Apple’s Lack of Innovation Hurts its Growth & Caps its Stock

Innovation Lag

The tech giant essentially established the smartphone market with the iPhone launch roughly two decades ago, changed the tablet market with the iPad release in 2010 and popularized wearables with the AirPods and more importantly the iWatch nearly ten years ago.

Despite progress on various fronts (streaming, BuyNowPayLater and more), Apple has not really innovated since then and risks losing some of its appeal and relevance.

Wearables

In an effort to change that, Apple made a foray into the augmented/mixed reality (AR/VR) headset market this year, which is dominated by Facebook-parent Meta Platforms. The Vision Pro appears to be technologically more advanced than the rival devices, with superior pass-through (a significant part of such devices), robust ecosystem and will likely strengthen Apple's patent portfolio. [1]

Its mere entry can lift the AR/VR headset market out of obscurity and Apple aims to capitalize early, in a segment that can grow by around 37% (CAGR) by 2027, according to the International Data Corporation (IDC) [2]. There are limitations though to the proliferation prospects of such devices and using them for long periods of time seems at least uncomfortable. Apple's deep pockets definitely allow it to invest in this still niche market, but this may be more of a FOMO move, while the $3,499 price tag is prohibitive for mass adoption.

As it steps into the AR/VR arena, Apple is facing challenges on another part of the wearables segment, that of fitness and health tracking, which it commands with the iWatch. A few day's ago, arch-rival Samsung unveiled the Galaxy Ring, with shipments due later this year [3]. Apple does not have a smart ring, nor has it disclosed any official plans. The Korean tech giant is looking to tap a market that DataHorizon Research estimates will reach a compound annual growth rate (CAGR) of 25.4% by 2032. [4]

Electric Vehicles

Electric vehicle penetration has been rising, as the world transitions away from fossil fuels and internal combustion engines. In a sign of their increasing appeal, the Tesla Model Y was the best-selling car in the world according to preliminary findings from Jato Dynamic [5], making it the first all-electric car to win this accolade.

Legacy automakers, startups and tech companies have jumped into electrification, trying to establish foothold in the market which is largely dominated by Tesla Motors Inc. Apple has long been rumored to be working on an electric car, but had never shared any concrete plan. We have now learned that the Cupertino-based firm has abandoned this project, as per Bloomberg, missing yet on another opportunity to innovate. [6]

What's more, the revelation comes not long after Chinese smartphone maker Xiaomi launched its own EV, the XU7 sedan. The firm aspires to become one of the top five global automakers and pushes for a highly connected experience, with the Human x Car x Home Smart Ecosystem. [7]

The reported dismantling of its in-house EV team does not necessarily mean that it is out of the market, as it definitely has the ability to buy one of the many struggling startups. Staying away of electromobility can turn out to be a good development, if it enables greater emphasis on Artificial Intelligence.

Artificial Intelligence

OpenAI took the world by storm with ChatGPT, its conversational generative AI chatbot, which launched in late-2022. It sparked a gen AI arms race in Silicon Valley, as all major players are incorporating this transformative technology into their products and services.

Apple however appears to have been caught off guard and risks missing out on perhaps the most important technological development since the World Wide Web. It has been secretive around its plans, with CEO Tim Cook saying that it will share detail on its AI work "later this year" [8], but a late entry can put it at a significant disadvantage.

Korean smartphone giant Samsung already leans heavily on this technology with the potential to spark a new smartphone super-cycle, after the adversities of the last two years. It unveiled its own large language model last year and launched AI-powered smartphones in January, with features like live call translation. [9]

Lack of Growth

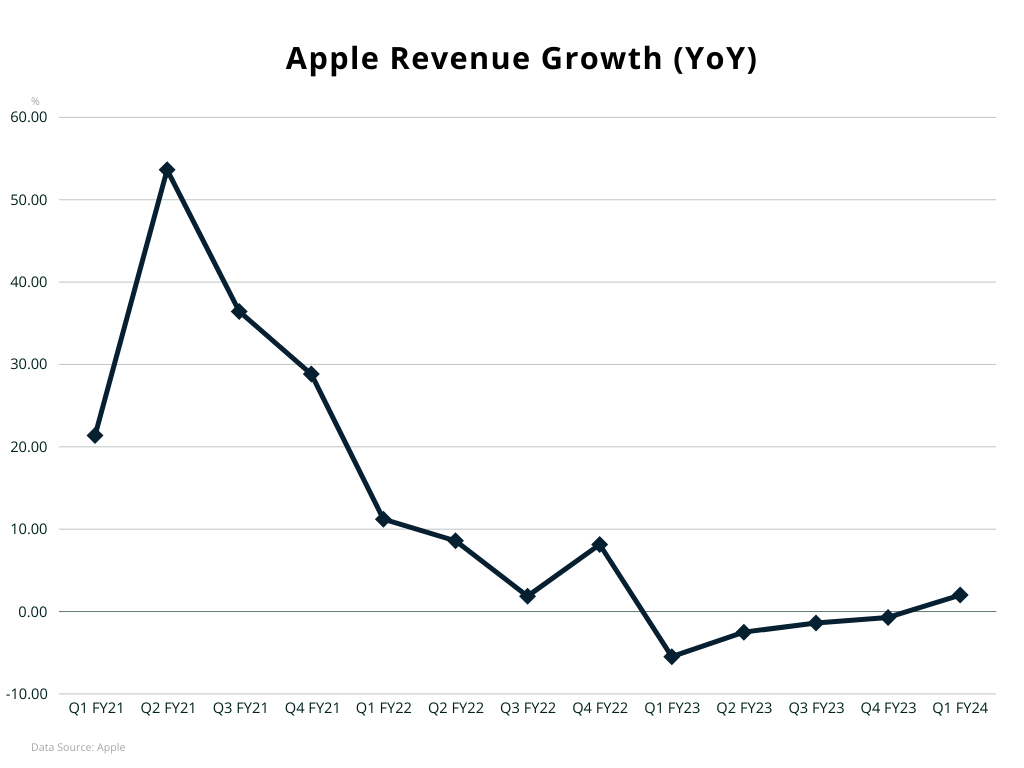

Apple's total revenues shrank in all four quarters of the previous fiscal year, which constituted the worst slump in twenty-two years and the post-iPhone era. Although it managed to snap the negative streak in the December quarter (Q1 FY24) with a marginal 2% y/y increase [10], it could slip back in contraction. The firm does not provide exact guidance, but CFO Luca Maestri expects "similar" revenue for the current quarter compared to the prior year. [8]

Making matters worse, the company appears to be losing its grip on China amidst resurgent domestic makers and relations Sino-Western fraught, which can hurt the appeal of American brands. Sales in Greater China fell nearly 13% y/y in Q1 FY24, despite the release of the latest iPhone. Adding to the worries, Counterpoint Research found that iPhone unit sales fell 24% y/y in the first six weeks of the current calendar year, partly due to"stiff competition". [11]

The smartphone market had a tough period over the last two years due to supply disruptions, high inflation, maturity and other factors. That has constrained iPhone shipments, Apple's main revenue generator. Despite resilience and taking the top spot globally for the first time in 2023 as per Canalys, actual unit sales slipped from a year ago [12]. The smartphone market appears to be bottoming out, but Apple is not out of the woods yet. It could be in more trouble, especially if it continues to leave unanswered the AI advances of its rivals and mainly Samsung.

The increasingly important services segment that includes the App Store, advertising, cloud storage, music, streaming and more, has been going from strength to strength. However, this may not be enough, if iPhone lags and Macs and iPads continue to disappoint.

Stock Headwinds

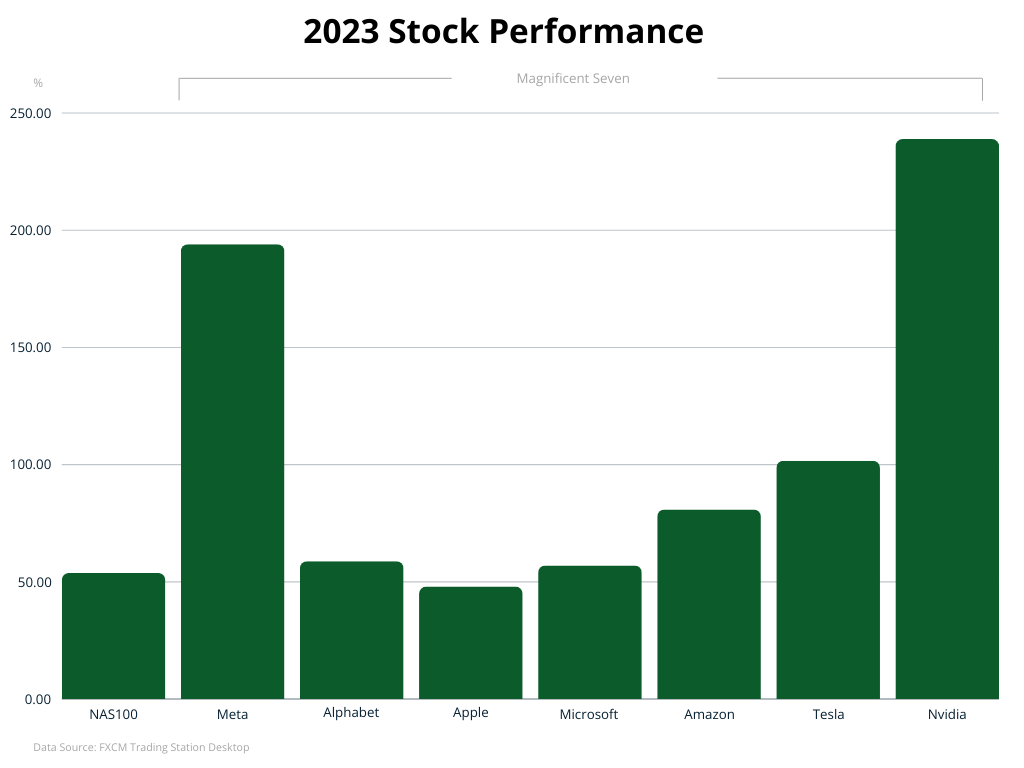

Apple's stock registered profits and all-time highs in 2023, but with a sub-50% y/y increase was easily outpaced by its Magnificent Seven peers. The enabler of the AI revolution Nvidia and Meta with its renewed focus on this technology, led the pack.

The sky-high valuation offers reasons for concern given the lack of growth and the company will need to find a driver to accelerate its sales. The new year has started with a notable decline, entering correction territory, with losses in excess of 10% YTD. Moreover, Apple lost the crown of the most valuable company in the world to Microsoft, which benefits from its leading work on generative AI.

Conclusion

Apple needs to find a driver that will accelerate its top and bottom lines, the way iPads and wearables have done in the past. The Vision Pro AR headset may help reposition itself as a company that pushes the envelope technologically, but will have little contribution to the balance sheet in the near term (if ever). Its best chance may be to speed up its efforts on the AI front and challenge its rivals. The annual June Developers Conference is a likely venue for any announcements, as this is where it typically unveils new products and services.

On the other hand, Apple does not necessarily need to become a disruptor again to find room for growth. It may be enough to stay close to competition, to satisfy its vast and committed customer base. Its services segment expansion is crucial, as it strengthens its moat and makes leaving its ecosystem difficult.

Headwinds in China are worrying but Apple is making strides in India, the world's most populous country, with an economic expansion that outpaces China. Furthermore, the global handhelds and PC markets appear to be stabilizing and look primed for a rebound. The stock is losing ground this year and further decline could be in store, but a correction is reasonable. Apple remains one of the most valuable companies in the world and it will be hard for investors to lose faith.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.