Tesla loses EV crown to BYD as 2025 deliveries drop

Tesla deliveries drop in 2025 as Elon Musk focuses on his AI vision

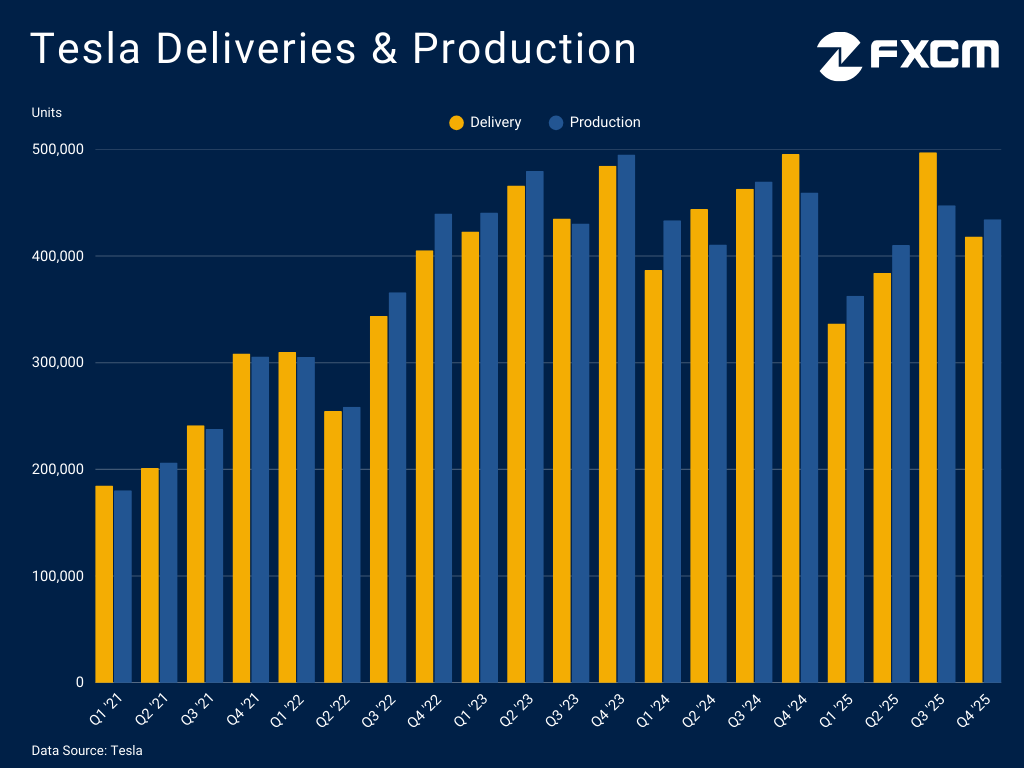

Tesla's deliveries fell 8.56% in 2025 to 1,636,129 units [1], marking a second consecutive annual decline and underscoring the company's struggles in its core automotive segment. Deliveries received a temporary boost in the third quarter as buyers rushed to take advantage of tax breaks before they expired, but sales plunged in Q4 as the EV maker faced a challenging operating environment.

Trump's rollback of clean energy incentives adds to headwinds from tariffs and broader economic uncertainty, which continue to dampen demand for electric vehicles. While stripped-down, more affordable versions of the Model Y and Model 3 may support buying interest, they are unlikely to generate excitement, particularly overseas where competitors offer compelling entry-level alternatives. These include Renault, Stellantis-owned Fiat and, most notably, China's BYD, which dethroned Tesla for the first time. BYD delivered 2,256,714 pure battery electric passenger vehicles last year [2], supported by rapid technological progress, affordable pricing and a broad product lineup.

Against this backdrop, Tesla's automotive business could continue to struggle in 2026 as Elon Musk pivots towards autonomous driving and humanoid robotics. While progress is tangible and Tesla expects to begin volume production of its dedicated Cybercab this year [3], the company remains well behind rivals such as Alphabet's Waymo and Baidu's Apollo Go. Humanoid robotics, meanwhile, appears to be an even longer-term ambition.

The strategic shift towards AI could unlock substantial long-term value for Tesla, and markets have so far been supportive of this vision, with TSLA.US rising 11.4% last year and reaching record highs. However, the former EV leader risks remaining caught between a weakening automotive business and AI ambitions that may take years to deliver meaningful returns, leaving the stock vulnerable to renewed downside pressure.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 02 Jan 2026 https://ir.tesla.com/press-release/tesla-fourth-quarter-2025-production-deliveries-deployments | |

| Retrieved 02 Jan 2026 https://www1.hkexnews.hk/listedco/listconews/sehk/2026/0101/2026010100423.pdf | |

| Retrieved 02 Aug 2026 https://assets-ir.tesla.com/tesla-contents/IR/TSLA-Q3-2025-Update.pdf |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**