Big Tech earnings preview: fresh AI optimism confronts mounting risks

A volatile external environment to test AI momentum

The earnings season hits a critical inflection point as five of the Magnificent Seven report within forty-eight hours - from April 29 to April 30. Meta, Alphabet, Amazon, Microsoft and Apple, all at the heart of the AI narrative, are scheduled to release their results. These come against a volatile global backdrop and the outcome can shape the trajectory of not just these stocks, but the SPX500 and global indices.

These earnings arrive amid a wave of renewed AI optimism that has propelled shares higher this month, buoyed by robust guidance from ASML and TSMC, the essential chokepoints of the semiconductor industry. Markets are currently betting that trade disruptions and the economic fallout from the Middle East conflict will not derail AI momentum or the critical data centre buildout. There is sound logic to this: the proliferation of AI appears unstoppable, with more firms developing LLMs, midsized models gaining traction and Agentic AI emerging as a powerful new accelerant.

However, risks are mounting and investors have become increasingly discerning, shifting from blind optimism to a focus on winners versus laggards. An upbeat narrative may not be enough to satisfy them and monetisation proof will likely be required. The Middle East conflict has complicated an already precarious macroeconomic environment, exacerbated by lingering tariff uncertainty. Rising energy prices have stoked stagflation fears, threatening to push the Federal Reserve and other major central banks toward tighter monetary policy, with the IMF downgrading its 2026 global growth forecast. [1]

For tech giants, this creates a double-edged sword. Higher costs of living may dampen consumer spending on discretionary items such as electronics. Simultaneously, macro uncertainty threatens to cool corporate investment and advertising spend - the lifeblood of platforms like Meta and Alphabet. Should growth falter, markets could quickly sour on the massive capital expenditures these companies continue to allocate toward AI infrastructure. Furthermore, disruptions to energy flows and critical materials supply pose real-world hurdles, adding costs to the maintenance and expansion of these vital networks.

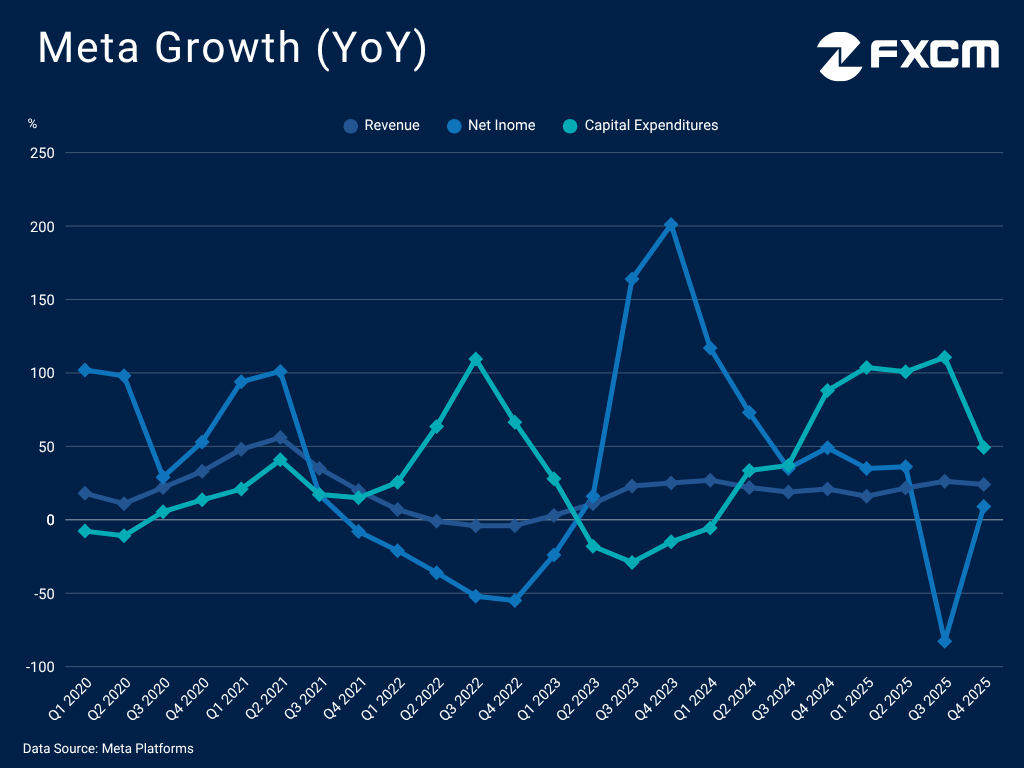

Meta Platforms

Meta is attempting to sharpen its AI edge with the release of Muse Spark, its latest model [2]. This launch marks a pivotal shift for the company as it is the first release under its "Superintelligence" unit, and represents a clear departure from its prior open-source strategy, a move intended to prioritise monetisation over ecosystem-wide adoption.

This transition comes on the heels of a strong quarter, driven largely by the tangible impact of AI on the advertising business. Ad impressions accelerated 18% y/y in Q4, while the company's Generative Ads Recommendation Model (GEM) drove a 3.5% lift in ad clicks on Facebook [3]. The momentum is so significant that eMarketer projects Meta Platforms will overtake Google in global digital ad revenue for the first time this year [4], a historic milestone driven by its superior AI-powered targeting.

Meta's top and bottom lines picked up in the fourth quarter and management expects revenues to rise 23.8%-30.7% y/y in Q1, marking a substantial growth boost. This could in turn keep investors calm regarding the massive AI investments. The company targets capital expenditures of $115-135 billion in 2026, representing an increase of at least 59.2% from last year.

However, the margin for error is razor-thin. Meta is uniquely exposed to macroeconomic volatility as its revenue is almost exclusively derived from advertising. Any softening in marketing budgets could translate directly into slower growth, testing the market's tolerance for the company's ballooning capex.

Furthermore, Meta faces a nuanced execution risk around user experience. Should the push to embed AI into the feed lead to a degraded experience, there is a risk of damaging the high engagement levels across its apps. Its consumer-facing chatbots also remain far less popular than those of OpenAI, Google and others, even if accurate measurements are hard to come by.

Shares of Meta Platforms are at a crucial juncture, with a golden opportunity to extend their April gains should earnings and guidance convince markets. Still, technical progress has been choppy and META remains at risk of renewed weakness.

Chart source: www.tradingview.com

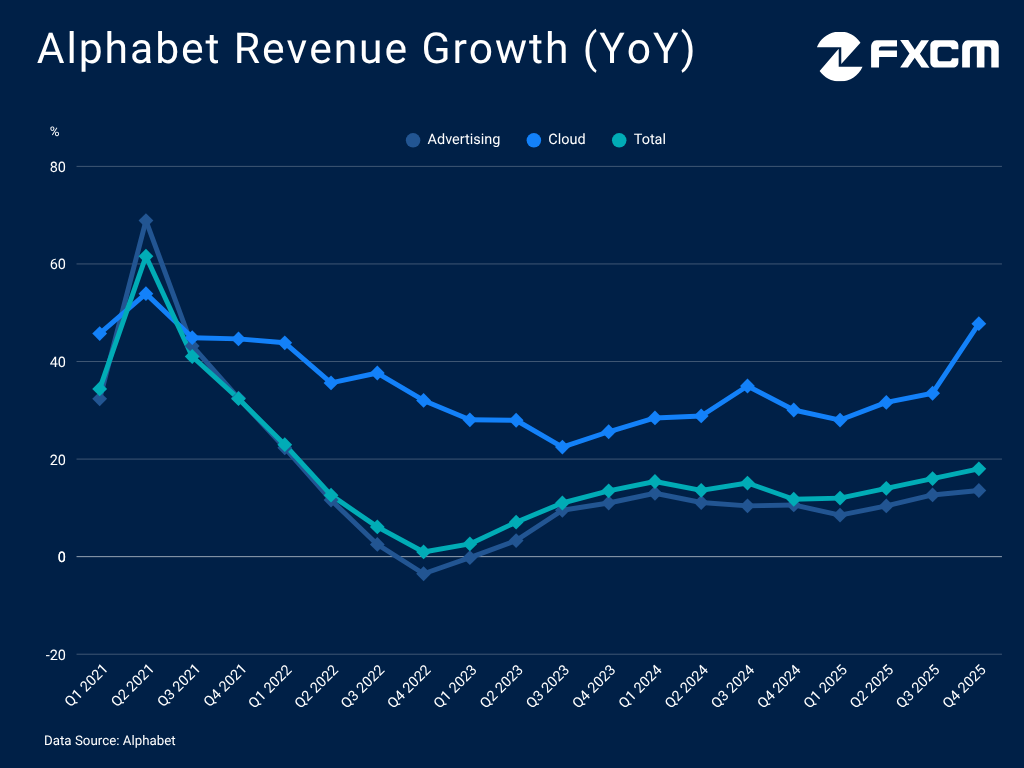

Alphabet

Wednesday's earnings arrive as Alphabet rides high on AI momentum, having successfully transitioned from a perceived laggard to a clear frontrunner. Its latest Gemini models have been well received, and the Stanford University 2026 AI Index report corroborates this, confirming that the performance gap between top-tier frontier models has effectively converged [5].

Beyond the benchmarks, Google is weaving Gemini directly into its ecosystem, making it easily accessible on Android and integrated into everyday apps like Gmail. Furthermore, Apple's decision to leverage Gemini to power its Siri overhaul [6] serves as a powerful validation of Alphabet's leadership, signalling that even the world's most valuable companies are looking to Google's infrastructure as the foundation for their next-generation AI.

Meanwhile, Alphabet is developing its own custom silicon, bolstering self-reliance, cost efficiency and LLM performance. This benefits its cloud business, which saw revenues jump nearly 50% y/y in Q4 - the fastest pace in over four years, with a backlog that more than doubled [7]. This momentum complements rising advertising sales and overall revenues, while an expansive and diverse product portfolio provides a degree of insulation against macroeconomic volatility.

However, this aggressive pivot is not without risks. AI proliferation threatens to cannibalise search dominance and affect click-through rates, while Meta is expected to overtake Alphabet in digital ad spend this year [4]. Stagflation risks could also weigh on global marketing budgets. And while Google Cloud is expanding rapidly, it remains a challenger behind Amazon and Microsoft.

Alphabet remains a solid performer with its shares firmly in positive territory this year, thanks to its AI leadership and overall business strength. Should results and guidance sustain the momentum, the stock could extend its advance to new all-time highs. But expectations are high and any disappointment could renew pressure and a drop below the EMA200 would negate the bullish bias.

Chart source: www.tradingview.com

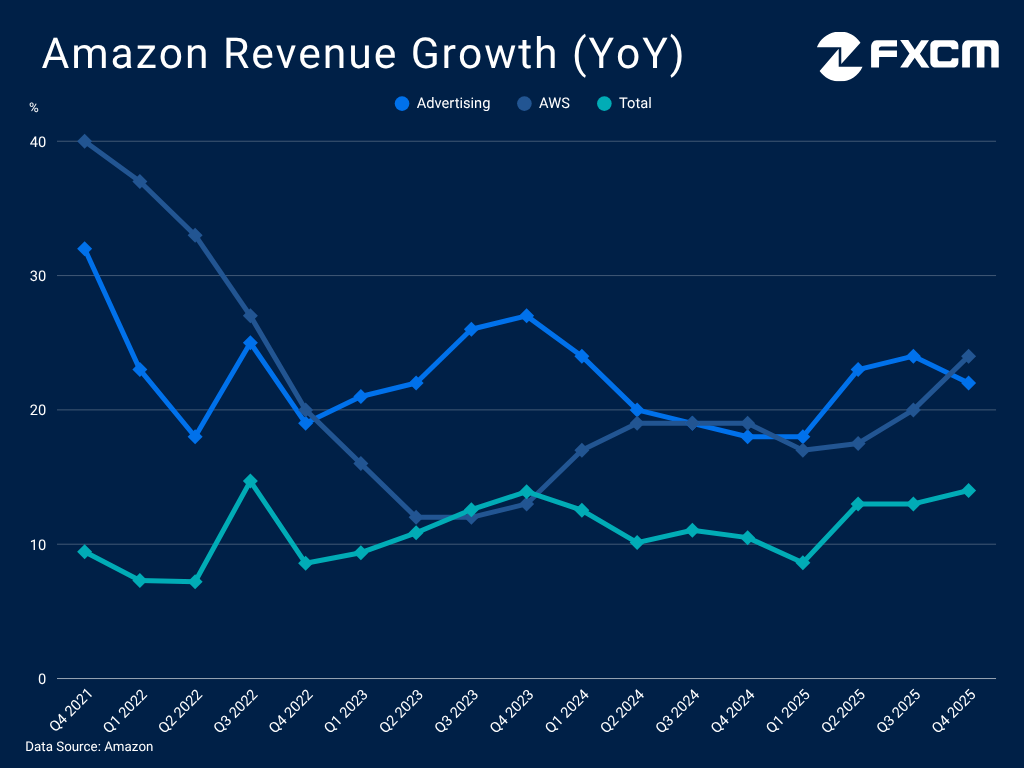

Amazon

Markets reacted negatively to Amazon's last report due to mixed numbers and a plan to boost 2026 spending by more than 50% to $200 billion. The current difficult external environment from tariffs and higher energy costs could intensify these concerns. Ad sales could decelerate further, the e-commerce business could face headwinds and costs could rise. Overall revenues have been stagnant in recent quarters and the situation could deteriorate based on Amazon's guidance, which points to a potential revenue slowdown and operating income that could even contract (the projection ranges from -10% to +16.9%). [8]

Nonetheless, CEO Andy Jassy has touted very strong demand for AI workloads and cloud services. Amazon Web Services (AWS) remains a bright spot and revenue growth momentum could continue in the reported quarter and beyond, which would justify the heavy spending.

The tech giant is cementing its dominance by locking in multi-billion dollar infrastructure commitments from industry leaders like Anthropic and OpenAI, ensuring its cloud services remain the backbone of the AI era. Amazon.com is also accelerating its custom AI chip development to increase independence, catalyse AI progress and potentially create a new revenue stream, as the CEO has opened the door to third-party chip sales. [9]

Additionally, Amazon's advertising prowess continues to expand. By leveraging proprietary AI-driven optimisation tools, the unparalleled depth of its first-party e-commerce data and the growing reach of Prime Video commercials, the company is effectively transforming its ad business into a full-funnel engine capturing an increasing share of total digital marketing budgets.

Amazon.com is a top Magnificent Seven performer this year, thanks to this month's surge. With the formation of a Golden Cross, it is well positioned to extend its gains as it progresses on the AI front. But the last disappointment acts as a cautionary tale and any new miss would push the stock lower. The advance also looks technically stretched as indicated by the RSI, creating scope for such moves.

Chart source: www.tradingview.com

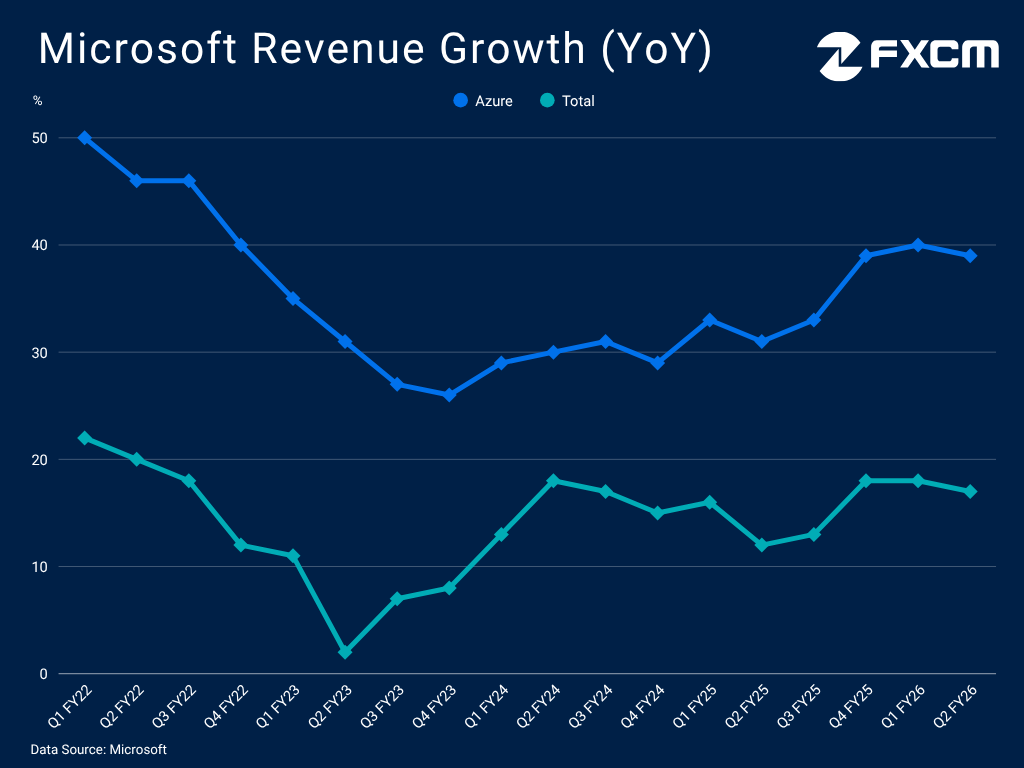

Microsoft

The tech giant is under increasing pressure to demonstrate a tangible return on investment for its massive AI-driven capital expenditures, which are on track to nearly double in FY26 and approach $150 billion. Markets were disappointed with the soft forward guidance of the last report, setting a difficult precedent. Management anticipates Azure revenue to grow at a slower clip of 37-38% y/y in Q3 FY26, a trajectory that could weigh on overall sales growth, while operating margins are projected to contract slightly [10]. Unless Microsoft exceeds these forecasts, markets may react negatively once again.

Although demand for its cloud services has continued to "exceed" supply, management faces a precarious balancing act between prioritising capacity for Azure and its internal AI product roadmap. The company also faces intensifying competition in the enterprise and Agentic AI space from rivals like Salesforce and ServiceNow. Microsoft's Copilot suite struggles to establish itself as a must-have utility. With 15 million paid seats against a base of 450 million M365 users, the implied 3.3% penetration rate is uninspiring. Against mounting stagflation risks, adoption faces further headwinds, leaving the company vulnerable to broader macroeconomic pressures.

However, Microsoft is playing the long game, leveraging the ubiquity of Teams and its M365 suite to remain the indispensable staple of corporate productivity. This entrenched position naturally facilitates Azure adoption, while its high-margin cybersecurity portfolio drives deeper enterprise integration. Despite the risks, Microsoft's reach across diverse, mission-critical sectors offers a significant buffer against macroeconomic headwinds, reinforcing its structural resilience relative to more specialised competitors.

MSFT is in the red this year and the worst-performing Magnificent Seven peer, as markets are not convinced about its ability to monetise its AI investments. If this perception persists after Wednesday's results, the bearish bias could be reaffirmed, opening the door to deeper declines as a technical Death Cross has formed. On the other hand, the lower valuation may support the stock's appeal should strong signals emerge from the earnings report, potentially opening the door to a more meaningful advance.

Chart source: www.tradingview.com

Apple

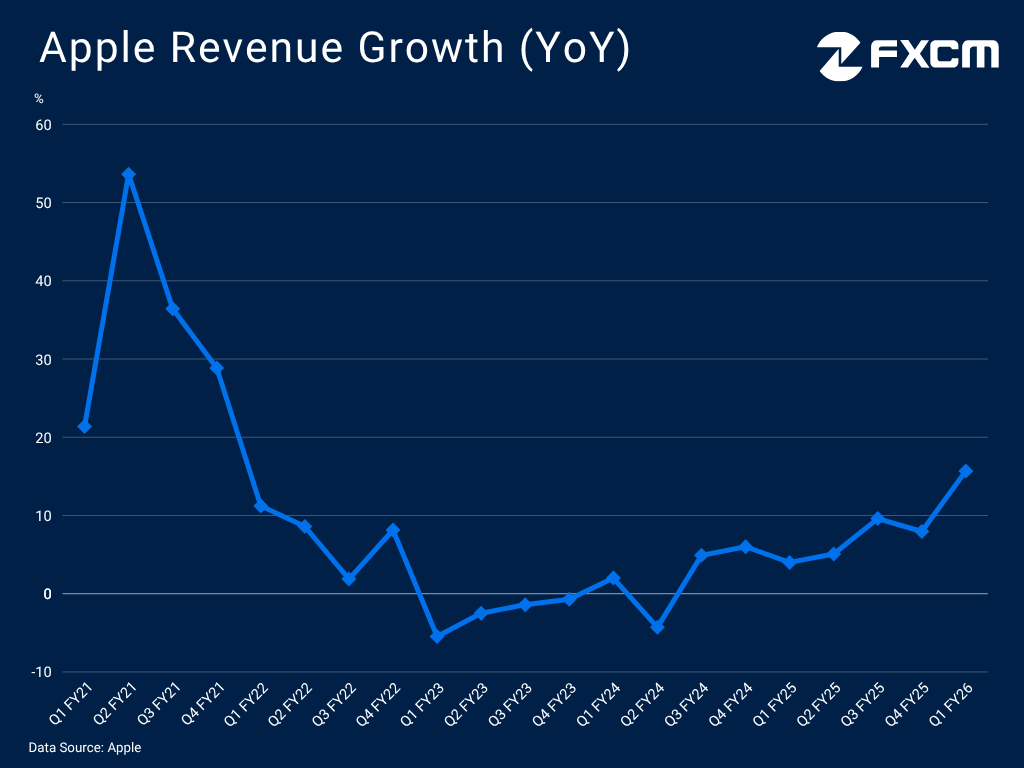

Thursday's earnings find Apple on solid footing following a blockbuster holiday quarter. Revenues for the three months ended December surged 15.7% y/y, the company's strongest performance in over four years, anchored by record-breaking iPhone sales and a vital recovery in China [11]. Momentum carries over as China shipments soared 41% y/y in the first quarter despite the market's 1% contraction according to Omdia [12], while management expects to maintain solid overall revenue growth of 13-16%.

Apple could deliver further good news in the coming months. At June's WWDC conference, the firm is expected to finally unveil the delayed Siri overhaul that would enhance its AI positioning and could facilitate a device upgrade cycle. With long-time hardware chief John Ternus set to take the helm in September, there is optimism that his engineering-first background will accelerate Apple's internal AI development, helping to close the firm's current AI gap.

However, the new CEO will face significant challenges. Apple has a sizeable AI gap to overcome, underscored by its need to partner with Google to power its AI revamp [6]. Meanwhile, it continues to lag on innovation as rivals launch new product categories, spanning as far as Xiaomi's EVs.

Crucially, Apple is uniquely exposed to macroeconomic pressures from tariffs and rising inflation that could weigh on demand for consumer electronics and push costs higher, with a memory chip shortage compounding the issue. IDC forecasts a substantial drop in global smartphone sales this year due to this shortage, while Apple expects it to impact gross margins.

Having defended the 38.2% Fibonacci level, AAPL has the potential to extend its advance to new all-time highs. Another strong earnings report coupled with positive AI signals could facilitate such an outcome. Still, challenges loom, leaving room for disappointment and renewed pressure on the stock.

Chart source: www.tradingview.com

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.