Copper Benefits for China’s Broad Stimulus

Copper Analysis

After the May record peak, prices slumped as oversupply fears creeped in and concerns of a global economic slowdown took hold. On the demand side, the two main driving forces faced pushback. Euphoria over the Artificial Intelligence boom that boosts chip making gave way to skepticism, while the clean energy transition faced some backlash and EV adoption has slowed.

However optimism returned over the last couple of months and the non-ferrous metal got a double boost from the US and China, with the latter being the world's top consumer. The US Fed pivoted this month with a jumbo 0.5%, pointing to an aggressive path ahead [1]. This strengthens the case for a soft landing and can also revitalize the real estate market, as mortgage rates are expected to decline.

China has been ramping up its efforts to prop the bumpy post-pandemic recovery on both the fiscal and monetary fronts. This week marked an acceleration as the central bank slashed the medium term lending facility (MLF), announced plans to lower the amount of reserves banks need to hold and to support for the stock market [2]. Crucially, the plan includes lower mortgage rates on existing home loans and a reduction in rates for second homes, in further support for the ailing real estate sector.

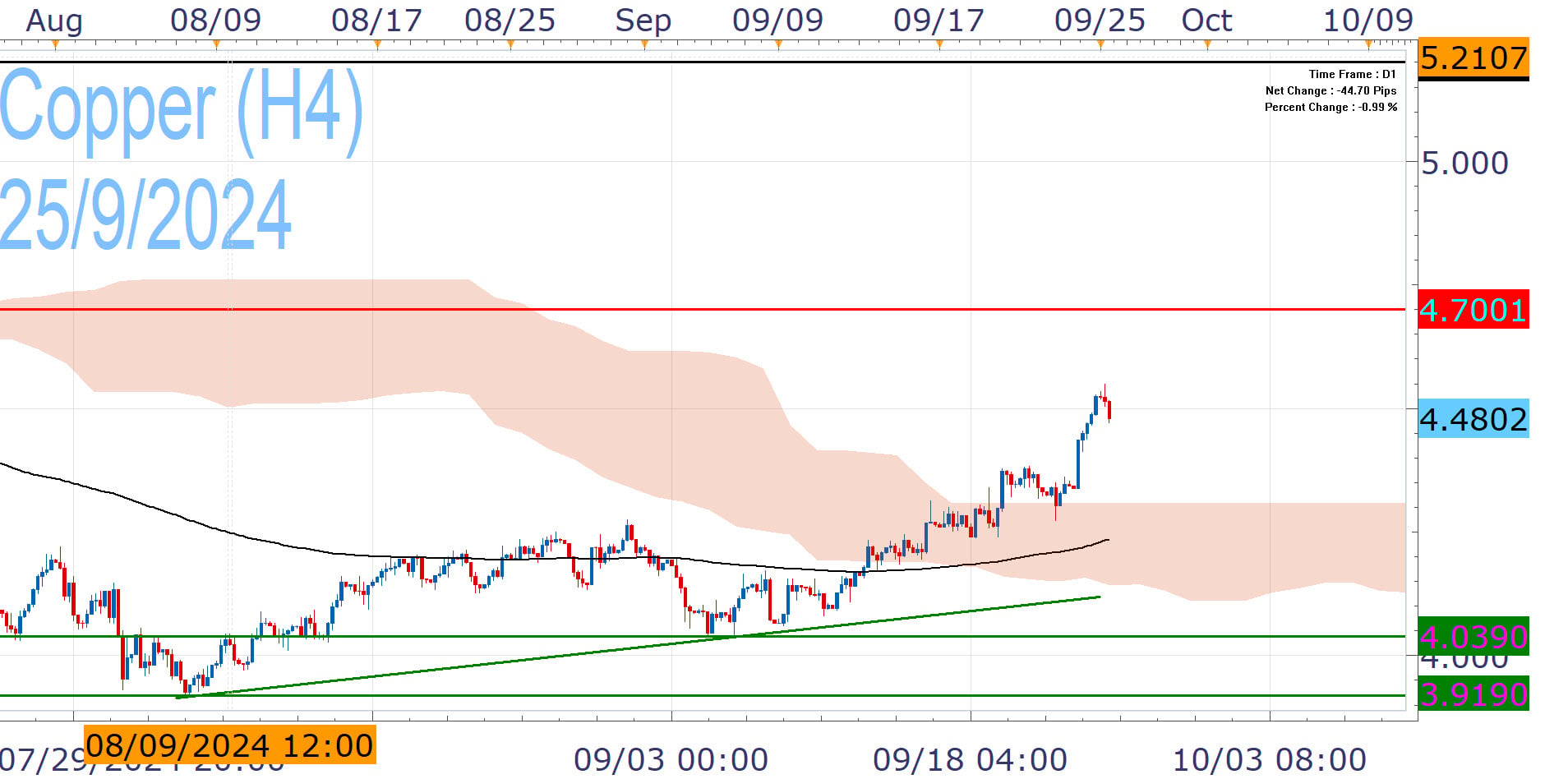

Copper prices jumped on the news and so did the stocks of producers like Anglo American, BHP and Rio Tinto. Copper extended its rebound testing the 4.500 handle and has the opportunity to take out the 4.700. Despite recent concerns, AI continues to drive demand and the EV market could rebound as lower interest rates around the world are likely to lower funding costs.

On the other hand, the Fed's frontloading risks pushing up inflation and that could lead to fewer cuts ahead. China's monetary actions are definitely in the right directions but more is needed, especially in the stimulus front. But bolder action carry risks. On the technical front, the move looks stretched so a pullback into the daily Ichimoku Cloud would be reasonable. Daily loses below the EMA200 (black line) would pause the bullish momentum, but the downside appears well protected and prolonged weakness does not look easy, technically not fundamentally.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 25 Sep 2024 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20240918.htm | |

| Retrieved 02 Aug 2026 https://english.www.gov.cn/news/202409/25/content_WS66f3602ec6d0868f4e8eb3c0.html |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**