GBP/USD in Peril after Strong NFPs & Dovish BoE

GBP/USD Analysis

The Bank of England stepped in to monetary easing earlier than the Fed, with a 0.25% cut, but did not follow through with another move last month and advocated for a "gradual approach" [1]. Its US counterpart however delivered a jumbo 0.5% pivot in September and pointed to an aggressive easing path ahead.

However, Fed Chair Powell sought to cool down market expectations with a more reserved speech last Monday. He warned that "this is not a committee that feels like it is in a hurry to cut rates quickly" and pointed to another 50 bps of cuts within the year [2]. The strong jobs report at the end of that same week extrapolated the messaging and markets now have priced out previously more aggressive bets for 75 bps of cuts. At the same time, BoE governor Bailey surprised markets with a dovish shift in his messaging. Speaking at The Guardian he said that policymakers could be "a bit more activist" in lowering rates [3], boosting market bets for a cut at the next meeting.

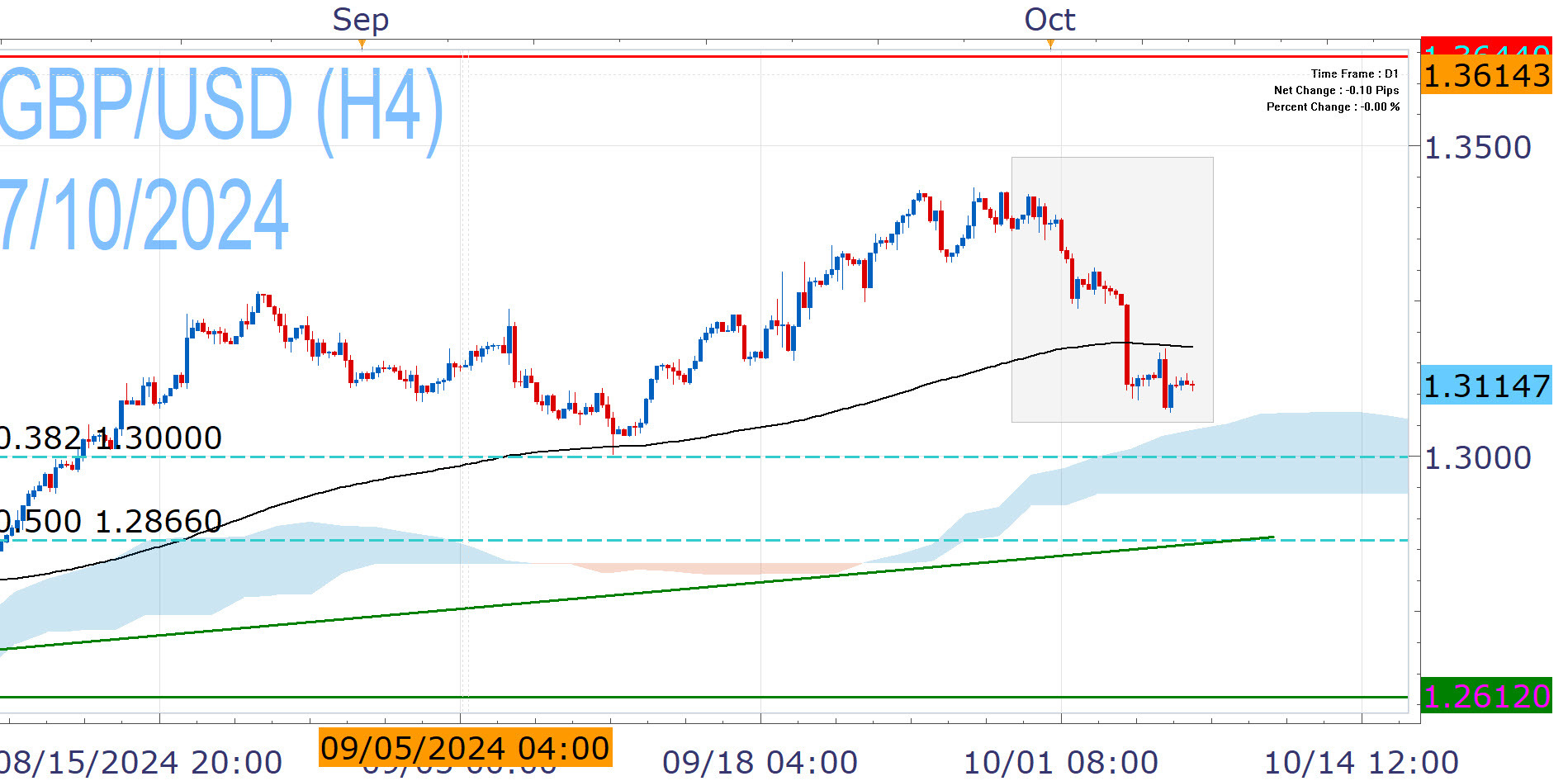

This shift in monetary policy dynamics led GBP/USD to its worst week of the year, with losses of nearly 2%. Crucially, it dropped below the EMA200 (black line) which negates the bullish bias and exposes it to the 38.2% Fibonacci. A breach would create risk for deeper correction, but sustained weakness is not easy.

The US Fed has laid out a much more clear and extensive easing path than the Bank of England, so the broader policy differential could still be supportive. Furthermore, the downside appears well-protected technically, with the daily Ichimoku Cloud and the ascending trend line form this year's lows. Above the pivotal 38.2% Fibonacci, GBP/USD can retake the EMA200 and control. Successful effort would keep the door open to new 2024 highs (1.3434), although gains are likely to be incremental form here on.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 07 Oct 2024 https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2024/september-2024 | |

| Retrieved 07 Oct 2024 https://www.youtube.com/live/fbp9cRgWrBk | |

| Retrieved 02 Aug 2026 https://www.theguardian.com/business/2024/oct/03/its-tragic-bank-of-england-governor-watching-middle-east-crisis-closely |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**