AUD/USD Cautious Despite the RBA’s Hold & Hawkish Stance

AUD/USD Analysis

The Reserve Bank of Australia kept rates at % and their twelve year highs for the seventh straight time and repeated the need for vigilance against inflation and a sufficiently restrictive stance [1]. Furthermore, Governor Bullock once again ruled out rate cuts in the near term during her post-meeting press conference [2]. The decision and messaging places the RBA at odds with the global trend of removing monetary restriction.

Consumer prices have come down substantially this year, but policymakers pre-empted further declines as temporary. They remain wary and don't expect inflation to return back to the 2-3% target for another two years. Furthermore, wages remain elevated despite moderation and the labor market is still tight.

However, with a struggling economy and global peers having delivered multiple cuts, this hawkish stance may become increasingly hard to sustain. There was already some softening, as Governor Bullock said that a rate hike was not discussed this time around. This was the first time since March that such action was not contemplated by the Board.

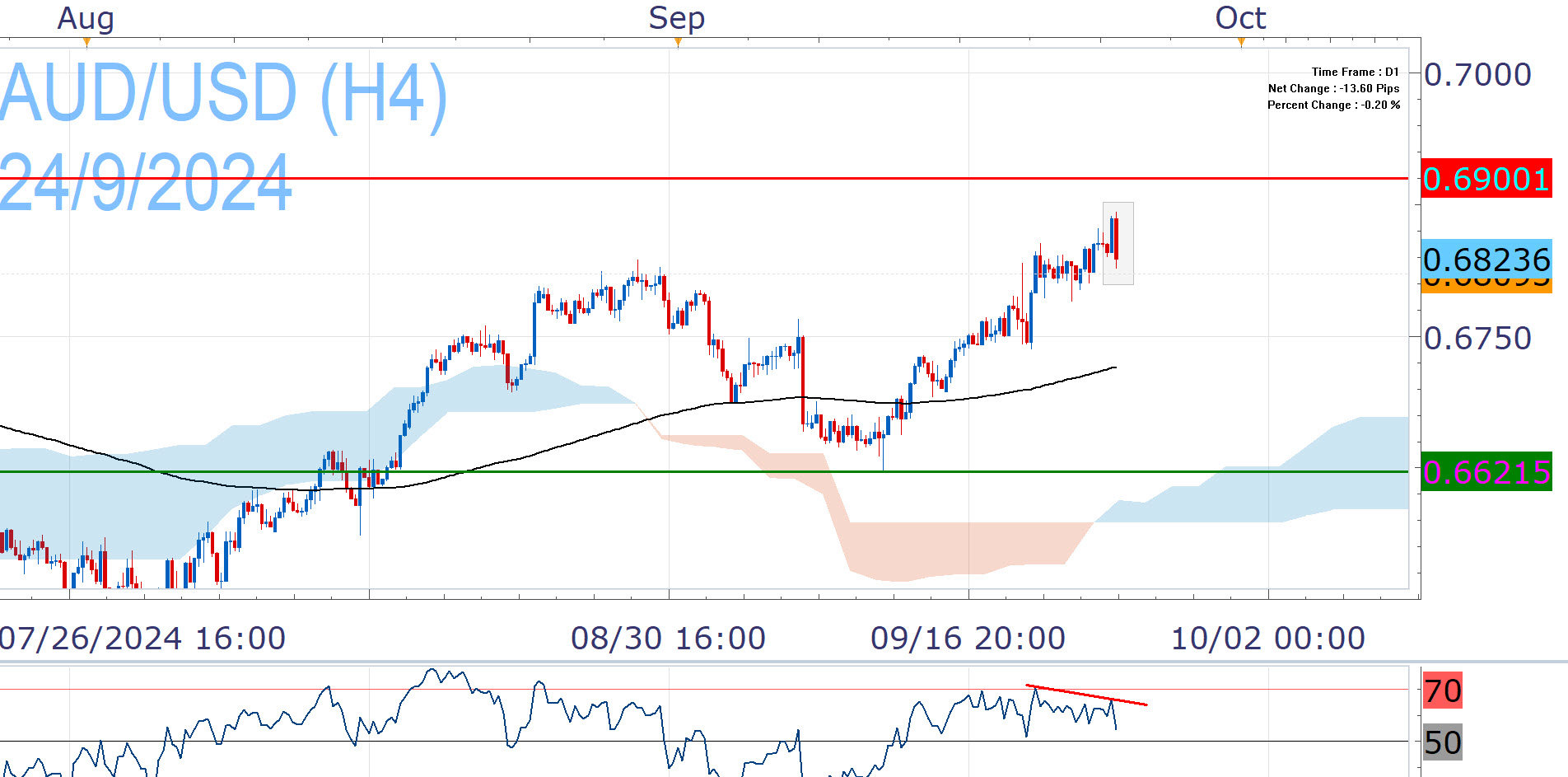

AUD/USD rose to new 2024 highs due to the RBA's commitment to monetary restriction, just as the US Dollar is harmed by the Fed's aggressive pivot. The US central bank delivered a jumbo rate cut of 50 bps last week, while pointing to an aggressive easing path ahead [3]. The monetary policy differential favors the pair, which has the chance to extend its recovery past the 0.6900 handle.

However AUD/USD falters ahead of that handle and erases initial gains, weighed by the lack of discussion of a hike by RBA officials. Furthermore, the RSI has not followed price action higher, creating scope for a pullback towards the EMA200 (black line). Daily closes below it would pause the bullish bias, but that is hard to justify under current policy dynamics.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.

References

| Retrieved 24 Sep 2024 https://www.rba.gov.au/media-releases/2024/mr-24-18.html | |

| Retrieved 24 Sep 2024 https://rba.livecrowdevents.tv/MediaConferenceMonetaryPolicyDecision24Sept/stream | |

| Retrieved 02 Aug 2026 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20240918.htm |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, Friedberg Direct, FXCM or its affiliates takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of Friedberg Direct and FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the Friedberg Direct's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.**