Is the Fed’s Hawkisness Waning?

Hawkish Fed

The US central bank has adopted an increasingly hawkish stance over the last few months, pivoting quickly towards a faster normalization of its ultra-loose monetary policy. It shifted its focus away from the labor market, to persistent high inflation, which is the main driver of it actions and which it recently stopped calling "transitory".

This rethink on inflation was worded by Mr Powel in his November 30th 2021 Senate testimony [1] and any "transitory" reference was omitted from the next policy statement.

At the beginning of that month, the central bank had announced a reduction of its asset purchases to the tune of 15/billion and another 15 billion in December. [2]

In the last meeting of 2021 in December, the Fed announced an accelerated reduction plan [3] that is expected to conclude the Quantitative Easing (QE) program by March of the current year, despite the rise of the Omicron variant.

Furthermore, bank officials projected three rate hikes in 2002, as per the accompanying dot-plot. [3].

Minutes of that December policy meeting were released last week and revealed even more hawkishness amongst officials, since ""Almost all participants agreed that it would likely be appropriate to initiate balance sheet runoff at some point after the first increase in the target range for the federal funds rate." [4]

Powell Nomination Hearing

Two months ago, US President Biden had nominated mr Powell for a second term as the Chair of the Board of Governors of the Federal Reserve System and the relevant hearing took place at the Senate yesterday. [5]

During his testimony, Mr Powell confirmed the end of asset purchases in March and that that the balance sheet reduction will be "sooner and faster" compared to the previous time the Fed had been down this road.

As to the timing of interest rates and the balance sheet unwinding, he said that "…meaning we will be raising rates over the course of the year, at some point perhaps later this year allow the balance sheet to run off."

This is a markedly more reserved approach, compared to last week's minutes and recent commentary by some Fed members, as mr Powell may want avoid being constrained into a predetermined tightening path.

Market Expectations

Market expectations around rate hikes have been rather aggressive, bolstered by the Fed's hawkish actions and commentary. This is reflected in the rise of US bond yields and the CME's FedWatch Tool, which projects lift-off in March. [6] and was not very deterred by yesterday's commentary.

At the time of writing, it also projected 29.4% probability of a fourth rate hike in December 2022, exceeding the Fed's dot-plot estimates.

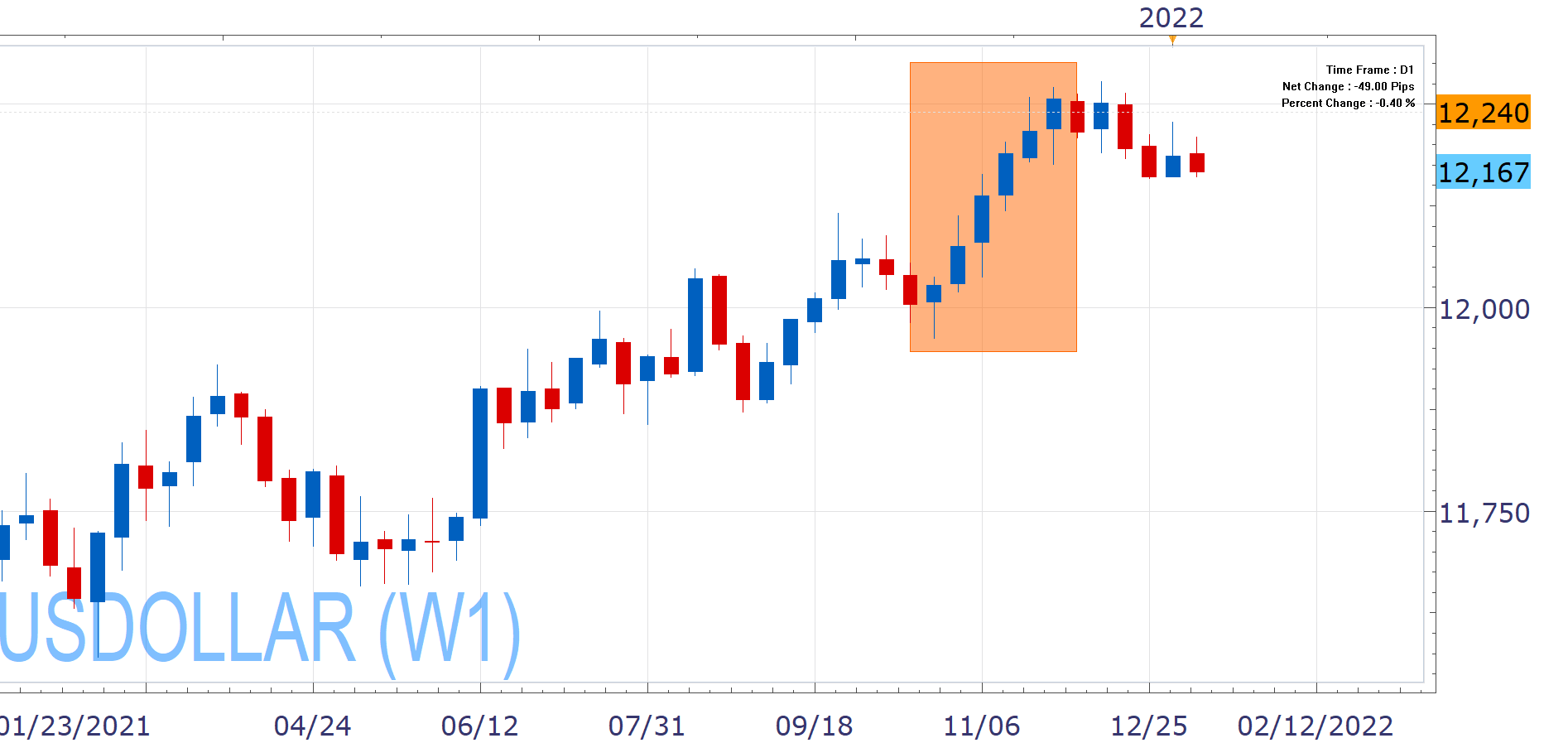

US Dollar Reaction

The Fed's hawkish pivot has been a source of strength for the US Dollar, which had ran a six-week profitable streak from late-October to early-December, but has since been facing headwinds, with December being negative.

Past Performance: Past Performance is not an indicator of future results.

QE conclusion in March is a given as per the central bank and if the first rate hike is not produced then, it will probably be a source of disappointment for the USD bulls.

The third tool of policy normalization, the sale of assets has the potential to continue to fuel hawkish expectations, but Mr Powell was reserved around its timing yesterday and the US Dollar reacted lower.

However, the US central bank is far ahead than some of its major counterparts in the policy normalization process and its rhetoric has been more aggressive than most in regards to the next steps, which has the ability to continue supporting the US Dollar.

The Fed's next monetary policy meeting takes place on January 25-26.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 12 Jan 2022 https://www.banking.senate.gov/hearings/cares-act-oversight-of-treasury-and-the-federal-reserve-building-a-resilient-economy | |

| Retrieved 12 Jan 2022 https://www.federalreserve.gov/monetarypolicy/files/monetary20211103a1.pdf | |

| Retrieved 12 Jan 2022 https://www.federalreserve.gov/monetarypolicy/files/monetary20211215a1.pdf | |

| Retrieved 12 Jan 2022 https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20211215.pdf | |

| Retrieved 12 Jan 2022 https://www.banking.senate.gov/hearings/01/04/2022/nomination-hearing | |

| Retrieved 28 May 2026 https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html# |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.