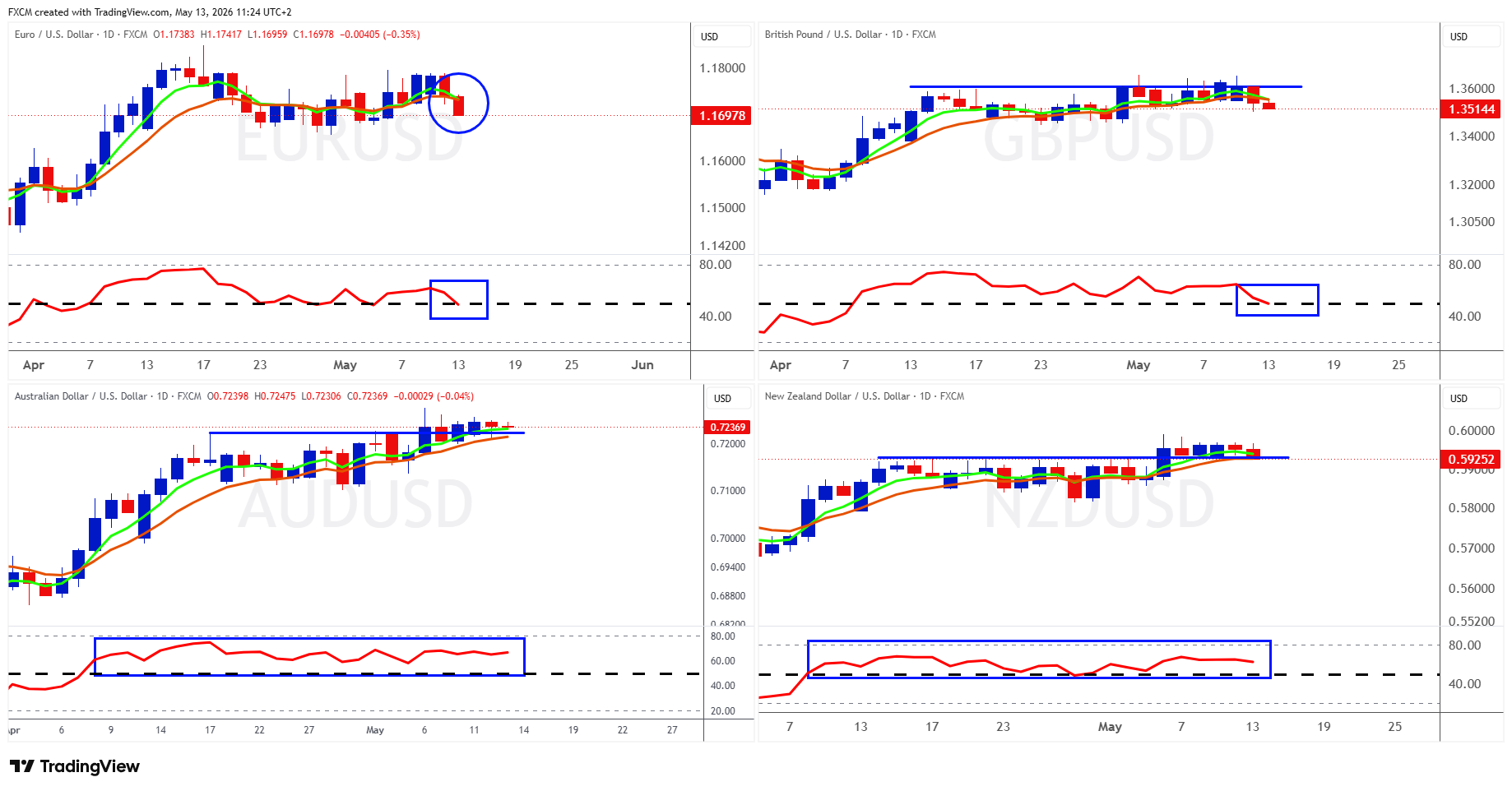

Some Currencies to Keep an Eye On

The top left shows EUR/USD, the top right GBP/USD, the bottom left AUD/USD, and the bottom right NZD/USD. The direction of the USDOLLAR will remain a key driver in determining where these currency pairs move next.

At the moment, EUR/USD appears to be losing momentum, with its Relative Strength Index (RSI) slipping below 50. If that persists, it would suggest further downside pressure for the euro. Sterling is showing a similar pattern, having failed to break decisively above the 1.361 resistance level.

The antipodean currencies, however, remain more constructive. Both AUD/USD and NZD/USD continue to hold RSI readings above 50, which suggests underlying momentum remains supportive of their respective base currencies.

Resistance at 0.72250 in AUD/USD and 0.59300 in NZD/USD is still proving influential. That said, if the USDOLLAR's RSI remains below 50 while the antipodeans continue to hold above 50, the path of least resistance still appears to be to the upside.

Gold

Technical Analysis

Gold's correlation with UKOil remains exceptionally strong, albeit inverse, at -91%. This means the two instruments continue to move closely, but in opposite directions. With UKOil largely consolidating in recent sessions, it is not surprising that gold has also drifted sideways over the past week.

The key level to watch for gold is 4,890. A break above this level would complete the double-bottom pattern we highlighted last week.

Momentum is mildly constructive, with the Relative Strength Index (RSI) holding above 50. If RSI continues to maintain this level, the probability begins to favour further upside. That said, a stronger bullish move in gold will likely depend on UKOil starting to weaken, and we still need clearer evidence of that.

Fundamental Perspective

Gold is caught in a macro tug-of-war. Hotter-than-expected US inflation has pushed Treasury yields and the dollar higher, forcing markets to scale back hopes of Federal Reserve rate cuts and even price in a small chance of further tightening.

That is normally a difficult backdrop for gold. At the same time, elevated oil prices, driven by continued disruption in the Middle East and restrictions around the Strait of Hormuz, are keeping inflation fears alive and reinforcing the Fed's higher-for-longer narrative.

Yet gold remains resilient near $4,700/oz, supported by persistent central bank buying and ongoing geopolitical uncertainty. In short, gold is no longer trading purely as a safe haven. It is increasingly becoming a test of whether inflation and energy shocks, or institutional demand, will dominate the next phase of the macro cycle.

Index in Focus: SPX500

Technical Analysis

The SPX500 has gained nearly 3% so far this month, building on April's impressive 10.75% rally. It is therefore no surprise that its Relative Strength Index (RSI) has pushed above 80, placing the index firmly in overbought territory (blue rectangle).

Notably, RSI has remained overbought since mid-April without a meaningful pullback in the index. This suggests there is a strong sense of momentum, and perhaps even excitement, driving continued buying in the large-cap names that are leading the market higher.

That said, caution is warranted. At some stage, RSI is likely to normalise, and that will probably be accompanied by some profit-taking and a pullback. However, as long as RSI remains above 50, any correction is likely to be constructive rather than a sign of broader weakness. In that scenario, support zones should be monitored for potential buy-the-dip opportunities, with the 7,200 level standing out as an important area to watch.

Fundamental Perspective

The SPX500 remains supported by a powerful mix of AI-driven earnings momentum, resilient US economic data, and an earnings season that has consistently beaten expectations. Roughly 83% of S&P 500 companies have beaten analyst estimates this quarter, while first-quarter earnings growth is tracking close to 29% year-on-year, driven largely by semiconductor and mega-cap technology names linked to the AI buildout.

The labour market has also remained firm, reinforcing the view that the US economy is proving more resilient than many expected.

However, risks are becoming harder to ignore. April US inflation accelerated to its highest level in nearly three years, pushing Treasury yields higher and reducing hopes of near-term Federal Reserve rate cuts. At the same time, Brent crude remains above $100 a barrel as Middle East tensions continue to disrupt supply, adding fresh inflation pressure.

In short, the market is still being driven by earnings and AI optimism, but with valuations stretched and breadth still relatively narrow, any disappointment on inflation, oil, or tech earnings could trigger a sharper bout of profit-taking.

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.