The Fed is Noticeably Behind the Curve

Introduction

The USD has been pulling back since its peaked in December. Moreover, the greenback has declined markedly since the CPI release yesterday, which showed inflation increasing at its fastest pace in 40-years. The pullback in the greenback may be a function of the "buy the rumour, sell the fact" phenomenon. I.e., markets are forward-looking, and FXCM's USDOLLAR basket accelerated its momentum upwards as far back as September last year. The green trendline shifted to a steeper gradient (the orange trendline) as momentum increased. The blue vertical marked the higher trough of the increased momentum, which was validated by the higher peak at the end of September. Now that the strong inflation is apparent, the market is selling off the dollar, to the point that the orange trendline is being threatened (aqua rectangle).

.png)

Past Performance: Past Performance is not an indicator of future results.

The Monetary Policy Lag

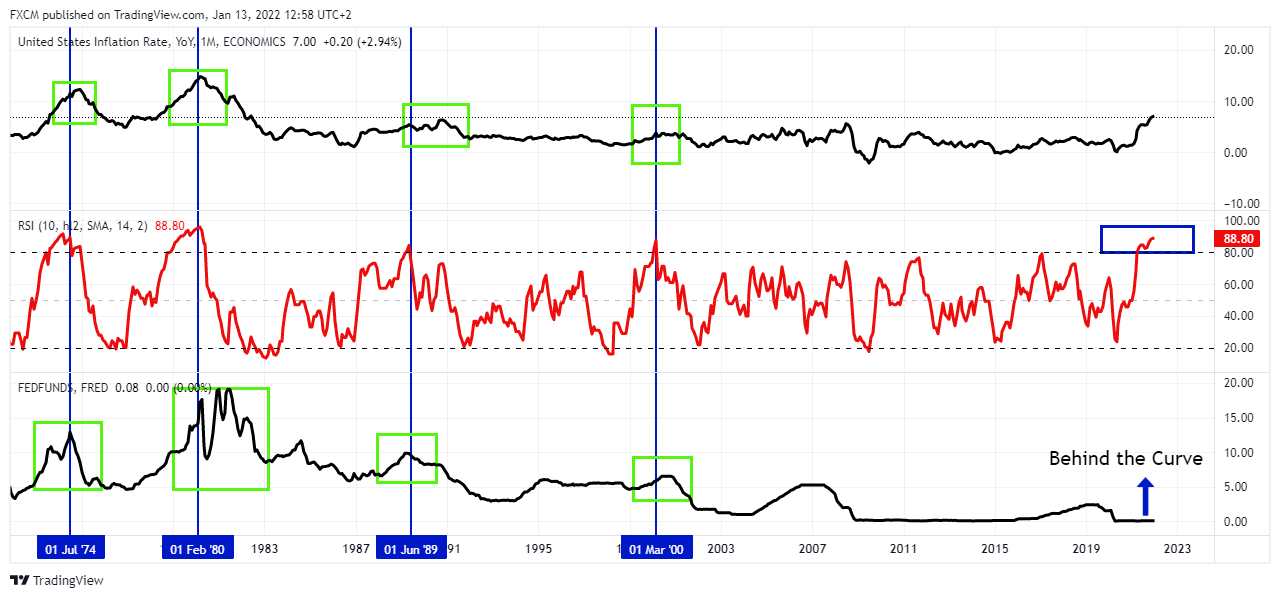

Given that this is the fastest pace of inflation since the 1980s, the below chart is informative. The top chart is the US inflation series, the middle chart is its RSI, and the bottom chart is the federal funds rate as a proxy for general monetary policy. The blue vertical lines indicate an overbought condition in the US inflation series. The blue rectangle is the current overbought condition. It is no surprise that the early 80s also show as overbought, given that the current rate of change in inflation is similar. Of interest, June 1989 and March 2000 show overbought conditions as well. So, there are 3 obvious overbought conditions in the inflation RSI before the current reading. On each of those three occasions, the federal funds rate had already been hiked by the Fed i.e., monetary policy was already contractionary (green rectangles). July 1974 is outside our period, but it shows similar. Noticeably, this is not the case this time. This time the Fed is behind the curve.

Source: www.tradingview.com

Past Performance: Past Performance is not an indicator of future results.

Possible Reasons For the Lag

One may argue that the pandemic was an exogenous shock to the system that has been strong enough to alter normal monetary policy trajectory. Another reason might be the change of measurement by the Fed in meeting its price stability mandate. At Jackson Hole in 2020, it announced a target of an average rate of 2%, as opposed to an absolute target of 2%. Moreover, the unlimited QE may have caused some damage to market mechanisms regarding the demand and supply of long-term bonds. Market expectations suggest that inflation is likely near its apex. However, keep in mind that the current monetary policy experiment is still ongoing as the Fed now looks to normalise a bloated $8.8tn balance sheet. I.e., variables may be present that were absent before. This may impact on the transmission of economic information. As such, the current selloff in the USDOLLAR may provide an opportunity i.e. a potential "buy the rumour, sell the fact" moment as hypothesised above. As such, we continue to monitor.

Featured Image by Steve Buissinne from Pixabay

Russell Shor

Senior Market Strategist

Russell Shor is a Senior Market Strategist at FXCM, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.