Netflix Strategic Changes Led to User Base Expansion & Record Revenues in Q2 2023

Key Points

-Netflix made two strategic changes to its business after a poor 2022, cracking down on password sharing and launching a new subscription plan with the inclusion of advertisements.

-According to Wednesday's results, these initiatives had a positive impact to its financials and user metrics.

-The streaming giant added 5.89 million subscribers in Q2 2023 and Revenues hit new record highs of $8.187 billion.

Strategic Business Changes

After very bad first half in 2022, Netflix was forced to rethink key aspects of its business, with a new policy to limit/monetize password sharing and the launch of an ad-supported subscription tier. Progress on those initiatives will be crucial for its future, with the first sign being positive.

Password Sharing Crackdown

Netflix had allowed password sharing for a long time, with no real efforts to contain it, since this practice had helped it grow in the early days of streaming. Back in January it had estimated a "wide" account sharing, to the tune of 100 million households, which "undercuts its long term ability to invest in and improve" the platform [1]. The company could not afford this and the revenue headwinds it was creating, amidst the challenging external environment of the past year and began testing ways to limit and monetize sharing.

The new sharing policy limits account access to one household and allows owners to add extra member for an additional monthly fee. The streaming giant implemented a broader rollout of its new password sharing policy in May to more than 100 countries, including the US and the UK. On Wednesday, it said that the new policy is now being rolled out to almost all of the remaining countries. [2]

The firm noted that "the cancel reaction was low", with a "healthy" conversion of borrowers to paying members. In the post-results earnings calls, co-CEO Greg Peters declared that the new password policy is "working", adding that "we're positive in terms of both revenue and subscribers" compared to pre-launch on all regions. [3]

Ad-Supported Tier

After years of resisting, Netflix crossed its advertising Rubicon in November, with the launch of a cheaper ad-supported subscription plan in the US and elsewhere, undercutting rival Disney in both timing and pricing. [4]

I have long maintained that the inclusion of advertisements is the future of the direct-to-consumer (DTC) market, especially in this environment of post-pandemic consumer behavior, increased competition and high inflation. It can create an additional revenue stream and allow Netflix to be less focused on subscriber growth, while at the same time it provides a lower entry point for prospective clients.

According to Wednesday's Q2 shareholder letter, members on the advertisement inclusive plan "nearly doubled" since the first quarter, although still being a small part of its user base. The DTC giant is already evolving its ads strategy, phasing out the cheapest ads-free Basic plan in the US and UK, after having done so in Canada recently. [2]. In the relevant earnings call, CFO Spence Neumman said that execs are "pleased with our per member ad economics", noting that the overall Average Revenue per Membership (ARM) of the ads plan, "continues to be higher" than the basic ad free one.

User Base Expansion

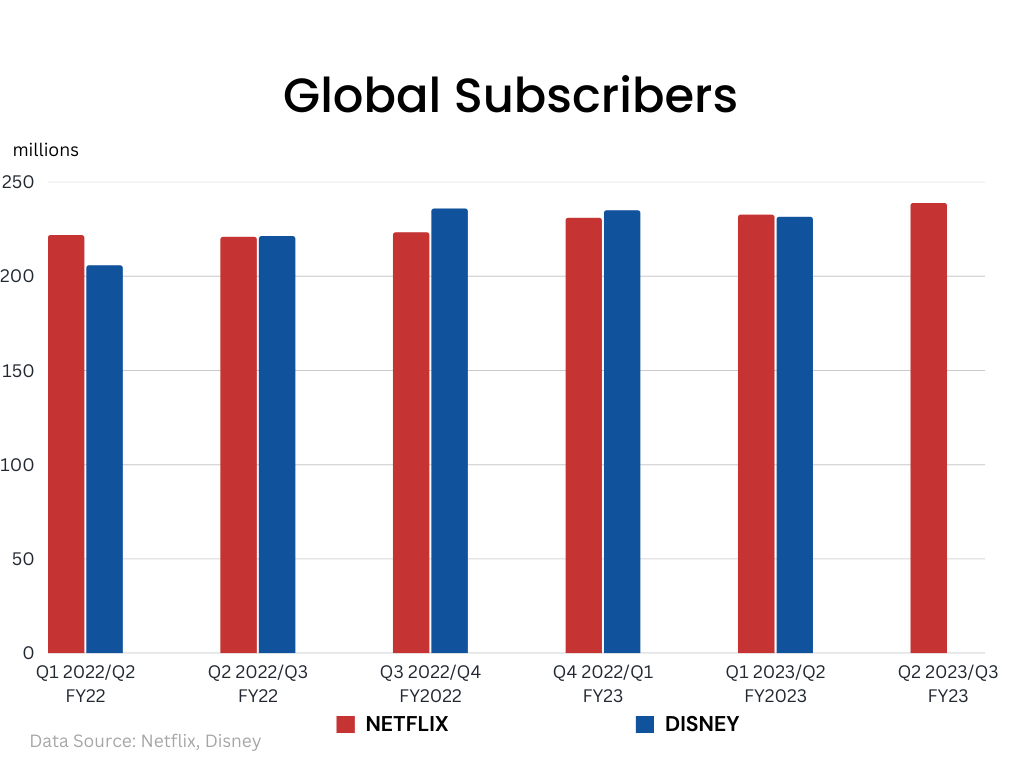

These new initiatives helped the streaming giant expand it user base by 8% y/y, the largest growth in over a year, adding a robust 5.89 million subscribers in the second quarter. This raised total members to 238.39 million, giving it a good chance of staying ahead of Disney, which reports in early-August.

Netflix had lost subscribers in the first half of the past year, conceding the top-spot to its rival. However, it returned to user growth after that and was able to regain the lead in Q1, as Disney has seen its subscriber base dwindle over recent quarters.

Although it has stopped providing explicit forecast, the firm expects net additions in Q3 to be "similar" to the ones reported for the second quarter. This isn't exactly awe-inspiring, but would still constitute strong expansion.

Solid Financials & Guidance

The positive impact of the firm's strategic initiatives was evident in the top and bottom lines, as well as the forward guidance, since Revenues reached new records of $8.187 billion, up 2.7% y/y. The firm forecasts sales to increase further to $8.52 billion in the third quarter and growth to accelerate by 7.5% up y/y.

The company's commentary was reveling, since it attributed the projected acceleration to the fact that the "full benefits' of the paid sharing policy and the growth of the ad-supported plan, will filter through. During yesterday's earnings call, CFO Spence Neumann spoke of paid sharing as the "primary revenue accelerator" this year. [3]

However, the Q2 Revenues fell somewhat short of the firm's own projections, while y/y growth is still low for its standards. Furthermore, the Q3 projection seems a bit underwhelming. Although the boost from the strategic changes is in the right direction, it may not be enough to satisfy investors.

Net Income expanded 14% q/q to $1.339 billion, but was little changed from a year ago. Operating Margins of 22.3%, showed notable improvement on both yearly and sequential comparison.

Free Cash Flow of $1.339 billion was lower than the $2.117 of Q1, but still marked a huge improvement compared to a year ago, when FCF was almost non-existent. More to it, Netflix upgraded its 2023 outlook to at least $5 billion, due to lower cash content spend caused by the strike of US writers and actors.

Increased Competition

The direct-to-consumer market is saturated and Netflix is no longer the clear-cut leader. It has to battle legacy media behemoths, which despite recent struggles, have very strong content. Its arch-rival Disney has two of the most important franchises in Hollywood, the Marvel Cinematic Universe (MCU) and Star Wars and is able to leverage that into its streaming platforms.

WarnerBros.Discovery has a huge slate of fan-loved movies, such as the Harry Potter series, but most importantly, the perennial TV success story: HBO. Videogame based "The Last Of Us" averaged 32 million viewers, making it the most watched show on the company's streaming platform in both Europe and Latin America [5]. The finale of the award-winning drama "Succession", drew in 2.9 million users across streaming and linear channels. [6]

Meanwhile. tech giants like Amazon.com and Apple with their deep pockets, are making progress in the streaming arena. Thy have already produced critically acclaimed and popular content, with the latter becoming the first streamer to win the Best Picture Oscar with CODA last year. [7]

What's more, Netflix lacks a live sports offering, something most of its main rivals offer. If it wants to fend them off, it will eventually have to tap that market. This would also be a logical next step after the ad-supported tier, since sports matches are well-suited for ad placement, given half-times, time-outs and other factors. This is a technically and economically difficult endeavor though. Co-CEO ted Sarandos alluded to that yesterday and seemed happy to stick to the current "sport adjacent" programs, for now at least. However, It is experimenting and will host a standalone live golf match in a few months. [3]

Conclusion

The adversities of the previous year, forced Netflix to change key aspects of its business. It acted swiftly with a new password sharing policy and a subscription plan with the inclusion of advertisements. The firm has to get this right, given the still challenging external environment and intense competition.

Yesterday's Q2 report showed good progress on these initiatives, which boosted its user base, as well its top and bottom lines. However, investors appear to have been expecting faster progress. In fact, the stock of Netflix dropped after-hours, following Wednesdays results.

The main disadvantage of Netflix in my view is content. Although it has a huge catalog, it has no live sports and can't match legacy entertainments giants, which have decades worth of content. However, these companies have been facing difficulties recently and trying to rationalize their businesses. Furthermore, Netflix may have an edge in weathering the strike of US writers and actors, given its foreign programming.

Overall, Netflix is not the undisputed king of streaming anymore, but the strategic changes it has implemented can help it stay ahead, if it can build on the early encouraging signs.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 20 Jul 2023 https://s22.q4cdn.com/959853165/files/doc_financials/2022/q4/FINAL-Q4-22-Shareholder-Letter.pdf | |

| Retrieved 20 Jul 2023 https://s22.q4cdn.com/959853165/files/doc_financials/2023/q2/FINAL-Q2-23-Shareholder-Letter.pdf | |

| Retrieved 20 Jul 2023 https://s22.q4cdn.com/959853165/files/doc_financials/2023/q2/netflix-inc-q2-2023-earnings-call-jul-19-2023.pdf | |

| Retrieved 20 Jul 2023 https://about.netflix.com/en/news/announcing-basic-with-ads-us | |

| Retrieved 20 Jul 2023 https://s201.q4cdn.com/336605034/files/doc_financials/2023/q1/WBD-1Q23-Earnings-Release-Final-05-04-23.pdf | |

| Retrieved 20 Jul 2023 https://press.wbd.com/na/media-release/hbo-0/succession-finale-draws-series-high-29-million-viewers | |

| Retrieved 01 Jul 2026 https://www.oscars.org/oscars/ceremonies/2022 |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.