Nvidia delivers strong earnings on AI demand but challenges linger

Growing AI capex fuels strong earnings and guidance

Tech giants continue to pour vast amounts of capital into data centres and infrastructure to power their AI capabilities. Alphabet, supported by renewed AI momentum, guided for nearly double capital expenditure in 2026 [1], while Amazon.com expects spending to rise by roughly 50% [2]. Meta Platforms is ramping up investment by 59.2% to 86.9% [3] as it pushes towards superintelligence and expands its partnership with Nvidia. [4]

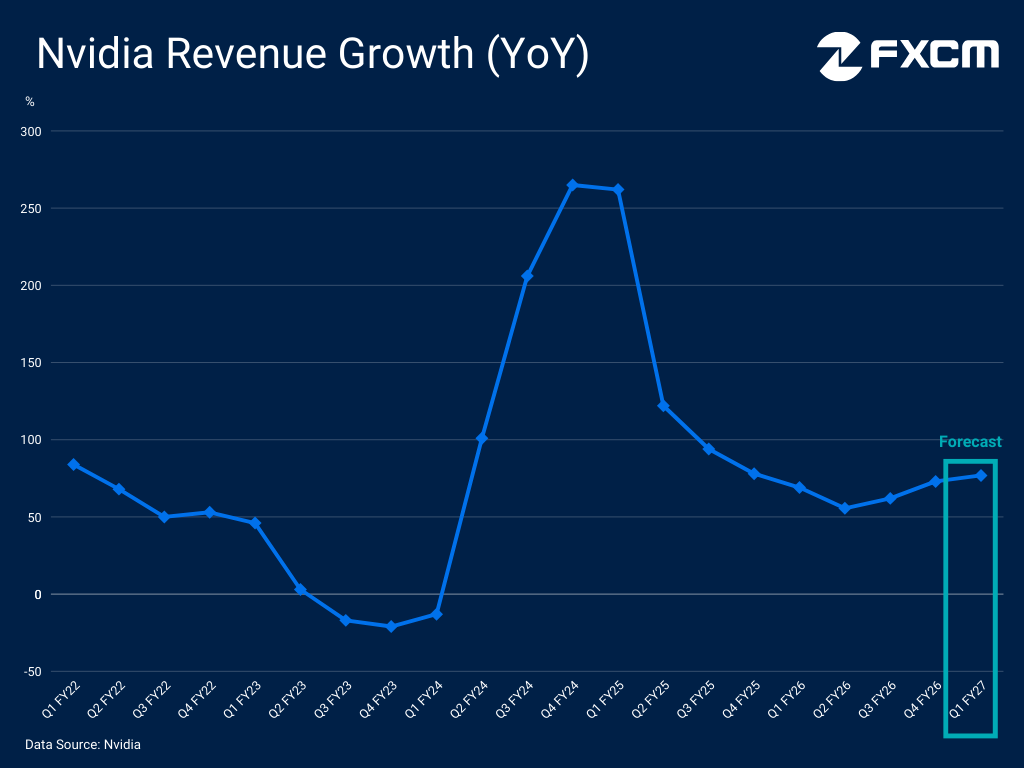

NVIDIA remains the key enabler and beneficiary of these investments, as its chips continue to be the preferred solution for training and inference while agentic AI becomes the next inflection point. Hyperscaler demand drove revenues to a record $68.127 billion in Q4 FY26, up 73% year on year, and management guided for faster growth of 74.9% in the current quarter. The new and more efficient Vera Rubin architecture is expected to continue supporting top and bottom lines, with CFO Colette Kress noting during the earnings call that production shipments are set for the second half of the year. [5]

Rising competition and diversification efforts

Nvidia is the undisputed king of the AI boom, but its leadership is unlikely to remain unchallenged and competitive pressures are increasing. Rival chipmaker AMD posted strong results and guidance as its data centre business benefits from accelerating AI investment, projecting average annual revenue growth of more than 35% over the next three to five years [6]. Highlighting its progress, AMD secured a long-term infrastructure agreement with Meta for up to 6 GW of Instinct GPUs earlier this month [7], following deals with OpenAI and others.

At the same time, several of Nvidia's largest customers are developing in-house chips in a bid for greater self-reliance and diversification. Alphabet has emerged as a frontrunner after making its Ironwood TPUs generally available [8]. Microsoft introduced its Maia 200 AI accelerator for inference in January [9], while Amazon recently unveiled its most advanced AI chips to date. [10]

China challenges linger

China remains a persistent headwind for Nvidia. Although the US government approved limited shipments of H200 chips to China-based customers, these approvals have not generated any revenue, according to CFO Colette Kress. Nvidia's guidance for the current quarter excludes any contribution from China, underscoring the ongoing challenges.

Against the backdrop of export restrictions and an adversarial trade environment, Beijing appears reluctant to allow Nvidia's semiconductors into the country as it accelerates efforts towards technological independence. President Xi stressed earlier this month that self-reliance in science and technology is critical for China's strength [11], with domestic tech firms aligning around this goal. Baidu recently unveiled a range of in-house chips for training and inference, with the M100 expected later this year [12], while Alibaba launched the Zhenwu 810E as an alternative to Nvidia's AI chips. [13]

Spending, production and concentration risks

Demand for AI infrastructure remains robust, but tariffs, export controls, critical minerals sourcing and power constraints continue to pose headwinds for the semiconductor industry and the wider adoption of AI, just as a memory crunch begins to take shape. While management expressed confidence in inventory levels and the ability to meet AI demand through 2027, the CFO acknowledged that the gaming segment could come under pressure.

Meanwhile, markets are becoming more cautious about massive capital spending and rising debt issuance against a challenging macroeconomic backdrop, while fears of disruption persist. However, CEO Jensen Huang largely dismissed these concerns, stating that "compute is revenue".

Another area of concern is revenue concentration. The AI boom remains confined to a small group of hyperscalers and Nvidia's exposure is significant. The company's 10-K filing for the fiscal year ended in January showed that just two customers accounted for 36% of total revenue, up from three customers representing 34% the previous year. [14]

Nvidia stock outlook

NVIDIA shares are up less than 5% this year amid shifting positioning and market dynamics, but the stock continues to outperform the S&P 500 and its Magnificent Seven peers, highlighting its enduring AI appeal. Nvidia's leadership is not under any imminent threat and the strong earnings and guidance can continue to support the bullish outlook and push NVDA towards new all-time highs.

Nonetheless, the earnings report also highlighted persistent challenges, particularly related to China. Against elevated concentration risks, production constraints, trade uncertainty and mounting concerns over spending, the results may fail to inspire markets and could push shares lower. NVIDIA remains exposed to the pivotal EMA200 and 38.2% Fibonacci of the 2025 low which would tests the upside bias.

Chart Source: www.tradingview.com

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**